2020 Pet Services Spending was $6.89B – Where did it come from…?

Next, we will look at Pet Services. It is by far the smallest Segment and after a $1.73B, 20.1% decrease, it got a lot smaller and returned to the level of 2016 – 2017. After the great recession, Services’ annual spending slowly but steadily increased. During this time, the number of outlets offering Services strongly grew as brick ‘n mortar retailers looked for a way to combat the growing influence of online outlets. After all, you can certainly buy products, but you can’t get your dog groomed on the Internet. This created a highly price competitive market for Pet Services. In 2017 there was a slight increase in visit frequency, but Pet Parents just paid less. This resulted in a 1.0% decrease in Services spending. In 2018 consumer behavior changed as a significant number decided to take advantage of the increased availability and convenience of Pet Services and spending literally took off, +$1.95B (+28.9%), by far the biggest increase in history. In 2019 Pet Parents, especially the younger ones, value shopped, and spending turned down $0.10B. That brought us to 2020 and the onset of the pandemic. Because Services outlets were often deemed nonessential, they were subject to restrictions and closures. This drove the huge drop in spending.

We’ve seen that the pandemic caused binge buying in Food, while it slowed the more discretionary Supplies segment. Services spending is arguably the most discretionary of any Pet Expenditure. Let’s look deeper into 2020 demographics.

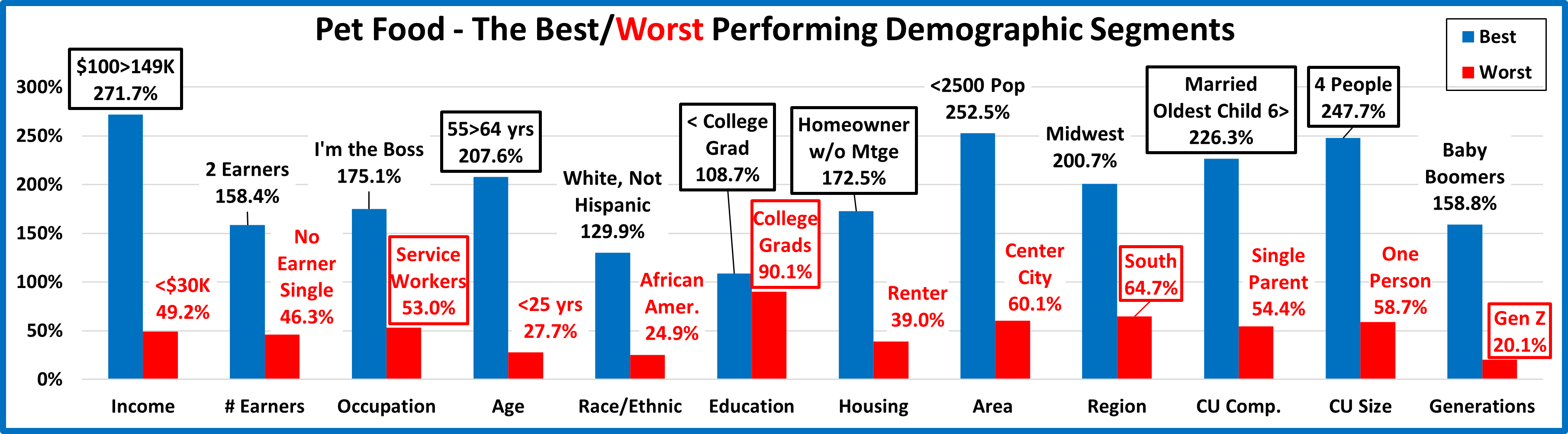

Let’s start by identifying the groups most responsible for the bulk of Services spending in 2020 and the $1.73B decrease. The first chart details the biggest Pet Services spenders for each of 10 demographic categories. It shows their share of CU’s, share of Services spending and their spending performance (Share of spending/share of CU’s). In order to better target the bulk of the spending we had to alter the groups in two categories – education and area. The performance level should also be noted as 5 of 10 groups have a performance level above 120%. This is the same as Supplies and Total Pet but less than the 6 for Veterinary and far less than the 8 for Food. Last year they also had only 5 over 120%, down from their peak of 7 in 2018. This indicates that there continues to be a little less disparity between the best and worst performing segments in 2020. Although performance is down from 2019, Income is still the biggest factor in Services Spending. The categories are presented in the order that reflects their share of Total Pet $ which highlights the differences of the 8 matching groups. One big difference is that higher education is a much bigger factor in Services $.

- Race/Ethnic – White, not Hispanic (87.9%) up from 87.3%.This big group accounts for the vast majority of spending in every segment. Services Spending became slightly less diverse in terms of race and ethnicity in 2020 as their performance grew from 127.4% to 128.5% and they remained in 4th place in terms of importance.

- Housing – Homeowners (78.3%) down from 84.5%. Homeownership is a big factor in spending in all industry segments. The Homeowners’ share of Services fell to the lowest level of any segment in 2020. Their performance plummeted from 132.6% to 119.3% and they dropped out of the 120+% club. Plus, Renters spent 10.5% more.

- # in CU – 2+ people (78.3%) up from 75.9% The share for 2+ CU’s is over 75% for all segments and Services is now 2nd to Food’s 82.5%. Their performance also increased from 108.7% to 111.6% and they moved up to 8th from 9th in importance. Only 4 person CUs spent more. 2+ CUs primarily gained ground because Singles had a 50% bigger drop.

- Area – City/Suburbs >2500 (83.3%) down from 87.1% in share, while performance fell from 106.9% to 102.7%, last place. Services is an Urban Segment so it makes sense that they would be the most impacted by pandemic related restrictions and closures. Led by Rural, the areas under 2500 population actually spent more on Services.

- # Earners – “Everyone Works” (69.9%) up from (67.6%) All adults in the CU are employed. Income is important so a high market share is expected. Their performance grew to 122.0% from 115.6% and they rejoined the 120% club at #5. Only CUs with 3+ Earners spent more. However, when all adults in a CU work, Services become more needed.

- CU Composition – Married Couples (62.8%) up from 61.4%. Married couples are a big share of $ and have 120+% performance in all segments. Their performance increased to 129.4% from 125.7% and they moved up from 5th to 3rd in terms of importance to Services spending. In 2020, kids were the key. Only Married Couples with children over 6 and Single Parents spent more.

- Income – Over $70K (69.2%) down from 75.0% This group’s performance rating is 159.2%, down markedly from 180.7%. However, CU income is still the single most important factor in increased Pet Services Spending. Only the $50>69K and $150>199K income groups spent more. With a $ drop due to closures and restrictions, it’s to be expected that the group that spent the most pre-pandemic would shoulder the brunt of the negative impact.

- Age – 35>64 (62.5%) up from 61.2%. Their performance grew minimally from 117.0% to 117.1% All age groups spent less. The <35 group had the smallest drop, -$0.06B. The 35>64 yr-olds spent -$0.97B less and the $ for 65+ fell -$0.70. The big drop by the oldsters combined with the small drop by the youngsters kept things on par with 2019.

- Education – College Grads (68.5%) down from 72.2% Income generally increases with education. Services spending moves up with each increasing level of education. College Grads spend the most so they were most impacted by the pandemic. Performance fell from 162.6% to 146.6% but a college education is still the 2nd most important factor.

- Occupation– All Wage & Salaried (66.8%) down from 69.8% – Only Self-Employed spent more. All white and blue collar work groups along with Retirees had a 20+% drop in Services’ spending. As expected, the high income Managers & Professionals who regularly spend the most on Services had the biggest drop, -$0.76B. All Wage & Salaried workers’ performance rating decreased from 114.5% to 108.7%. Services spending became a little more balanced in terms of Occupation but for the wrong reason.

We changed 2 of the groups for Services – Education and Area, to better target the biggest spenders. We should also note that Income is still more important to spending in Services than in any other segment but # Earners was the only income related category to gain in importance. Marriage also grew in importance but spending became a little more balanced in most categories with gains by renters and larger CUs.

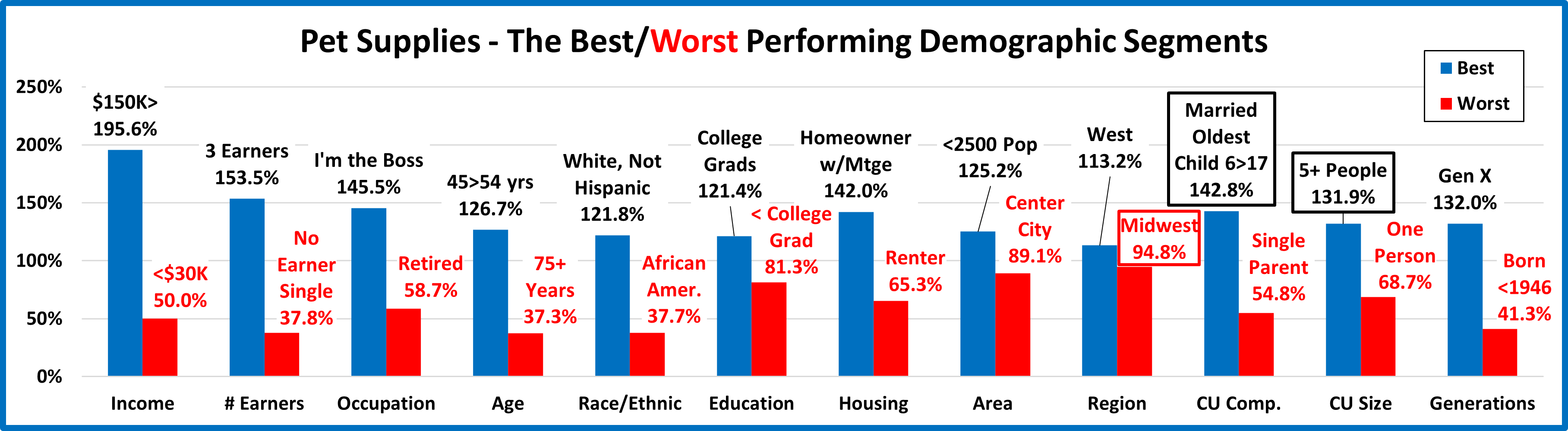

Now, we’ll look at 2020’s best and worst performing Pet Services spending segments in each category.

Most of the best and worst performers are not a surprise. There are 7 that are different from 2019 – 3 of the best and 4 of the worst, the same as last year. The 3 new winners are more family oriented. The high income Gen Xers, including 45>54 yr-olds stayed on top but you can see a move away from the oldest Americans. 75+ yr-olds, those Born before 1946 and No Earner, singles all moved to the bottom. Changes from 2019 are “boxed”. We should note:

- Income is even more important to Pet Services. While the 283.8% Performance by the $150K> group is about the same as last year’s 284.3%, it is still the best performance by any group in any Industry segment.

- # Earners – Winner and loser are new. They are the segments with the highest and lowest incomes. Not a surprise.

- Generation – Gen X retained Top Spot and the oldest group, born before 1946 replaced Millennials at the bottom. Gen X had the only 100+% performance but the younger groups all improved while the older groups lost ground.

- Age – 45>54, the highest income group. is by far the best performer. All groups from 25>64 perform at 100+%. The lowest performers were at both ends of the age spectrum.

- Area –Suburbs 2500> kept the lead in $ and performance. Services is an Urban segment but the gap narrowed a bit in 2020. Suburbs 2500> performed at 109.3, up from 106.9%. Areas <2500 performed at 88.3%, up from 69.6%.

- CU Composition – Children mattered in 2020. Married couples with children and even Single Parents spent more on Services. Marriage is the key. Married Couples only and those with children of any age all perform over 100%.

In Pet Services spending performance, income is still the major factor. After the youth movement in 2018, spending skewed towards older groups in 2019. This was reversed in 2020 as the younger groups basically held their ground while the older CUs drove the big decrease.

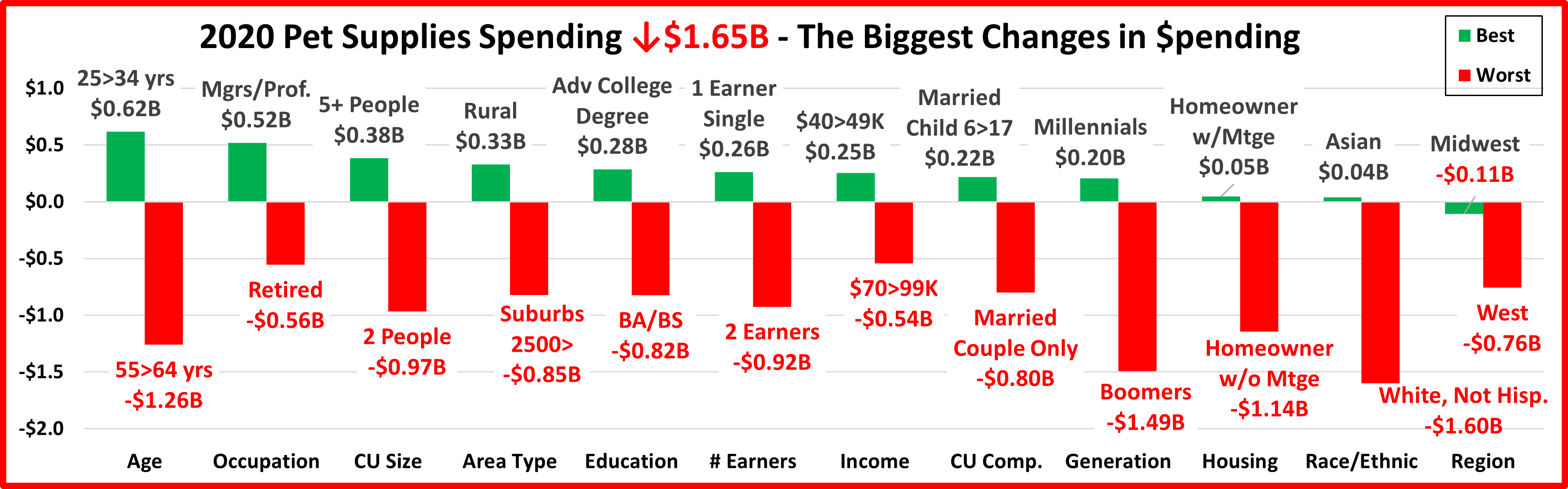

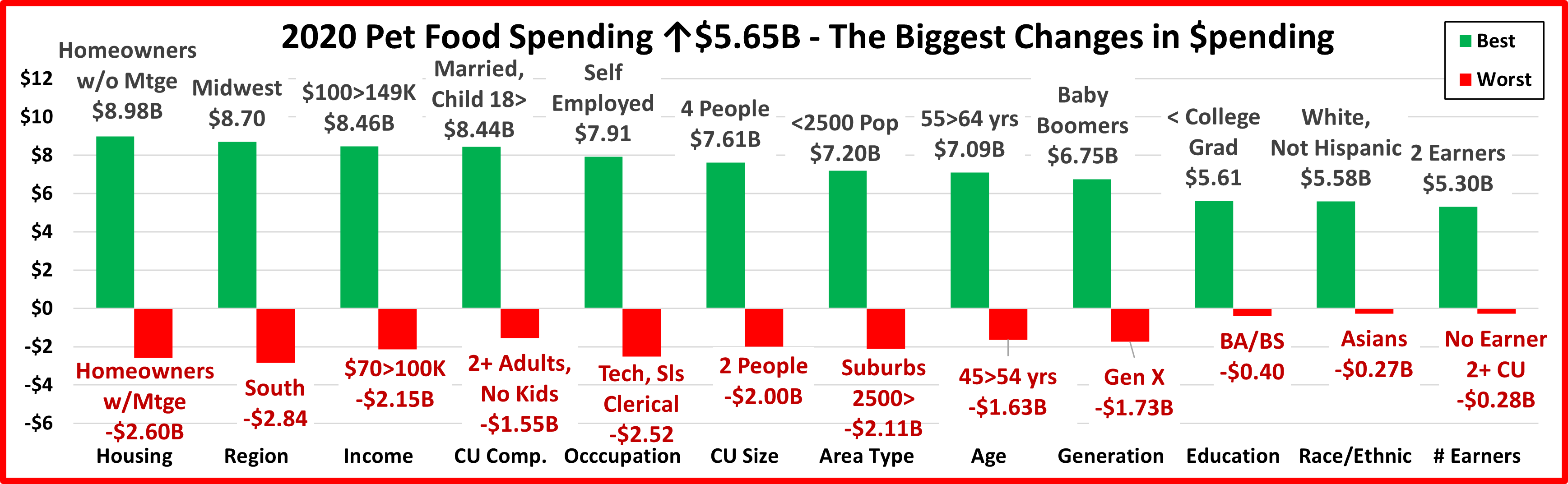

It’s time to “Show you the money”. Here are segments with the biggest $ changes in Pet Services Spending.

The pandemic closures and restrictions drove Pet Services Spending down $1.73B. In this chart you immediately see a difference from last year. In 2020 there were 3 categories in which all segments spent less on Services. In 2019, there were none. In 2019 the changes by the winner and loser tended to cancel the other out. In 2020, the changes by the losers were radically larger than the winners. The tumult that began in 2019 continued in 2020. Again, there were only 2 repeats and 8 of 24 segments switched from first to last or vice versa. In 2019 there were 9 flips. Here are the specifics:

- # in CU – Both the winner and loser are new.

- Winner – 4 People – Pet Services Spending: $1.19B; Up $0.15B (+14.2%) 2019: 5+ People

- Loser – 2 People – Pet Services Spending: $2.49B; Down $1.10B (-30.6%) 2019: 3 People

- Comment: The winners in both 2019 and 2020 reflect the growing strength of the younger generations.

- CU Composition – Married, oldest child 6>17 kept their spot at the top.

- Winner – Married, Oldest Child 6>17 – Services: $1.31B; Up $0.15B (+12.5%) 2019: Married, Oldest Child 6>17

- Loser – Married, Couple Only – Services: $1.80B; Down $0.95B (-34.6%) 2019: Married, Oldest Child <6

- Comment – This reflects the strength of the 25>54 year olds. It also demonstrates the importance of “family”, especially children. All married groups with children over 6 spent more. The loser was more likely to be older.

- Housing – Renters flipped from last to first and were the only segment to spend more.

- Winner – Renter – Services: $1.48B; Up $0.14B (+10.5%) 2019: Homeowner w/o Mtge

- Loser – Homeowner w/Mtge – Services: $3.80B; Down $1.16B (-23.4%) 2019: Renter

- Comment – Homeowners w/mtge spend the most so they have the most to lose and they did.

- Occupation – Mgrs & Professionals, the biggest Services spenders were again the group with the biggest decrease.

- Winner–– Self-Employed – Pet Services Spending: $0.71B; Up $0.14B (+24.3%) 2019: Retired

- Loser – Mgrs & Professionals – Pet Services Spending: $2.79B; Down $0.76B (-21.4%) 2019: Mgrs & Profess.

- Comment – The highest income Self-Employed group spent more in every industry segment.

- Area Type – Big Suburbs flipped from 1st to last. It’s the 1st time since 2016 that Center City didn’t either win or lose.

- Winner – Rural – Pet Services Spending: $0.38B; Up $0.13B (+50.7%) 2019: Suburbs 2500>

- Loser – Suburbs 2500> – Pet Services Spending: $3.33B; Down $0.95B (-22.2%) 2019: Center City

- Comment – Rural was the only group to spend more on Services but they increased spending in all segments.

- Income – The winner flipped from last to first.

- Winner – $50 to $69K – Pet Services Spending: $0.74B; Up $0.12B (+18.6%) 2019: $30>39K

- Loser – $100 to $149K – Pet Services Spending: $1.19B; Down $0.79B (-40.0%) 2019: $50 to $69K

- Comment – Last year we had an up/down spending rollercoaster in income groups. In 2020 only $50>69K & $150>199K spent more. The winning $50>69K group only spent more on Services. The losing group cut back on the more discretionary Supplies and Services to help fund their $9.6B increase in Food & Veterinary.

- Generation – Gen Z is a surprise, but they had an increase because many are just beginning as Pet Parents.

- Winner – Gen Z – Services: $0.13B; Up $0.07B (+118.8%) 2019: Born <1946

- Loser – Boomers – Services: $2.19B; Down $0.59B (-21.3%) 2019: Gen X

- Comment – Boomers had the biggest decrease, but it was only slightly larger than Gen X or those born before 1946. Gen Z spent more but the drop by Millennials was minimal, only -$0.16B, 9% of the total decrease.

- Education – College Degree flipped from 1st to last.

- Winner – HS Grads – Pet Services Spending: $3.30B; Up $0.05B (+8.9%) 2019: Adv. College Degree

- Loser – Adv. College Degree – Services Spending: $0.93B; Down $1.04B (-31.7%) 2019: HS Grad w/some College

- Comment – Only those with no college courses, including those w/o a high school diploma spent more. They only account for 10.6% of Services $ but that’s up significantly from 7.4% in 2019.

- # Earners– Like the Occupation category, the 2 highest income groups provided both the winner and the loser.

- Winner – 3+ Earners – Pet Services Spending: $0.57B; Up $0.04B (+56.0%) 2019: No Earner, Single

- Loser – 2 Earners – Pet Services Spending: $2.25B; Down $0.85B (-14.4%) 2019: 1 Earner, Single

- Comment – All but 3+ Earner CUs spent less. No Earner, Singles had the biggest % decrease, -44.7%.

- Race/Ethnic – Both the 2019 winner and loser flipped.

- Winner – Hispanic – Services: $0.52B; Down $0.01B (-2.6%) 2019: White, Not Hispanic

- Loser – White, Not Hispanic – Services: $6.06B; Down $1.47B (-19.6%) 2019: Hispanic

- Comment– All groups spent less. Hispanics are 2nd in spending but the total minority share of Services $ is 12.1%.

- Age – The 75+ yr olds flipped from 1st to last.

- Winner – <25 yrs – Pet Services Spending: $0.16B; Down $0.03B (-14.3%) 2019: 75+ yrs

- Loser – 75+ yrs – Pet Services Spending: $0.34B; Down $0.42B (-55.1%) 2019: 35>44 yrs

- Comment: In 2018, all age groups spent more on Services. In 2019 all groups under 45 yrs old spent less, while all groups over 45 spent more. In 2020 all age groups spent less but the <35 group was down only -$0.06B while the 35>64 yr olds were -$0.97B and the 65+ group spent -$0.7B less.

- Region – The Midwest lost and has now flipped for three consecutive years.

- Winner – South – Pet Services Spending: $2.65B; Down $0.30B (-10.2%) 2019: Midwest

- Loser – Midwest – Pet Services Spending: $1.23B; Down $0.59B (-32.5%) 2019: Northeast

- Comment – In 2018 all regions spent more. In 2019 it was only the Midwest and West. In 2020 all spent less.

We’ve seen the winners and losers in terms of change in Services Spending $ for 12 Demographic Categories. Income still matters and the younger groups, especially those with children have come to the forefront. Spending has become more balanced but for the wrong reasons. Here’s some data which shows the monumental change from the 2018 peak.

- Sales:

- 2018: $8.72B

- 2019: $8.62B

- 2020: $6.89B

- % Segments Spending More:

- 2018: 88%

- 2019: 49%

- 2020: 21%

- Avg Biggest Increase:

- 2018: $1.04B

- 2019: $0.25B

- 2020: $0.05B

- Avg Biggest Decrease:

- 2018: -$0.02B

- 2019: -$0.27B

- 2020: -$0.89B

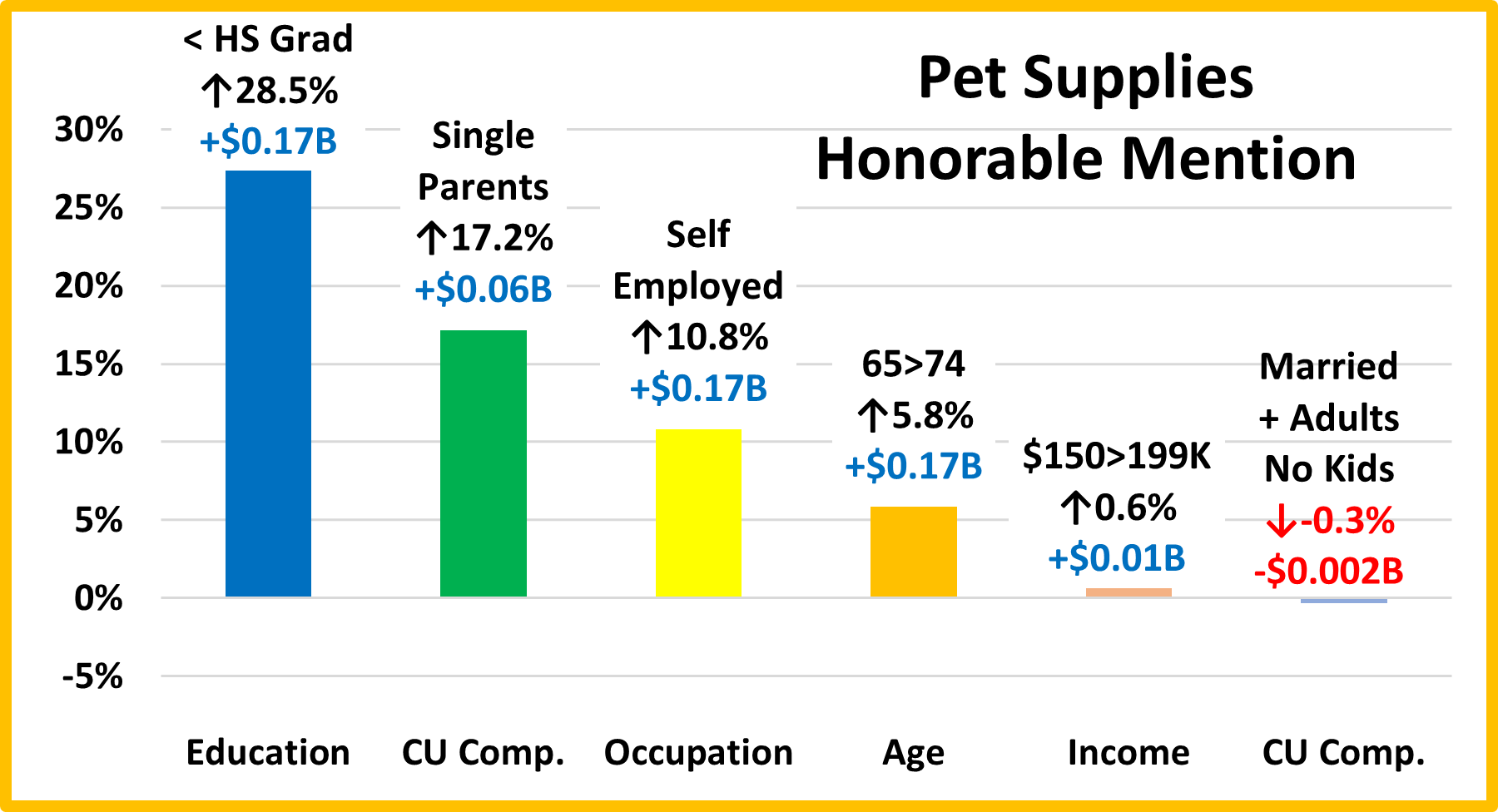

We found the winners in performance and $, but there were others who performed well but didn’t win. They deserve….

HONORABLE MENTION

As you see on the chart, sometimes we had to include both 2nd and the 3rd place finishers to reach our 6 positive segment goal. Higher income is important, but the results were mixed in 2020. The $50>69K group won but there were also positive performances by the $150>199K and $30>39K groups. In a reversal from last year, CUs with kids spent more unless you were married and your oldest child was under 6. This also included single parents. The only area spending increase came from Rural areas but urban areas with a population of 100>249K also posted an increase. A College Degree is more important in Services Spending than in any other industry segment. In 2020 those with only a High School diploma and those who didn’t finish high school were the only 2 education segments to spend more on Services. Only 21% of all demographic segments spent more on Services so our choices for Honorable Mention were limited.

Summary

For years, Services’ spending slowly but steadily increased. However, the number of outlets offering Services was radically increasing. In 2017, this competitive pressure caused Pet Parents to shop for value and spending fell 1%. In 2018, the abundance of outlets and competitive prices finally had their intended impact. Many more consumers took advantage of the convenience of Pet Services and spending literally took off. In 2019 Consumers held their ground at the new higher level but we saw turmoil similar to 2017. Again, value shopping likely contributed to the small decrease.

2020 brought the pandemic and Services outlets were often deemed nonessential so they were subject to restrictions and closures. Services are definitely needed by some groups. However, for most demographics, Services are a convenience and spending is very discretionary in nature. The reduced availability and the pandemic driven focus on the “needed” segments – Food and Veterinary caused a 20% drop in Services $. High Income is still important in Services spending, but we saw mixed results in 2020. However, the $70K> group still has its highest performance in Services.

Performance is an important measurement. There were 5 categories with high performing big groups, the same as 2019. This is equal to Supplies, but less than Veterinary (6) & Food (8). This indicates a little less disparity in Services Spending.

- Income

- Higher Education

- CU Composition

- Race/Ethnicity

- # Earners

The Housing category dropped out and was replaced by # of Earners. These changes were caused by the spending again skewing a little younger. The younger crowd is more likely to have all adults in the CU working. They also are more like to rent than own their home. Renters had the only increase in the Housing segment and pushed Homeownership below the 120% marker. While Spending did move a little younger, Gen X and Boomers are still the top 2 spenders.

A radical increase in the number of outlets caused a competitive market which broadened the appeal of Services and drove a record increase in 2018. Value shopping caused a small decrease in 2019 but Services stayed at the new “normal” level. The pandemic changed all that. Outlets closed and people stayed home so DIY became the new trend even in Pet Services. Services did become more demographically balanced, but it was due to the huge drop in spending by those who normally spent the most, not by any big increases. As Retail America recovers from the 2020 pandemic, we assume that many services outlets will re-open. However, to get back to the previous high level of spending, Pet Parents will also have to move away from DIY and back to “I need help with my pet children, and I have the money to pay for it.” Services were hit the hardest by the pandemic in 2020. We’ll see what happens in 2021.

At Last – The “Ultimate” Pet Services Spending Consumer Unit consists of 4 people – a married couple with 2 kids. The oldest child is 6>17. They are White, but not of Hispanic origin. At least one of them has an advanced College Degree. They are 45 to 54 years old and both work in their own business which generates an income of over $200K. They live in a large suburb of a metropolitan area of 2.5>5 MM in the Western U.S. and are still paying off their mortgage.