2022 U.S. PET SUPPLIES SPENDING $21.94B…Down ↓$1.86B

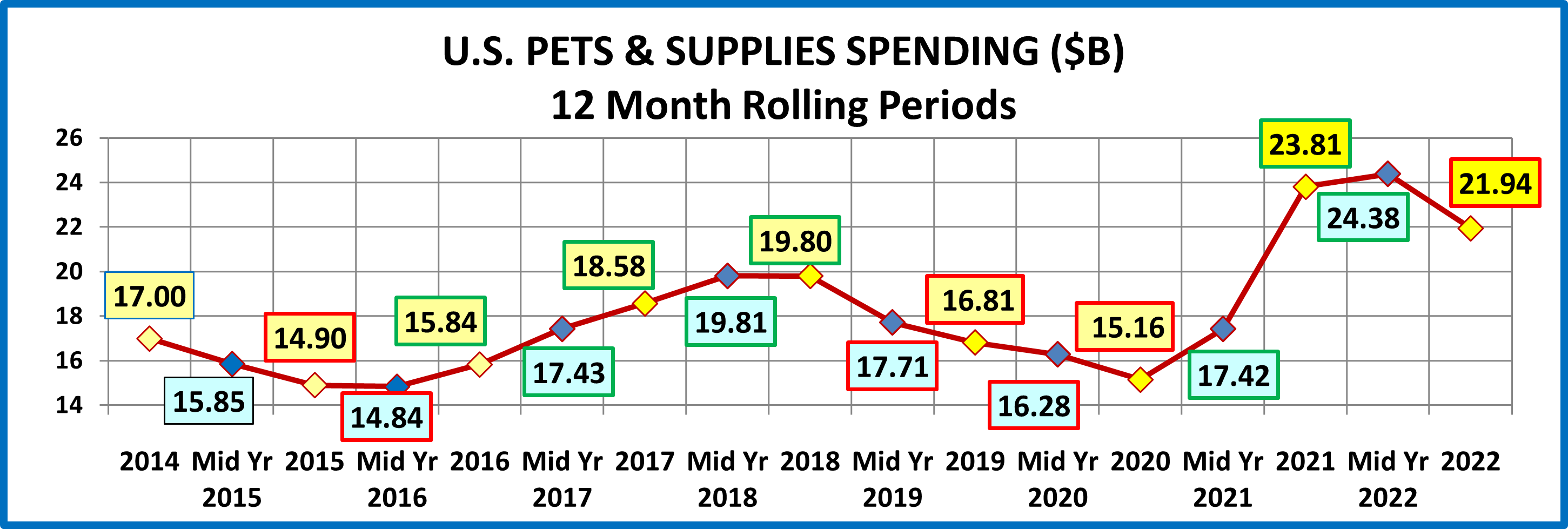

Total Pet spending grew to $102.71B in 2022, up $2.73B (+2.7%) from 2021. After a record $8.75B (+57%) increase in 2021 the Supplies segment fell $1.86B, (-7.8%) to $21.94B in 2022. (Note: All numbers in this report come from or are calculated by using data from the US BLS Consumer Expenditure Surveys)

Supplies Spending fell -$4.6B 2018>2020 due to Tarifflation and the Pandemic. In 2021, Pet Parents caught up with their needs. Spending turned up in the 1st half then skyrocketed in the 2nd half. In 2022, it plateaued in the 1st half then fell sharply in the 2nd half. We’ll drill down into the data to determine what and who was behind the drop in Spending.

In 2022, the average household spent $163.64 on Supplies, down 8.2% from $178.20 in 2021. (Note: A 2022 Pet CU (68%) Spent $240.65) This doesn’t exactly match the -7.8% total $ decrease. Here are the specific details:

- 0.4% more CU’s

- Spent 10.0% less $

- 2.1% more often

Let’s start with a visual overview. The chart below shows recent Supplies spending history.

Since the great recession, spending in the Supplies segment has been driven by price. Although many supplies are needed by Pet Parents, when they are bought and how much you spend is often discretionary. When prices fall, consumers are more likely to buy more. When they go up, consumers spend less and/or buy less frequently.

2014 was the third consecutive year of deflation in Supplies as prices reached a level not seen since 2007. Consumers responded with a spending increase of over $2B. Prices stabilized and then moved up in 2015.

In 2015 we saw how the discretionary aspect of the Supplies segment can impact spending in another way. Consumers spent $5.4B for a food upgrade and cut back on Supplies – swapping $. Consumers spent 4.1% less, but they bought 10% less often. That drop in purchase frequency drove $1.6B (78%) of the $2.1B decrease in Supplies spending.

In 2016, supplies’ prices flattened out and consumers value shopped for their upgraded food. Supplies spending stabilized and began to increase in the second half. In 2017 supplies prices deflated, reaching a new post-recession low. The consumers responded with a $2.74B increase in Supplies spending that was widespread across demographic segments. An important factor in the lift was an increase in purchase frequency which was within 5% of the 2014 rate.

In 2018 prices started to move up in April and rapidly increased later in the year due to the impact of new tariffs. By December, Supplies prices were 3.3% higher than a year ago. This explains the initial growth and pull back in spending.

In 2019 we saw the full impact of the tariffs. Prices continued to increase. By yearend they were up 5.7% from the Spring of 2018 and spending plummeted -$2.98B. The major factor in the drop was a 13.1% decrease in purchasing frequency.

2020 brought the pandemic. Prices deflated but with retail restrictions and the consumers’ focus on needed items, both the amount spent and frequency of purchase of Supplies fell.

In 2021 the recovery began with a strong lift in the 1st half that reached record levels in the 2nd half. Pet parents bought all the supplies that they had been putting off for 2 years because of Tarifflation and the Pandemic. It was the greatest lift in history, but 2021 spending ended up where it was headed in 2018 before being “derailed” by outside influences.

In 2022 inflation took off, especially in the 2nd half. Spending plateaued then fell -$2.44B in the 2nd half. Consumers just spent less per transaction. This was not a surprise after the buying binge in 2021.

That gives us an overview of the recent spending history. Now let’s look at some specifics regarding the “who” behind the 2022 drop. First, we’ll look at spending by income level, the most influential demographic in Pet Spending.

National: $163.64 per CU (-8.2%) – $21.94B – Down $1.86B (-7.8%).

Only the $70>100K & $100>$150K income groups spent more but the 50/50 $ divide stayed the same at $114K.

- <$30K (23.8% of CUs)- $63.42 per CU (-17.4%); $2.02B– Down $0.59B (-22.7%). This group is very price sensitive, so they had the biggest percentage decrease and spending fell to the pre-pandemic 2019 level.

- $30K>70K (28.9% of CUs)- $111.91 per CU (-9.6%); $4.34B – Down $0.57 (-11.6%). This big, lower income group matches both the national spending pattern and that of the $150K+ group. 2019 Tarifflation and 2022 inflation had big impacts. Amazingly enough, until 2019 they were the leader in Total Supplies $. Now, they rank 3rd.

- $70>$100K (14.1% of CUs) – $172.08 per CU (+7.3%); $3.26B – Up $0.08B (+2.6%). This middle-income group had consistent spending. 2020 hit them hard but they rebounded strong in 21 and spending even grew slightly in 22.

- $100K>$150K (15.5% of CUs) – $238.62 per CU (+4.0%); $4.96B – Up $0.61B (+14.0%). This high income group had the 2nd biggest COVID drop. In 21 they had the 2nd strongest recovery. In 22, they had the only significant increase.

- $150K> (17.7% of CUs) – $310.84 per CU (-25.2%); $7.36B – Down $1.39B (-15.9%). This highest income group had the biggest $ drop, which is not surprising after a $4.6B lift in 2021. They still remain the Supplies spending leader. BTW, the $150>200K group actually spent $1.3B more on Supplies in 2022 while $200K> spent $2.7B less.

All groups $70K>199K spent more. The drop came in the 2nd half because it was impossible to repeat the $6.4B lift in 2021.

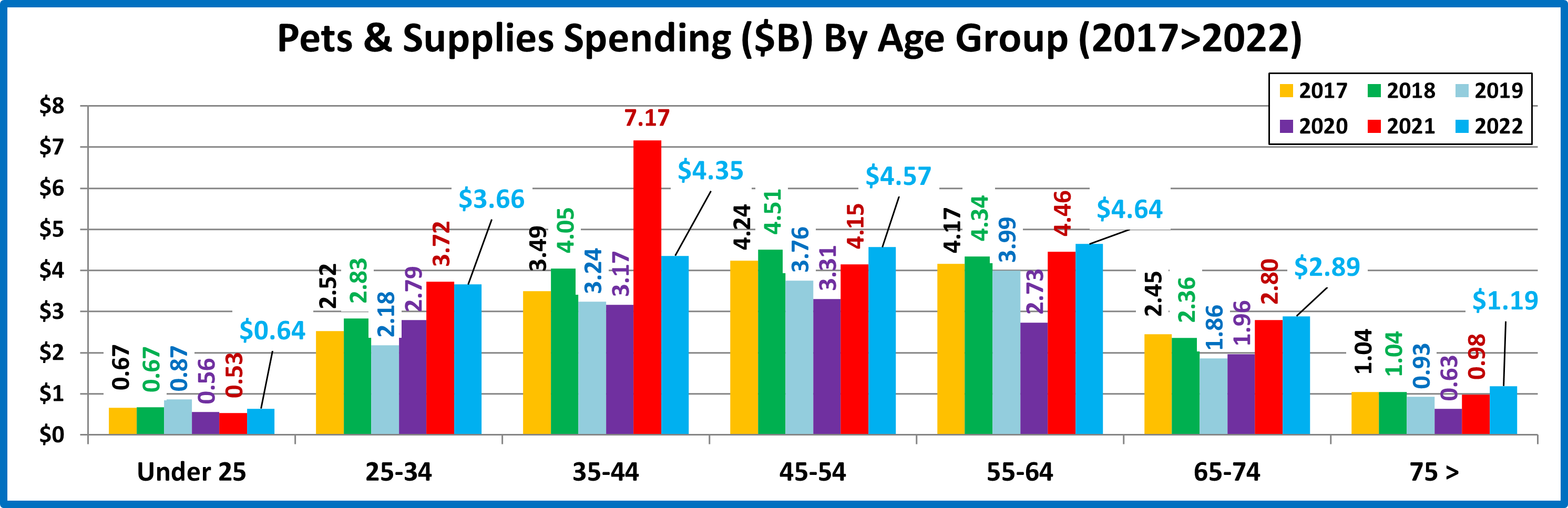

Now, we’ll look at spending by Age Group.

National: $163.64 per CU (-8.2%) – $21.94B – Down $1.86B (-7.8%)

It’s simple. Under 25 and over 45 spent a little more. 25>44 spent less, especially the 35>44 yr-olds.

- 55>64 (18.2% of CUs) $190.04 /CU (+5.4%); $4.64B – Up $0.18B (+4.1%). Tarriflation caused a spending drop in 2019. Spending fell again in 2020 as they binge bought pet food. They had a strong recovery in 2021 and slowly grew in 2022 as 1.3% less CUs spent 3.1% more on Supplies, 2.3% more often. They are back in the #1 spot.

- 45>54 (16.9% of CUs) $201.44 per CU (+8.0%); $4.57B – Up $0.42B (+10.0%). From 2007>2018 this highest income group was the leader in Supplies spending. They came back from the pandemic drop with growth in 21 and again in 22 as 1.8% more CUs spent 1.8% less, 10.0% more often. They were #1 in 2020 but are now #2.

- 35>44 (17.0% of CUs) $190.89 per CU (-38.9%); $4.35B – Down $2.81B (-39.2%) They are 2nd in income and expenditures. Strong inflation drove their $ down in 2019 but the Pandemic had little impact. Spending took off in 2021 but plummeted in 2022 as 0.5% less CUs spent 40.5% less $, 2.7% more often. They fell from #1 to #3.

- 25<34 (15.6% of CUs) $175.18 per CU (-1.0%); $3.66B – Down $0.06B (-1.6%). After trading Supplies $ for upgraded Food and Vet Care in 2016, these Millennials turned their attention back to Supplies. Tarriflation hit them hard in 2019 but they actually increased spending in the pandemic. The lift grew even stronger in 2021 but then spending fell slightly in 2022 as 0.6% less CUs spent 0.2% more $, 1.2% less often.

- 65>74 (16.2% of CU’s) $132.82 per CU (+1.9%); $2.89B – Up $0.09B (+3.1%). This older group is very price sensitive so rising prices caused them to cut back on spending in 2019. Like the 25>34 yr-olds, they also increased spending in 2020 and spending soared in 2021. However, unlike 25>34 yr-olds, their spending grew in 2022 as 1.2% more CUs spent 0.1% less $, 2.1% more often.

- 75> (11.4% of CU’s) $77.89 per CU (+16.0%); $1.19B – Up $0.21B (+21.8%). This low-income group is price sensitive but they are committed to their pets. Their spending was severely impacted by the Pandemic, but they had a strong recovery in 2021 and now 2022 as 4.9% more CU’s spent 20.5% more, 3.7% less often.

- <25 (4.7% of CUs) $101.89 per CU (+27.2%); $0.64B – Up $0.11B (+20.7%). Many formed CUs with other young adults or got married, but most made Pets a priority. In 2022 5.1% less CUs spent 46.4% more $, 13.1% less often.

The 25>44 2021 binge buyers didn’t repeat in 2022. All other groups spent a little more in 2022.

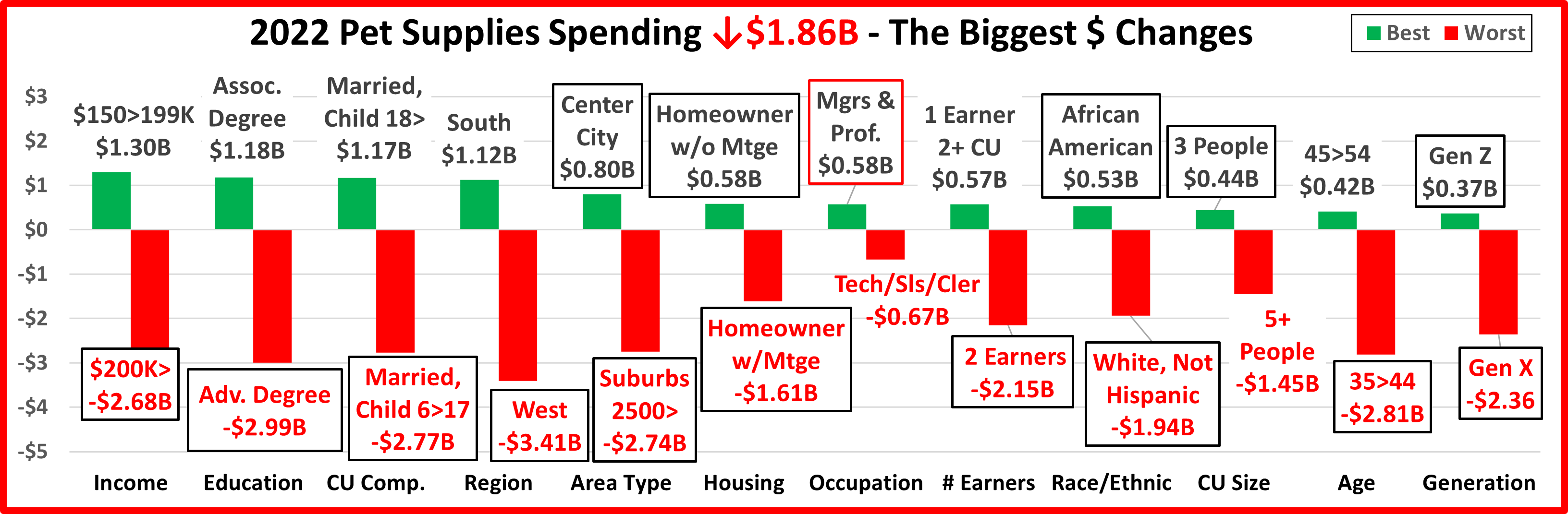

Next, let’s take a look at some other key demographic “movers” in 2022 Pet Supplies Spending. The segments that are outlined in black “flipped” from 1st to last or vice versa from 2020. The red outline stayed the same.

In 2021, 97% of all segments spent more and in 9 categories all segments had increases. In 2022, despite the decrease, 52% of segments still spent more. 15 of 24 segments flipped from 1st to last or vice versa. Only 1 segment held its spot. 5 flipped from last to 1st but 10 flipped from 1st to last. The 2021 binge buy was clearly not repeated.

Only 3 of the winners are the “usual suspects”

- $150>199K

- Mgrs & Professionals

- 45>54 yr-olds

The other 9 are all somewhat surprising.

In the losers group, only 2 – Tech, Sls, Clerical and 5+ are not surprises. The others are and all 10 flipped from 1st to last.

The 2021 $8.65B increase in Supplies $ was the biggest in history. This was a binge buy as Pet Parents purchased all of the needed Supplies that they had put off buying during the pandemic. Like the 2020 panic binge buy in Pet Food, there was no need for it to be repeated so spending fell in the following year. The drops in both segments were relatively small compared to the binge lifts. Supplies fell $1.86B (-7.8%) in 2022 but there were still many positives as 52% of all demographic segments spent more on Supplies than they had in 2021. There is another factor to be considered to put 2022 Supplies spending in a better perspective. Many Supplies categories have been commoditized, so the segment is very susceptible to price changes. Prices rose in 2018/19 and spending fell -$4.6B. Prices fell 2016>18 and spending grew by $5B. In 2022 the inflation rate was 7.7%. That means that the drop in the amount of Supplies purchased in 2022 was really -14.4%. That’s almost double the actual $ drop. Plus, all segments with an increase below 7.7% bought less.