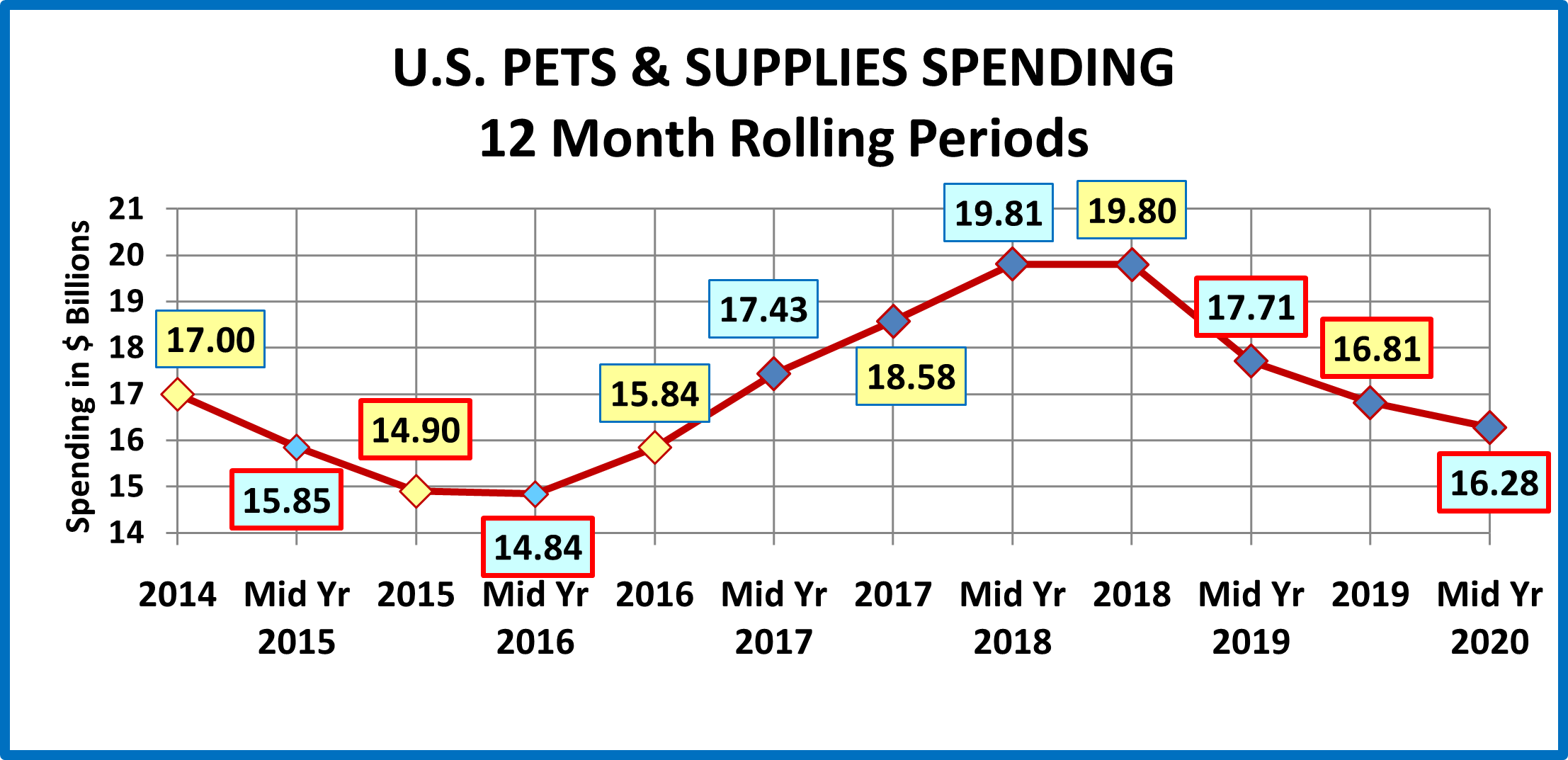

U.S. PET SUPPLIES SPENDING $16.28B (↓$1.43B): MID-YR 2020 UPDATE

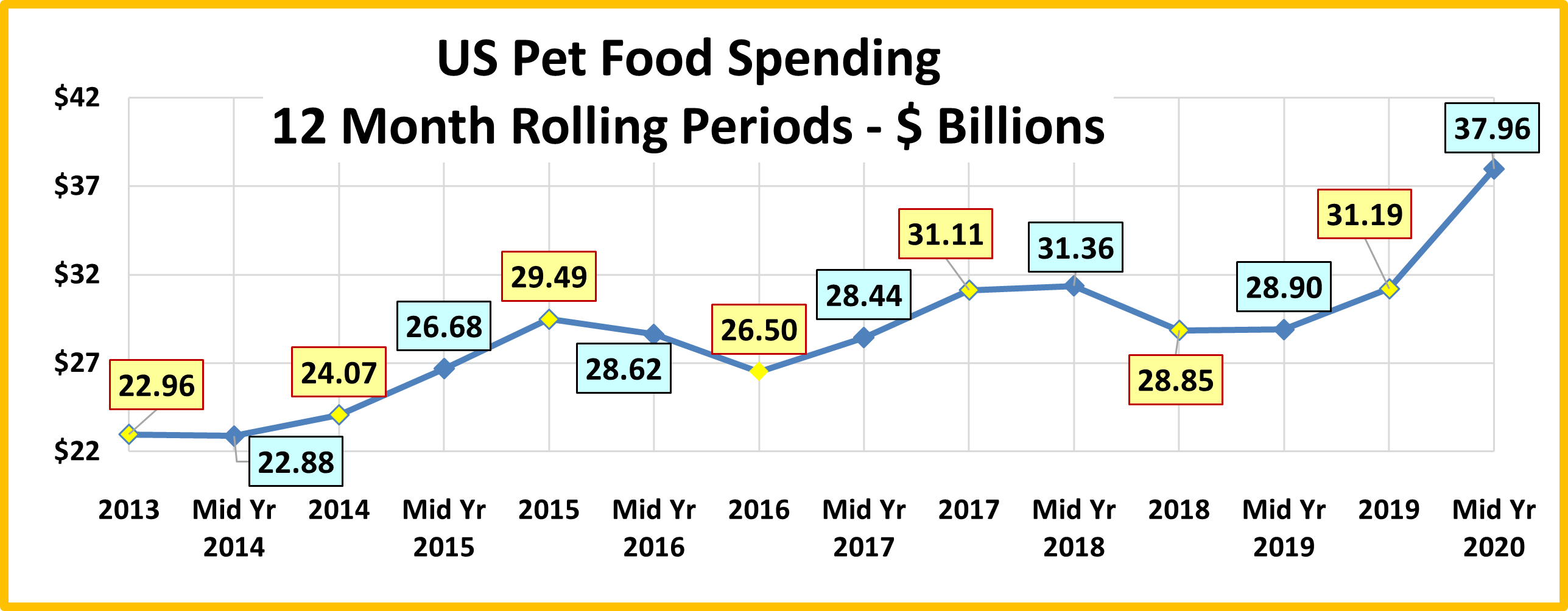

In our analysis of Pet Food spending, we saw that spending grew in the 2nd half of 2019 then skyrocketed in the beginning of 2020 largely due to Pandemic Panic buying. There was no Panic in Pet Supplies and spending continued its steady decline from its 2018 peak. Mid-Year 2020 Pet Supplies spending was $16.28B, down $1.43B (-8.1%). The continuing spending drop in 2020 puts spending in this segment below the level of 3 years ago in Mid-Yr 2017. The following chart should put the recent spending history of this segment into better perspective.

Here are this year’s specifics:

- Mid Yr 2020: $16.28B; ↓$1.43B (-8.1%) from Mid Yr 2019. The -$1.43B came from:

- Jul > Dec 2019: ↓$0.90B

- Jan > Jun 2020: ↓$0.54B

Like Pet Food, Pet Supplies spending has been on a roller coaster ride. However, the driving force is much different. Pet Food is “need” spending and has been powered by a succession of “must have” trends. Pet Supplies spending is largely discretionary, so it has been

impacted by 2 primary factors. The first is spending in other major segments. When consumers ramp up their spending in Pet Food, like upgrading to Super Premium, they often cut back on Supplies. However, it can go both ways. When they value shop for Premium Pet Food, they take some of the saved money and spend it on Supplies. The other factor is price. Pet Supplies prices reached their peak in September of 2009. Then they began generally deflating and in March 2018 were down -6.7% from 2009. Although it is not a hard and fast rule, Price inflation in this largely discretionary segment can retard sales, usually by reducing the frequency of purchase. On the other hand, price deflation generally drives Supplies spending up. Innovation can “trump” both of these influencers. If a new “must have” product is created, something that significantly improves the pet parenting experience, then consumers will spend their money. The perfect example of this is the successive waves of new food trends. Unfortunately, we haven’t seen much significant innovation in the Supplies segment recently.

Recent history gives a perfect example of the Supplies roller coaster. In 2014 Supplies prices dropped sharply, while the movement to Super Premium Food was barely getting started – Supplies spending went up $2B. In 2015, consumers spent $5.4B more on Pet Food. At the same time, Pet Supplies prices went up 0.5%. This was a “killer” combination as Supplies spending fell $2.1B. In 2016 consumers value shopped for Food, saving $2.99B. Supplies spending stabilized by mid-year then increased by $1B in the second half when prices fell sharply. Consumers spent some of their “saved” money on Supplies. Supplies prices continued to deflate throughout 2017. Food spending increased $4.61B in 2017 but this came from a limited group, generally older CUs, less focused on Supplies. The result was a $2.74B increase in Supplies spending. This appeared to be somewhat of a break with the overall pattern of trading $ between segments.

In the first half of 2018 Pet Food spending slowed to +$0.25B. Supplies’ prices switched from deflation to inflation but were only up 0.1% versus the first half of 2017. During this period Supplies Spending increased by $1.23B. Prices began to climb in the second half of 2018 due to impending new tariffs in September. By June 2019 they were 3.4% higher than 2018. The impact of the tariffs on the Supplies segment was very clear. Spending became flat in the second half of 2018, then took a nosedive in the 1st half of 2019, -$2.09B. Prices stayed high for the rest of 2019 and spending fell an additional -$0.9B. In 2020 prices turned up again through March before plummeting, -3.8% by June. Spending dropped an additional -$0.54B. Initially, the pandemic had no positive impact on Supplies spending. We expect that to change in the second half. More time with their pets and lower prices usually means more Supplies spending.

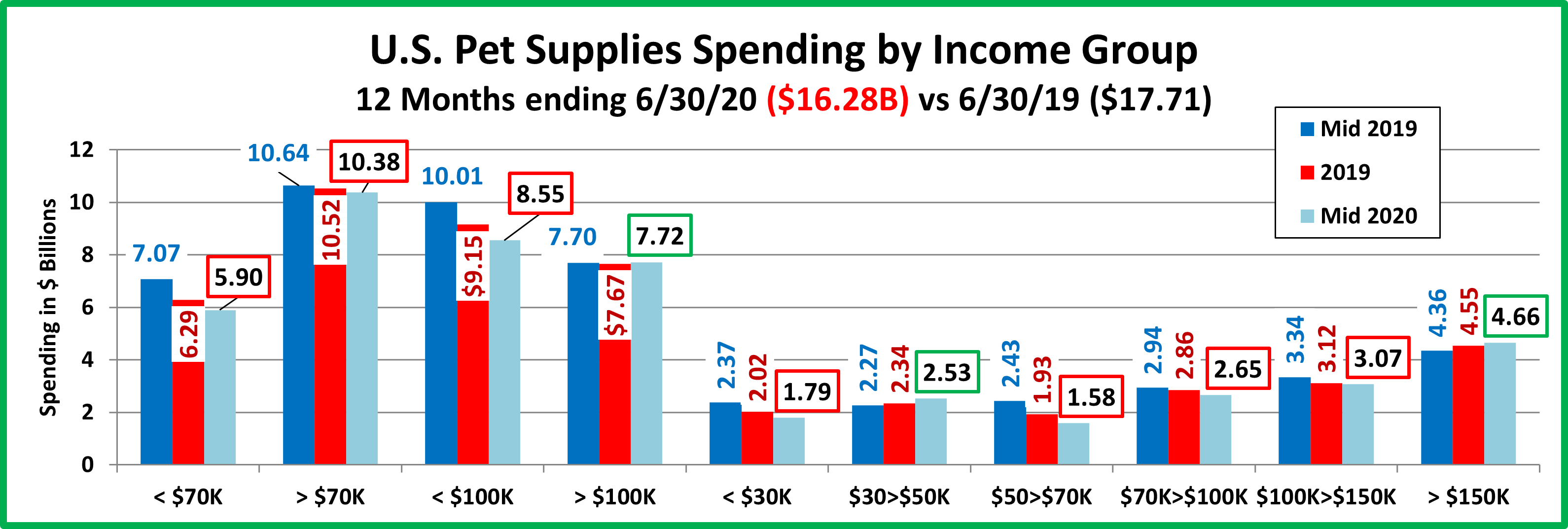

Let’s take a closer look at the data, starting with the two most popular demographic measures – age and income. The graphs that follow will show both the current and previous 12 months $ as well as 2019 yearend. This will allow you to track the spending changes between halves.

The first graph is for Income, which has been shown to be the single most important factor in increased Pet Spending, especially in Pet Supplies and both of the Service segments.

Here’s how you get the change for each half using the $50>70K group as an example:

Mid-yr Total Spending Change: $1.58B – $2.43B = Down $0.85B (Note: green outline = increase; red outline = decrease)

- 2nd half of 2019: Subtract Mid-19 ($2.43B) from Total 2019 ($1.93B) = Spending was down $0.50B in 2nd half of 2019.

- 1st half of 2020: Subtract Total 2019 ($1.93B) from Mid-20 ($1.58) = Spending was down $0.35B in 1st half of 2020.

- I added an under/over $100K measurement to the graph. As you can see, the share of Supplies spending “flips” based upon the $70>$100K group. That means that the “break even” dividing line is probably slightly above the average CU income of $83.8K. The Supplies $ of CUs above average, 33% is equal to the 67% of CUs below average.

- There are only 2 spending patterns in the individual segments – drops in both halves or increases in both halves.

- The decrease in Supplies Spending was widespread across income groups. Both over and under $70K trended down while over $100K was basically flat. The two segments with increases were an unlikely pair – $150K+ and $30>$50K. The higher income group is to be expected but the lower income group is a surprise. $30>50K is the income range for Retirees but it’s not them. It is likely driven by the younger crowd.

- The spending movement, whether up or down, is gradual. In most cases the $ changes in each half are very close.

- The two factors, high prices and the onset of the pandemic had very little impact on the over $100K group. It was basically “business as usual”. The biggest negative came from the <$30K and the $50>$70K groups. Their spending fell -$1.43B, likely due to a reduced purchase frequency. There’s no Supplies binge spending yet. Maybe that will come in the 2nd half of 2020 with the big drop in prices?

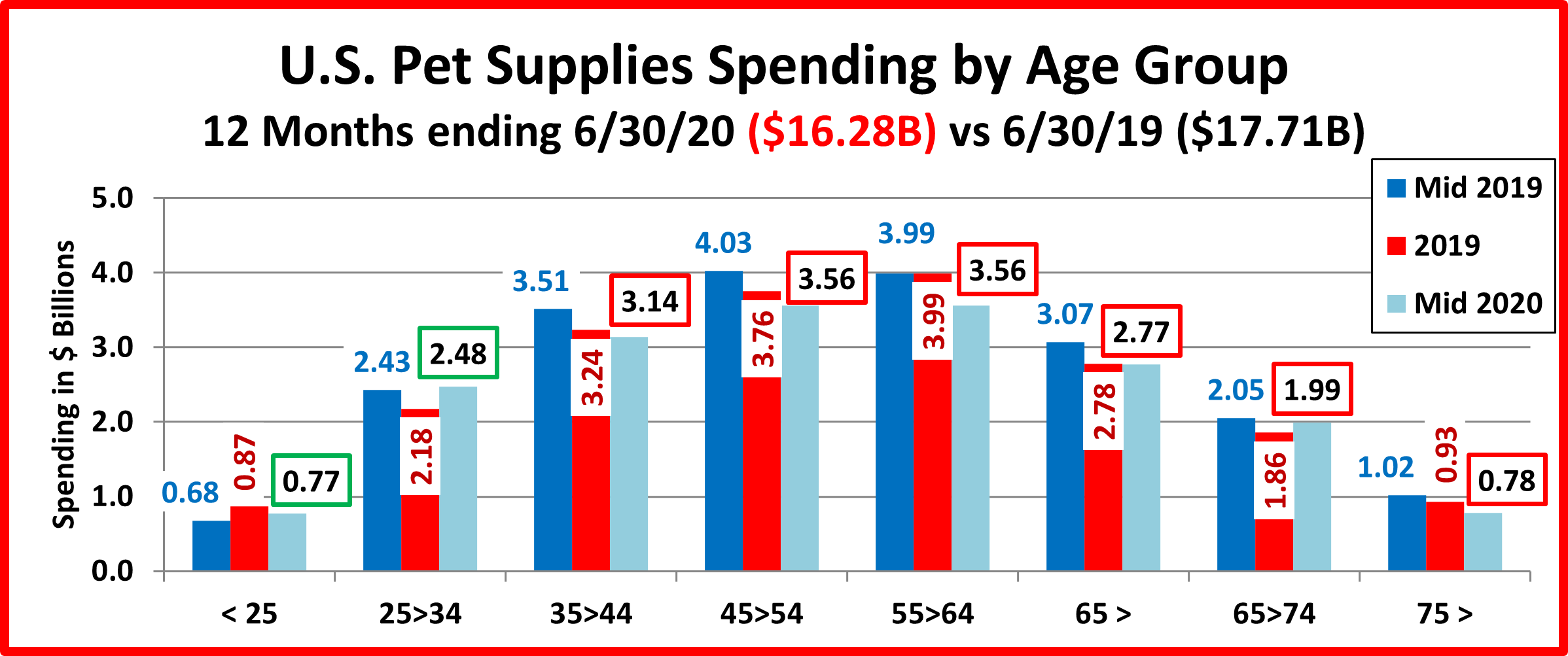

Now let’s look at Pet Supplies spending by Age Group.

- Generally, the over 35 group spent less while under 35 spent a little more but there was a mix of patterns.

- The <25 and 25>34 year olds had opposite patterns for the halves. If there was any “binge” pet supplies spending due to the pandemic, it came from the 25>34 year old Millennials.

- The 35>54 yr olds, Gen X, were down in both halves, probably due to value shopping and slightly reduced frequency.

- The 55> group also had a mixture. The 75> were down in both halves. The Boomers were divided. The 65>74 yr olds had a small pandemic lift while spending dropped sharply for the 55>64 group. This drop was correlated to helping to pay for their huge panic buy of Pet Food.

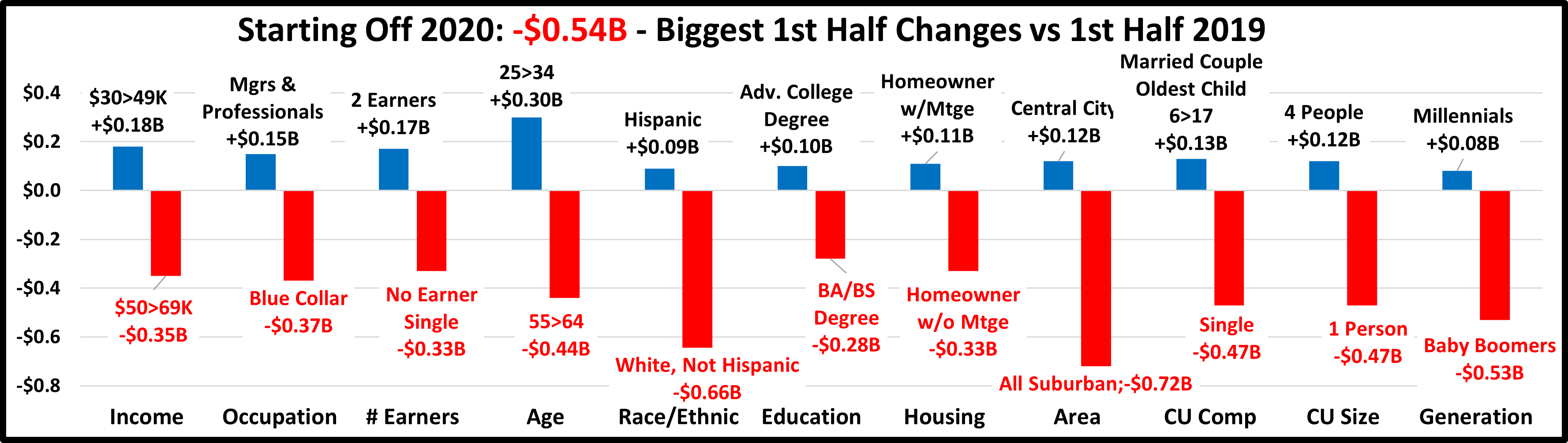

Now let’s look at what is happening in Supplies spending at the start of 2020 across the whole range of demographics. In our final chart we will list the biggest $ moves, up and down by individual segments in 11 demographic categories.

- The first thing that you notice is that the biggest decreases are radically larger than the biggest increases.

- The decrease is widespread but not as bad as last year when in 5 of the 11 categories all segments spent less on Supplies. In the 1st half, 27 segments, 33% spent more. This is up from 22 in the 2nd half of 2019 and much better than 8 last year. There’s a long way to go but things are slowly improving in the Supplies segment.

- There are some “usual suspects” in the winners – Mgrs/Professionals & Adv College Degree and losers – Singles & Blue Collar. There are also some surprise winners – $30>49K & Hispanic and losers – BA/BS & Suburban. However, most of the winners & losers reflect the young vs old pattern that we saw in the age analysis.

- The young positives are reflected in these winners – 25>34, Center City, 4 people, Married, oldest child 6>17, 2 earners and of course, Millennials. The older losers are no earner singles, homeowner w/no mtge, 55>64, suburban and of course, Baby Boomers.

- Here’s a hidden positive. Minorities were +$0.12B in the 1st half. African Americans were down slightly, -$0.01B but Asians and Hispanics spent $0.13B more.

The 24 month Spending winning streak for Supplies which began in the second half of 2016 came to an end in the second half of 2018. During that time spending on Pet Supplies increased $4.97B (+33.5%). It was also widespread across America. Of 82 separate demographic segments, only 1 spent less on Supplies in that period – the Greatest Generation. This 92+ year old group has now become too small to be accurately measured.

What are the market conditions that affect Supplies spending? We have to first note that the world changed for Supplies because of the great recession. Prices have generally deflated since then and spending in the segment became more sensitive to changes in price. Prices go up…spending drops, usually due to reduced purchase frequency. Prices go down… spending turns up. This situation did not exist prior to the recession.

The other factor is spending in other segments, especially Food. Pet spending comes out of “one bucket”. A big increase in one segment can result in a cut back in others and big savings can generate more spending. The recent upgrade to Super Premium Food was such a big $ commitment that it magnified this effect.

In 2018, something new was added – outside influence. The FDA warning on grain free dog food had an immediate, negative impact on the Food segment. For Supplies, it was added tariffs. Prices in the Supplies segment began to turn up in the Spring. By June 2019, they were 3.4% higher than 2018. Supplies spending flattened out then plummeted in the 1st half of 2019. Prices stabilized at the high level and Supplies $ continued to fall. Then came the start of the pandemic. This spurred huge panic buying in food but not supplies. In fact, the huge lift in Food probably contributed to Supplies continued decline. I expect Supplies to rebound strongly in the 2nd half . We’ll get the data in September.