We looked at the Total Pet Spending for 2018 and its key demographic sources. Now we’ll start drilling down into the data. Ultimately, we will look at each individual segment but the first stop in our journey of discovery will be Pet Products – Pet Food and Supplies. Food and Supplies are the industry segments that are most familiar to consumers as they are stocked in over 200,000 U.S. retail outlets, plus the internet. Every week over 22,000,000 U.S. households buy food and/or treats for their pet children. Pet Products accounted for $48.65B (61.9%) of the $78.6B in Total Pet spending in 2018. This was down $1.046B (-2.1%) from the $49.69B that was spent in 2017. We have seen that this drop was caused by the reaction to the FDA warning on grain free dog food which drove food spending down in the second half combined with new tariffs on Supplies, which flattened spending in that segment in the second half.

Overall, in 2018 Pet Food spending fell -$2.27B, while Supplies spending growth slowed to +$1.22B. We’ll combine the data and see where the bulk of Pet Products spending comes from.

We will follow the same methodology that we used in our Total Pet analysis. First, we will look at Pet Products Spending in terms of the same 10 demographic category groups that were responsible for 60+% of Total Pet spending. Then we will look for the best and worst performing segments in each category and finally, the segments that generated the biggest dollar gains or losses in 2018.

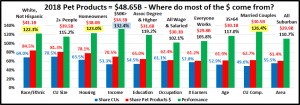

The first chart details the biggest pet product spenders for each demographic category. It shows their share of CU’s, share of pet products spending and their spending performance (spending share/share of CU’s). Although their share of the total products $ may be different from their share of the Total Pet $, the biggest spending groups are the same. The categories are presented in the order that reflects their share of Total Pet Spending. This highlights the differences. In Pet Products spending, the # of earners and occupation are less important while marriage and area type matter more. We should also note that, like Total Pet Spending, Income is the highest performing demographic characteristic. In Pet Products there are 4 groups with a performance rating of over 120%, which is down from 5 last year. This is two less than Total Pet, which indicates that Pet Products spending is spread more evenly across the category segments.

- Race/Ethnic – White, not Hispanic (84.5%, down from 85.7%) They are no longer the largest group but still account for the vast majority of spending in every segment. With a 122.3% performance rating, this category still ranks #4 in terms of importance in Pet Products Spending demographic characteristics. Hispanics, African Americans and Asian American account for over 30% of U.S. CU’s, but they only spend 15% of Pet Products $. Although pet ownership is relatively high in Hispanic American households, it is significantly lower for African Americans and Asian Americans.

- # in CU – 2+ people (81.3%, down from 82.5%) The spending numbers for Pet Products are higher than those for Total Pet, 80.9%. If you put 2 people together, pets very likely will follow. If you have a pet, you must spend money on food and supplies. Their overall performance of 115.2% is lower because of a bad year for 2 person CUs and a great year for singles. Performance decreases as the number of people in the CU increases but all CU sizes with 2 or more people perform above 100% so they all “earn their share”. The key is “It just takes two.”

- Housing – Homeowners (78.1% down from 80.3%). Controlling your “own space” has long been the key to pet ownership, larger pet families and more pet spending. At 123.0% performance, homeownership fell from to second to third place in terms of importance for increased pet products spending. Homeownership increased by 0.6% in 2018, but Renters had a big year in Pet Products spending, +9.0%.

- Income – Over $50K (70.5%, down from 70.9%). Pet Parenting is common in all income groups but money does matter in spending behavior for all industry segments. With a performance rating of 132.4%, (down from 137.7%) CU income is still the single most important factor in increased Pet Products Spending. As a general rule, Higher Income = Higher Pet Products Spending. However, in 2018 much of the decrease in share and performance was due to decreased spending by the middle income groups. $50>99K was down -$2.17B.

- Education – Associates Degree or Higher (65.0%, up from 59.0%). Their performance level also skyrocketed from 109.9% to 119.2%. In 2017 there was a big spending lift by High School Grads with some College. They reversed course in 2018, down -$3.3B. All education levels below Associates Degree spent less, every group with a formal degree spent more. Pet Parents don’t need a College degree, but higher education once again produces increased $.

- Occupation – All Wage & Salary Earners (62.4%, down from 66.1%). Pet ownership is widespread across all segments in this group. The low performance, 102.1%, down from 108.2%, reflects increased balance, but some turmoil. There was a big spending drop from blue-collar workers but a lift from Tech/Sls/Clerical and self-employed.

- # Earners – “Everyone Works” (61.2%, up from 59.9%). Their performance is 105.8%, up from 104.5%. In this group, all adults in the CU are employed. After a great 2017 by CU’s with 2+ people and only one earner, their spending fell $1.7B in 2018. 2 & 3 Earner CUs spent more in 2018, along with No Earner, Singles. Income is a still a priority in Pet Products Spending, but not how many people work to get it.

- Age – 35>64 (61.9%, down from 66.4%). Their performance also decreased from 124.3% to 117.0% and they dropped out of the 120+% performance club. Although the 35>54 group increased spending by $.45B, the 55>64 year old Baby Boomers’ spending fell $3.33B. Increases by every other age group made spending more balanced.

- CU Composition – Married Couples (62.7%, down from 63.1%). Pet parenting and marriage both represent strong commitments. Their performance decreased from 127.5% to 126.4%, but they moved up to 2nd place. Married Couples only spent less. Married w/children spent more but overall, Marriage is very important in Pet Products $.

- Area – Suburban (61.4%, up from 58.2%). Their performance also jumped from 104.7% to 110.7%. Suburban households are the biggest pet spenders. However, population truly mattered in 2018. Suburban and Rural areas under 2500 population were down $2.9B. Suburban areas over 2500 were up $1.5B and Center City was up $0.36B.

Although the biggest spending groups are the same for Pet Products as for Total Pet, there are subtle differences in market share and performance. Money still matters most but how you earn it matters less. It appears that Pet Products Spending is becoming more balanced across almost all demographic categories.

Now, let’s drill deeper and look at 2018’s best and worst performing Products spending segments in each category.

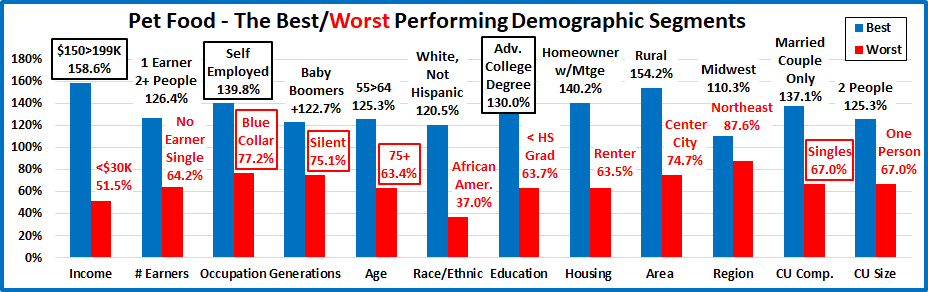

Most of the best and worst performers are the ones that we would expect. However, there are 7 that are different from 2017. That is the same as last year but 2 more than Total Pet. Changes from 2017 are “boxed”.

We should note: Only 1 of the Product winners is different from Total Pet – 55>64 yr olds, who won despite a 30 point drop in performance. The performance of the matching segments is lower than Total Pet, with 1 exception – the Suburbs <2500. Their performance fell from 170% to 160% but they still grabbed 2nd place, behind the $200K+ group.

The average performance of the 2018 Product winners was 134.6%, down sharply from 142.8% – 9 were down. The average for the losers was 63.4%, up from 60.0% – 9 were up. The narrowing of the gap between best and worst reinforces that Pet Products spending is becoming more balanced across America. We should also note:

- Generation – The biggest change was Gen X replaced the Boomers at the top for the first time since….

- Occupation – Self-employed bounced back in income and their spending reflects the increase. Blue Collar workers were the group most affected by the second half drop in Food spending.

- Region – The West held on to the top spot but now only 2 regions are performing above 100%

- Age – The under 25 group got involved with pets and moved out of last place.

Except for Gen X, the winners are the ones we expected, but the gap between top and bottom has narrowed.

It’s time to “Show you the money”. Here are segments with the biggest $ changes in Pet Products Spending.

In this section we will see who drove Pet Products spending down. There is only one repeat from 2017 – the Midwest won again. There was definitely turmoil as 15 Segments switched positions – from first to last or vice versa. However, there are other surprises, like the performance of 65>74 yr olds, Tech/Sales/Clerical workers, Hispanics and Millennials.

- Generation – Millennials edged out Gen X for the top spot and had the biggest lift of any segment in any category.

- Winner – Millennials – Products Spending: $10.61B; Up $1.89B (+21.7%)

- Loser – Baby Boomers – Products Spending: $18.65B; Down $4.55B (-19.6%)

- Comment – Only Boomers spent less, everyone else combined couldn’t make up the difference.

- Area Type – After a big 2017, Rural flipped from first to last.

- Winner – Suburbs >2500 – Products Spending: $21.86B; Up $1.49B (+7.3%)

- Loser – Rural – Products Spending: $5.36B; Down $2.34B (-30.4%)

- Comment –Urbanization? All areas under 2500 pop. down $2.9B; Areas over 2500 pop. up $1.85B.

- Occupation – Another flip, as Blue-Collar workers gave back their big 2017 lift in food.

- Winner – Tech, Sales, Clerical – Products Spending: $8.22B; Up $1.31B (+18.9%)

- 2017: Blue-Collar Workers

- Loser – Blue-Collar Workers – Products Spending: $7.88B; Down $3.34B (-29.8%)

- Comment – The non-manager, white collar workers stepped up and the Self-Employed returned to prominence, but they couldn’t overcome the negative Blue Wave.

- Education – In 2017 Education was less of a factor in Pet Products spending. In 2018 it returned to prominence.

- Winner – BA/BS Degree – Products Spending: $14.16B; Up $1.28B (+9.9%)

- 2017: HS Grad w/some College

- Loser – HS Grad w/some College – Products Spending: $9.05B; Down $3.3B (-26.7%)

- Comment – Once again there is a simple dividing line. If you have a formal degree after HS, you spent more on Pet Products, +$2.3B. All other education segments spent less, -$3.35B.

- Income – The lower Middle Income group was the most impacted by the decline in Food Spending.

- Winner – $150 to $199K – Products Spending: $5.10B; Up $1.22B (+31.5%)

- Loser – $50 to $69K – Products Spending: $6.39B; Down $1.32B (-17.1%)

- Comment – The total middle-income group, $50>99K was down $2.17B. Only the Over $150K and the $30>39K groups generated positive numbers, but not enough to overcome drops from everyone else.

- Housing – The 2017 winner and loser swapped places. This year’s winner also reflects the Millennial influence.

- Winner – Renter – Products: $10.67B; Up $0.88B (+9.0%)

- Loser – Homeowner w/o Mtge– Products Spending: $12.14B; Down $2.78B (-18.6%)

- Comment– The biggest group, Homeowners w/Mtges hasn’t been on the radar for 2 years. They were up $.88B.

- # in CU – A dual flip. The loser reflects the spending drop by Married Couples Only – The Winner: Married, w/1 child.

- Winner – 3 People – Products Spending: $8.08B; Up $0.75B (+10.2%)

- Loser – 2 People – Products Spending: $20.21B; Down $2.31B (-10.3%)

- Comment: All CU sizes spent more on Supplies but only singles and 3 person CUs spent more on Food. The result was that they were the only groups to increase Pet Products spending.

- # Earners – Another dual flip but No Earner, Singles was truly a surprise winner.

- Winner – No Earner, Single– Products Spending: $3.57B; Up $0.72B (+25.1%)

- Loser –– 1 Earner, 2+ CU Products Spending: $11.25B; Down $1.69B (-13.0%)

- Comment – The # of Earners is less of a factor in Pet Product spending, unless you have 2 or more people in your CU. In those cases, (81% of America) only CUs with 2 or more earners spent more.

- CU Composition – One last dual flip. The winner reflects the strong performance by the younger groups.

- Winner – Married, Oldest child <6– Products: $1.94B; Up $0.66B (+51.9%)

- 2017: Married, Couple Only

- Loser – Married, Couple Only – Products: $15.11B; Down $1.57B (-9.4%)

- 2017: Married Oldest Child <6

- Comment – Married Couples only are perennially the best performers but 2018 was a bad year…for Food. They spent more on Supplies. Married Couples with children, oldest child from 6>17 and singles also spent more on both Food and Supplies. The overall lift by Supplies for most groups couldn’t overcome the drop in Food.

- Age – These results show that the Boomers’ product spending drop came from the younger members of the group.

- Winner – 65>74 yrs – Products Spending: $7.15B; Up $0.66B (+10.1%)

- Loser – 55>64 yrs – Products Spending: $11.08B; Down $3.33B (-23.1%)

- Comment: All groups <45 or 65+ spent more on Products. The 45>64 yr olds spent less, but it gets complicated. The under 35 and over 75 groups spent more on both Food and Supplies. 35>64 age range spent less on food but more on Supplies. The “winning” 65>74 yr olds did the opposite. – A very good reason to look at each segment.

- Race/Ethnic – White, Non-Hispanics account for 84.5% of Pet Products’ $, but the minorities are very slowly gaining.

- Winner – Hispanic – Products Spending: $4.25B; Up $0.51B (+13.7%)

- 2017: White, Not Hispanic

- Loser – White, Not Hispanic – Products Spending: $41.09B; Down $1.50B (-3.5%)

- Comment – The spending by African Americans and Asians was essentially flat. However, the Hispanics stepped up with a big lift in Food $. The U.S. is becoming more ethnically/racially diverse. Let’s hope that Pet Products spending does too.

- Region – The Midwest hung on to the top spot by having the biggest increase in Supplies Spending

- Winner – Midwest – Products Spending: $11.12B; Up $0.39B (+3.6%)

- Loser – Northeast – Products Spending: $7.84B; Down $1.08B (-12.1%)

- Comment – Every region spent less on Food but only the Northeast also spent less on Supplies.

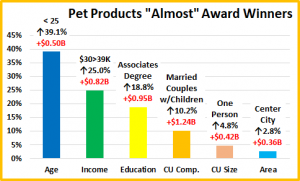

We’ve now seen the “winners” and “losers” in terms of increase/decrease in Pet Products Spending $ for 12 Demographic Categories. 2018 was not a great year for Pet Products Spending due to Food. Many 2017 big spenders like Boomers, Blue Collar Workers, HS Grads with some College and Rural areas did a reversal in 2018. A lot of Segments spent more but their efforts failed to counter the drop in Food spending. Of course, not every good performer can be a winner but some of these “hidden” segments should be recognized for their outstanding effort. In 2018 there were actually quite a lot of them. I’ve narrowed it down to 6. They don’t win an award, but they deserve….

HONORABLE MENTION

Pet Products spending was down $1B in 2018. However, It was a mixed bag. An increase in Supplies couldn’t quite counter the big drop in Food. A significant increase, +39%, came from the <25 group. This bodes well for the future. It also wasn’t “all about money” as the $30>39K income group spent 25% more. Education once again became more important in Pet Products spending but not just college degrees. The Associates Degree group finished second behind the BA/BS group, but had a 19% increase. Marriage is the second most important factor in Pet Products spending but the CUs with Children were the drivers. Regardless of their children’s age, all groups increased spending. We can’t leave out singles. They are the worst performing group but are 30% of U.S. CUs. They stepped up with a 5% increase. Finally, the large Suburbs had the biggest increase, but Center City also spent more. In 2018, more population, at least in the West and Midwest, meant increased spending. Pet Products spending was down in 2018 but it wasn’t all bad news. 50 of 92 segments had an increase, so 54% spent more.

Summary

Spending on Pet Products has been on a roller coaster ride since 2015. Many consumers upgraded to Super Premium Food and cut back on Supplies in 2015. In 2016 they value shopped for Food and Spent some of the saved money on Supplies. In 2017 there was increased availability and value in both segments. More Consumers recognized the opportunity and spent $7B more.

2018 was calm, until the second half when the FDA warning on grain free caused many consumers to downgrade their food and new tariffs on Supplies flattened spending growth. On the surface, big changes weren’t immediately apparent. The demographic groups responsible for most of Pet Products Spending were the same as those in 2017. However, there were changes in their spending share and rankings. Higher Education and Marriage moved up while the number of Earners and Age became less important. In terms of their performance, Income, Marriage and Homeownership stayed on top. However, there were now only 4 groups with 120+% performance as the Age Group dropped out of the club. Total Pet has the same 4, Plus Age and Higher Education. This indicates that Pet Products spending is more balanced than Total Pet in certain demographic categories and this movement continues.

When we looked at the performance of individual segments, the winners were “back to normal” with the groups that we have come to expect through the years, with one major exception – Gen X replaced Baby Boomers as the top performing generation. This was a huge change and the impact became more apparent when we looked at $ changes.

The first thing that we note is that the Boomers spending fell $4.6B. You see the widespread impact as 2017’s big winners like Blue Collar, HS Grads with Some College and Rural “gave it all back” in 2018. In an apparent reaction to the FDA Dog Food warning, they undoubtedly downgraded their Food. This along with the new tariffs on Supplies created incredible turmoil in the 2018 market. 15 of the 24 segments switched positions compared to 2017, from 1st to last or vice versa. However, it wasn’t all bad news. 50 of 92 demographic segments (54%) actually increased Pet Products spending in 2018. Both young and old stepped up. You see this in the performance of winners like Millennials, Renters, 65>74 yr olds, Married with an oldest child under 6 and many more. Although they weren’t able to overcome the massive influence of the Boomers, it bodes well for the future. What about 2019? Hopefully, the Food segment will return to a more normal market. The big question is how will a full year of added tariffs affect Supplies spending?

Finally…The “Ultimate” 2018 Pet Products Spending CU is a married couple, alone. They are in the 45 to 54 age range. They are White, but not of Hispanic origin. At least one of them has an advanced College Degree. Both of them work in their own business, earning over $200K. They still have a mortgage on their house located in a small Suburb in the West.