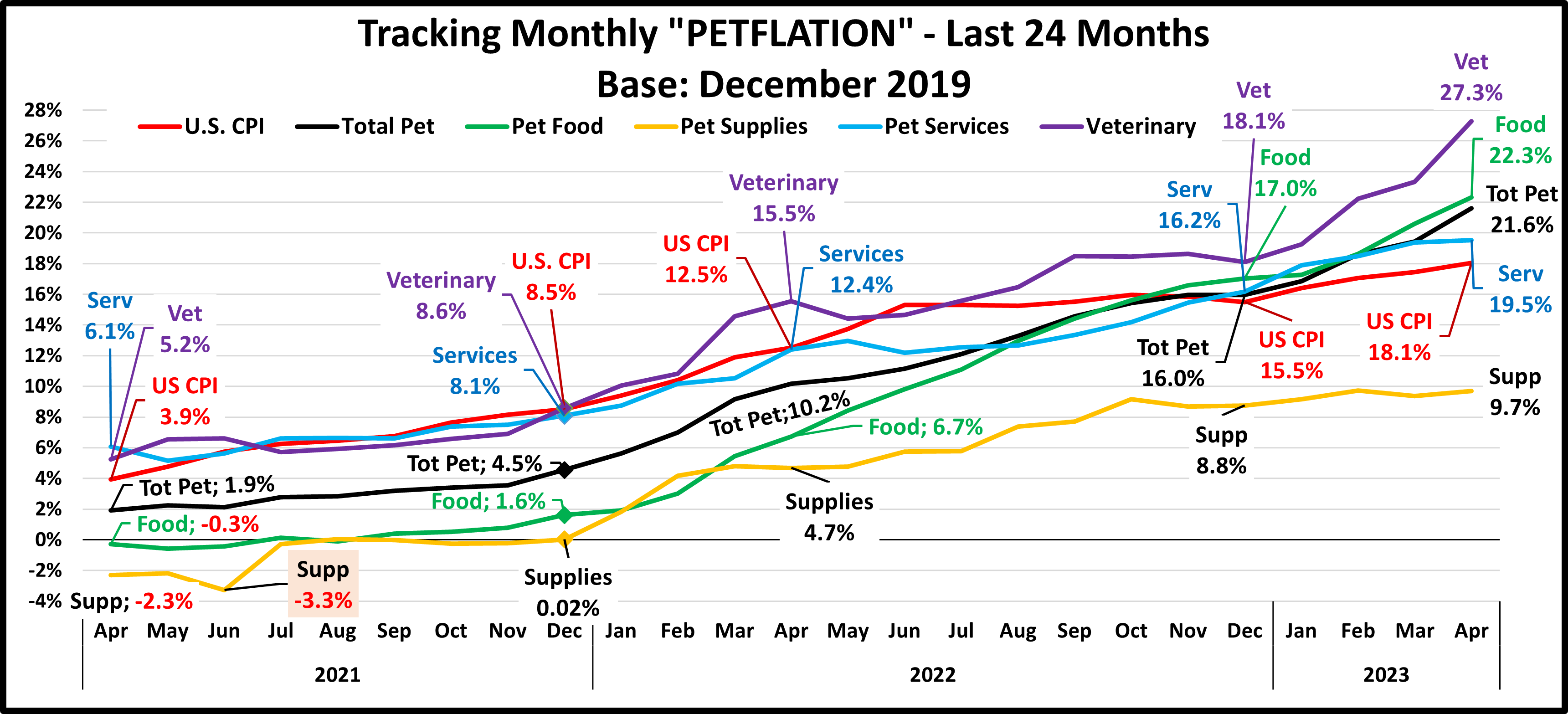

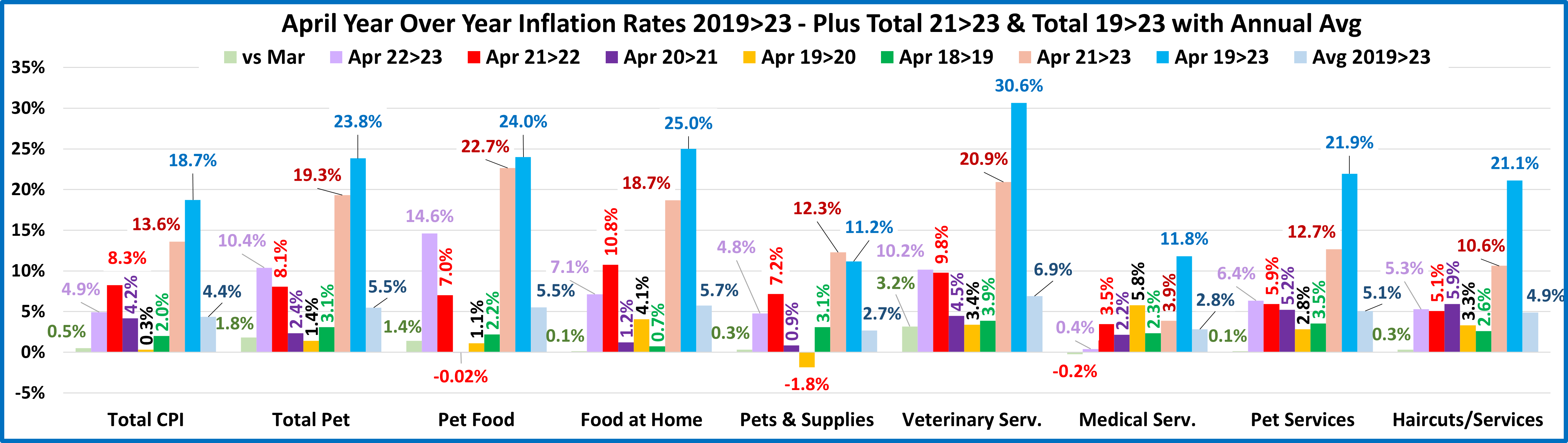

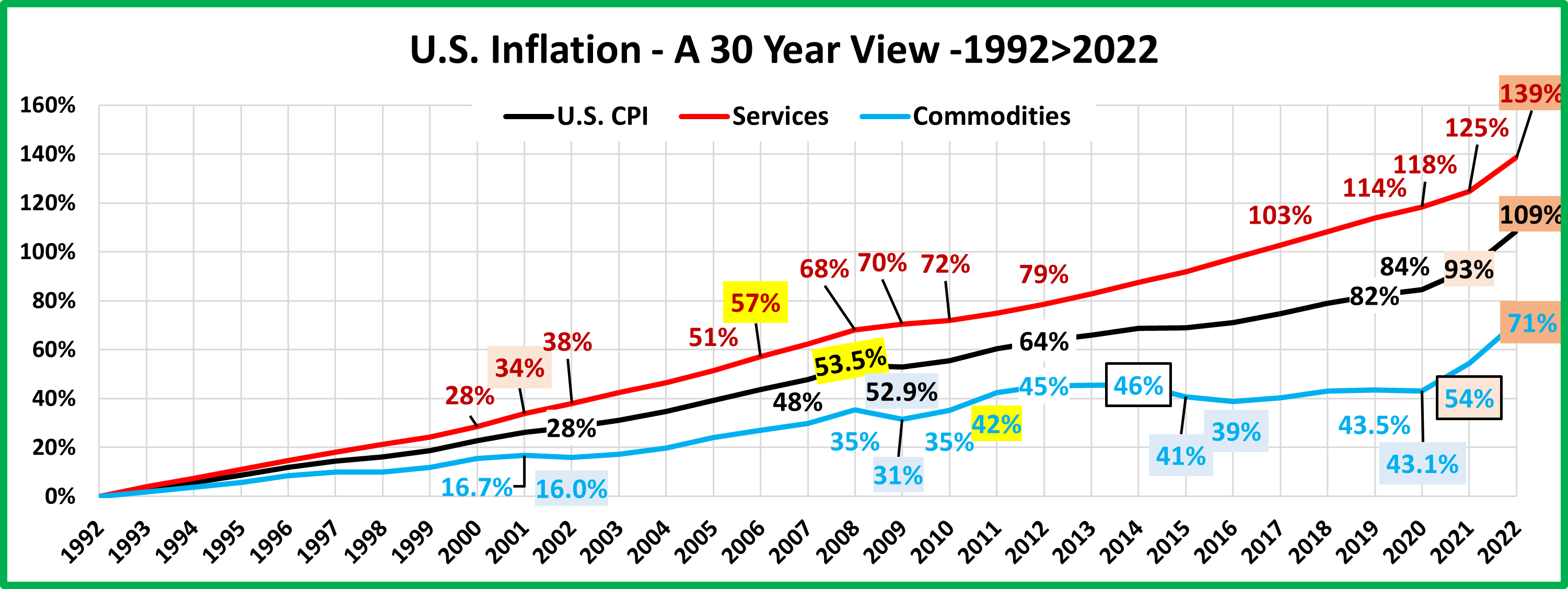

Retail Channel $ Update – March Final & April Advance

While inflation continues to slow, its cumulative effect on consumer spending is now being felt. The rate of sales increases has slowed even more than inflation. This has caused a drop in the amount of product sold in many channels. Some have even turned negative in the actual $ sold vs previous years. A recession is the biggest fear, so we’ll continue to track the retail market with data from two reports provided by the Census Bureau and factor in the CPI from US BLS.

The Census Bureau Reports are the Monthly and the Advance Retail Sales Reports. Both are derived from sales data gathered from retailers across the U.S. and are published monthly at the same time. The Advance Report has a smaller sample size so it can be published quickly – about 2 weeks after month end. The Monthly Final Report includes data from all respondents, so it takes longer to compile the data – about 6 weeks. Although the sample size for the Advance report is smaller, the results over the years have proven it to be statistically accurate with the final monthly reports. The biggest difference is that the full sample in the Final report allows us to “drill” a little deeper into the retail channels.

We begin with the Final Report for March and then go to the Advance Report for April. Our focus is comparing to last year but also 2021 and 2019. We’ll show both actual and the “real” change in $ as we factor inflation into the data.

Both reports include the following:

- Total Retail, Restaurants, Auto, Gas Stations and Relevant Retail (removing Restaurants, Auto and Gas)

- Individual Channel Data – This will be more detailed in the “Final” reports, and we fill focus on Pet Relevant Channels

The data will be presented in detailed charts to facilitate visual comparison between groups/channels. The charts will show 11 separate measurements. To save space they will be displayed in a stacked bar format for the channel charts.

- Current Month change – % & $ vs previous month

- Current Month change – % & $ vs same month in 2022 and 2021.

- Current Month Real change for 2023 vs 2022 and vs 2021 – % factoring in inflation

- Current Ytd change – % & $ for 2023 vs 2022, 2021 and 2019.

- Current Ytd Real change % for 2023 vs 2022, 2021 and 2019

- Monthly & Ytd $ & CPIs for 22>23 and 21>23 which are targeted by channel will also be shown. (CPI Details are at the end of the report)

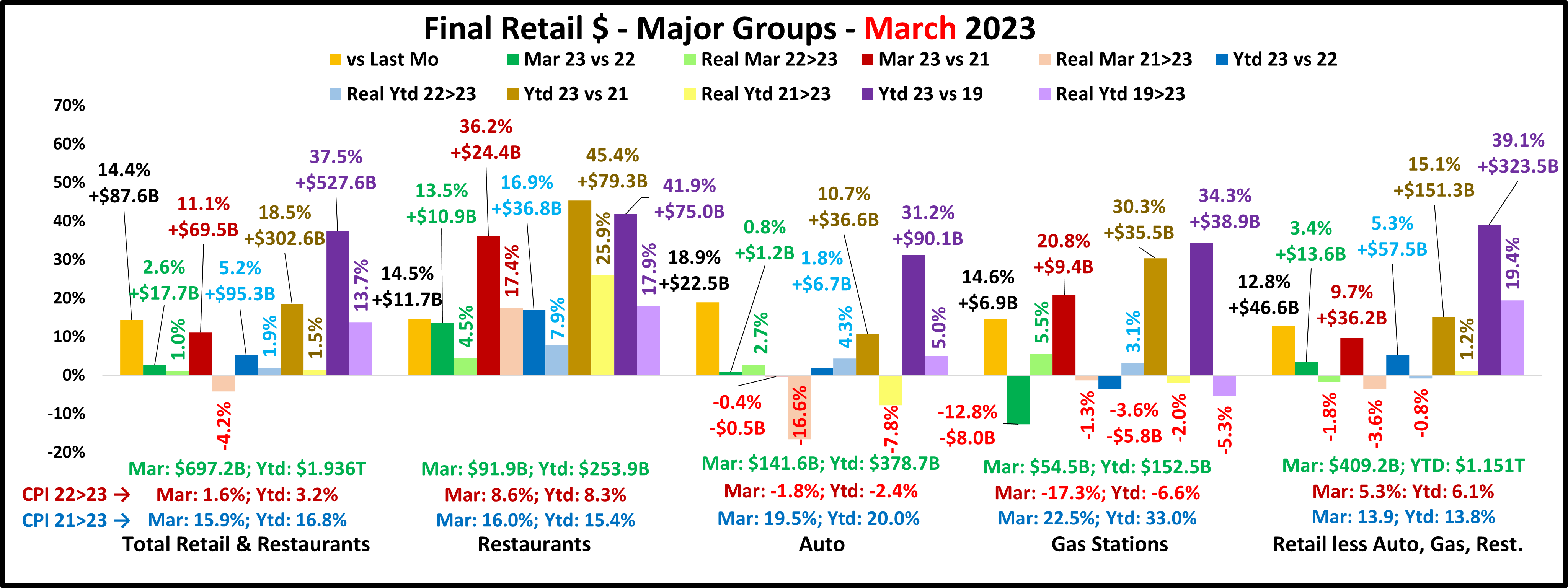

First, the March Final. All were up from last month and only Gas Stations and Auto had any decreases vs 21 or 22. When you consider inflation, Auto was down vs 21 and Gas Stations vs 19 & 21. Total Retail & Relevant retail were really down vs Apr 21 but Relevant Retail was also down for the month & Ytd vs 2022. (All $ are Actual, Not Seasonally Adjusted)

The March Final is $6.0B less than the Advance Report. Specifically, Restaurants: -$4.6B; Gas Stations: -$0.7B; Auto: +0.9B; Relevant Retail: -$1.6B. Sales were up from February as expected and consumers continue to spend more vs last year in all but Gas Stations. In fact, Total Retail, Restaurants & Relevant Retail were positive in all actual Sales measurements vs 22, 21 & 19. Auto was “really” down vs 21 and Gas Stations are really down Ytd vs 21 & 19. The most significant change is that the real sales for Relevant Retail vs 2022 turned negative again. It has now been down for 11 of the last 12 months. They are still in 1st place in performance since 2019 but only 50% of their growth is real.

Now, let’s see how some Key Pet Relevant channels did in March in the Stacked Bar Graph Format

Overall– All 11 were up from Feb, but vs 22, 10 were up vs Mar and Ytd. 8 were “really” down monthly & 6 Ytd. Vs 2021, 7 had increases but only 3 monthly were real and 4 Ytd. Vs 2019, Office/Gift/Souvenir was the only real negative.

- Building Material Stores – The pandemic focus on home has produced sales growth of 38.7% since 2019. Prices for the Bldg/Matl group have inflated 23.4% since 2021 which is having an impact. HomeCtr/Hdwe stores are down for the month vs 22 & 21 & Ytd vs 22. Farm Stores are a little better, only down vs March 2021. However, both have all negative real numbers vs 2022 & 2021. Importantly, only 22.1% of their 19>23 lift was real. It was only this high because most of the lift came prior to the inflation wave. Avg 19>23 Growth: HomeCtr/Hdwe: 8.2%, Real: 2.2%; Farm: 10.6%, Real: 4.5%

- Food & Drug – Both channels are truly essential. Except for the pandemic food binge buying, they tend to have smaller fluctuations in $. However, they are radically different in inflation. The rate for Grocery products is over 2 times higher than for Drugs/Med products. Drug Stores are positive in all numbers vs 22, 21 & 19 and 75% of their growth since 2019 is real. While the $ are up for Supermarkets their 2023 real sales are down vs 2022 & 2021 and just slightly positive vs 2019. Only 10% is real growth. Avg 19>23 Growth: Supermarkets: +6.4%, Real: +0.7%; Drug Stores: +5.1%, Real: +3.8%.

- Sporting Goods Stores – They also benefited from the pandemic in that consumers turned to self-entertainment, especially sports & outdoor activities. Sales are up 30% from February, slightly positive vs 2022 but down vs 2021. Real sales are only positive Ytd vs 2022. Their current inflation rate is 1.1%, a big drop from +5.4% in 21>22 and +6.5% in 20>21. The result is that 59% of their 45.4% lift since 2019 is real. Their Avg 19>23 Growth Rate is: +9.8%; Real: +6.1%.

- Gen Mdse Stores – All channels are up vs February. In actual sales, the only negative was Disc Dept Stores Ytd vs 2021. In real sales, the only positives were in monthly & Ytd sales for $/Value Stores vs 2022. Disc Dept Stores have the worst performance of any channel in all measurements and only 17% real growth since 2019. The other channels average 36%. Avg 19>23 Growth: SupCtr/Club: 6.1%, Real: 2.2%; $/Value Strs: +6.4%, Real: +2.4%; Disc. Dept.: +3.3%, Real: +0.6%

- Office, Gift & Souvenir Stores – Actual sales are up from February and in all measurements vs 2022, 2021 & 2019. However, their real sales growth is still down monthly vs 2022 & 2021 and Ytd vs 2019. Their recovery didn’t start until the spring of 2021, but they are making progress. Avg Growth Rate: +1.2%, Real: -1.5%

- Internet/Mail Order – Sales are up +13.0% from February and above $100B, a monthly record. They are positive for all measurements, but their growth rate is only 43% of their average since 2019. However, 80% of their 101.3% growth since 2019 is real. Avg Growth Rate: +19.1%, Real: +16.0%. As expected, they are by far the growth leaders since 2019.

- A/O Miscellaneous – Pet Stores are 22>24% of total $. In May 2020 they began their recovery which reached a record level of $100B for the first time in 2021. In 2022 their sales dipped in January, July, Sept>Nov, rose in December, fell in Jan>Feb, then turned up in March. Real sales are down vs March & Ytd 2022, but all other measurements are positive. They are still the % increase leaders vs 2021 and 73% of their 59.5% growth since 2019 is real. Average 19>23 Growth: +12.4%, Real: +9.4%. They remain 2nd in growth since 2019 to the internet. I’m sure that Pet Stores are contributing.

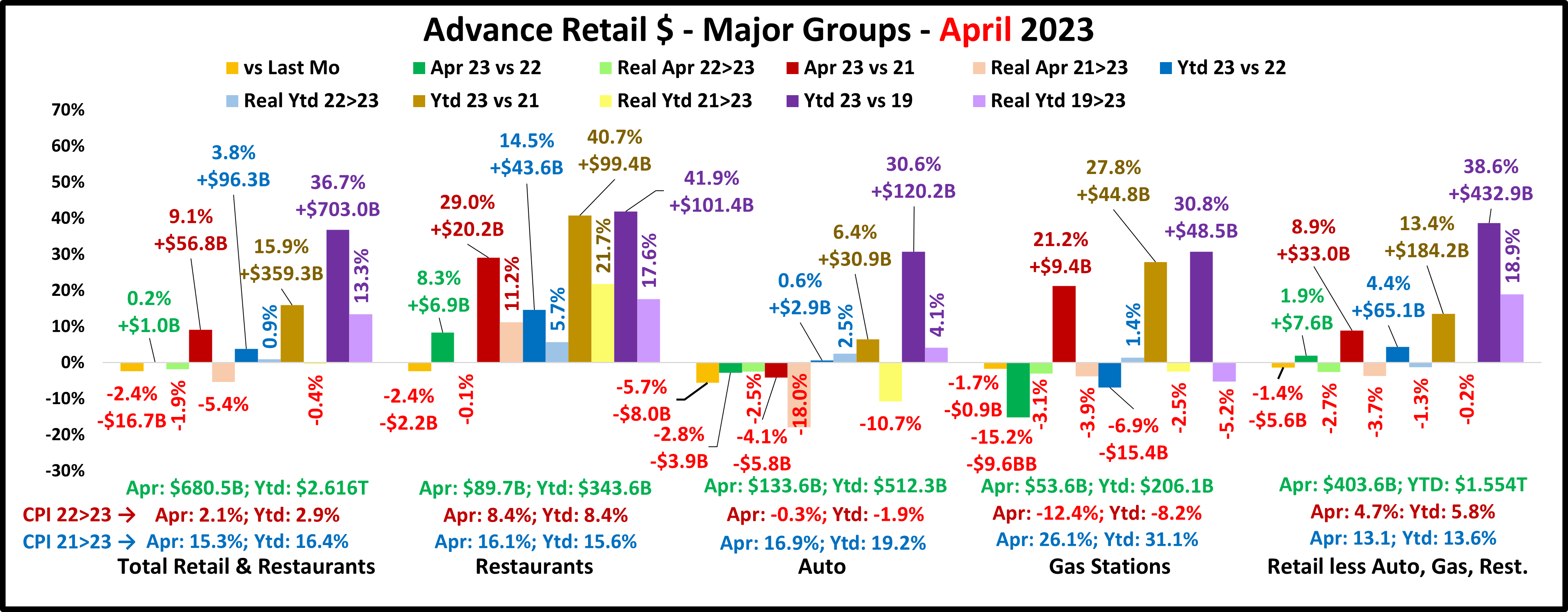

There is no doubt that high inflation is an important factor in Retail. In actual $, 10 channels reported increases in sales vs 2022 and 7 vs 2021. When you factor in inflation, the number with any “real” growth drops to 3 vs 2022 & 2021. Inflation is slowing but not as fast as sales increases. Inflation has increased its impact at the retail channel level. Recent data indicates that Inflation again slowed a little. Let’s look at the impact on the Advance Retail $ales for April.

Since 2019, we have seen the 2 biggest monthly drops in history but a lot of positives in the Pandemic recovery. Total Retail reached $700B in a month for the first time and broke the $7T barrier in 2021. Relevant Retail was also strong as annual sales reached $4T in 2021 and all big groups set annual $ales records. In 2022 radical inflation was a big factor with the largest increase in 40 years. At first, this reduces the amount of product sold but not $ spent. Total Retail hit $8T and all groups again set new annual records in 2022. In 2023, sales fell for all groups in Jan>Feb, rose in March then fell in April. Except for dips by Auto & Gas Stations, all actual sales are slightly positive. The biggest change is that of the groups’ total of 20 “real” sales measurements vs 22 & 21, only 6 are positive. 3 of those are from Restaurants but even their sales vs April 2022 are really down. This clearly shows the growing impact of cumulative inflation.

Overall – Inflation Reality – The April $ increase rate for all vs 2022 was below the inflation rate, producing negative real numbers. You also see the impact of cumulative inflation as real sales are down for all but Restaurants vs 2021. Restaurants still have the strongest performance vs 2022, 2021 & 2019. The biggest negative is in Relative Retail. Monthly & Ytd Real sales are down vs 2022 & 2021. Consumers pay more but buy less.

Total Retail – Every month since June 2020 has set a monthly sales record. December 2022 $ were $748.9B, a new all-time record. Sales dipped in Jan>Feb, rose in March then fell in April. Inflation is slowing but so is sales growth. Sales are up 0.2% vs last year. That’s the lowest rate since the -6.7% drop in May 2020. Also, real sales are down vs April 22 as well as monthly and Ytd vs 21. Plus, only 36% of the 19>23 growth is real. Inflation is slowing but it has been above 4% since March 2021. We are starting to see the cumulative impact. Avg 2019>23 Growth: +8.1%, Real: +3.2%.

Restaurants – They were hit hard by the pandemic and didn’t begin recovery until March 2021. However, they have had strong growth since then, setting an all-time monthly record of $91B in December and exceeding $1T in 2022 for the 1st time. They are the best performing big group vs 22, 21 & 19. Inflation decreased to 8.4% in April from 8.6% last month but is still +16.1% vs 21 and +20.6% vs 19. 42.0% of their 41.9% growth since 19 is real but that is less than the 53.3% of their 40.7% growth since 21. Recovery started late but inflation started early. Avg 2019>23 Growth: +9.1%, Real: +4.1%. They just account for 13.1% of Total Retail $, but their performance improves the overall retail numbers.

Auto (Motor Vehicle & Parts Dealers) – This group actively worked to overcome the stay-at-home attitude with great deals and a lot of advertising. They finished 2020 up 1% vs 2019 and hit a record $1.48T in 2021 but much of it was due to skyrocketing inflation. In 2022 sales got on a rollercoaster. Inflation started to drop mid-year, but it caused 4 down months in actual sales which are the only reported sales negatives by any big group in 2021>2022. This is bad but their real 2022 sales numbers were much worse, down -8.2% vs 2021 and -8.9% vs 2019. 2023 started off a little better but got worse in March & April. April $ are down vs 22 & 21 and Ytd Real sales vs 2021 are also down. Their Ytd real sales vs 19 are still positive but slowing, despite continued deflation. Avg 2019>23 Growth: +6.9%, Real: +1.0%.

Gas Stations – Gas Stations were also hit hard. If you stay home, you drive less and need less gas. This group started recovery in March 2021 and inflation began. Sales got on a rollercoaster in 2022 but reached a record $583B. Inflation started to slow in August and prices slightly deflated in Dec & Feb then dropped 17% in Mar and 12.4% in April. However, prices are still +31.0% vs 21. The deflation actually caused monthly & Ytd sales vs 22 to drop but Ytd real sales are up. However, all real sales vs 21 & 19 are still down. Avg 2019>23 Growth: +6.9%, Real: -1.3%.The numbers show the cumulative impact of inflation and demonstrate how strong deflation can be both a positive and a negative.

Relevant Retail – Less Auto, Gas and Restaurants – They account for 60+% of Total Retail $ in a variety of channels, so they took many different paths through the pandemic. However, their only down month was April 2020 and they led the way in Total Retail’s recovery. Sales got on a roller coaster in 2022 but all months in 2022 set new records with December reaching a new all-time high, $481B, and an annual record of $4.81T. In 2023, Jan & Feb had normal drops. Sales in March turned up then fell in April. All actual sales are up vs 22, 21 & 19 but all real sales vs 22 & 21 are down. Real sales vs last year have now been negative in 12 of the last 13 months. 49% of their 19>23 $ are real, which shows that Inflation is a problem that began in 2022. Their Avg 2019>23 Growth is: +8.5%, Real: +4.4%. The performance of this huge group is critically important. This is where America shops. The fact that real sales are down again is bad news.

Inflation is slowing slightly but the impact is growing. Sales increases are slowing, and the fact that 70% of all real sales measurements vs 22 & 21 are negative is very concerning. Restaurants are still doing well while Auto & Gas Stations are still struggling despite ongoing deflation. However, the biggest concern is Relevant Retail. They have definitely returned to Inflation Phase II – Consumers spend more but the amount bought decreases. The Apr sales increase rate is the lowest since the pandemic drop in April 20. This can lead to Phase III, when actual sales drop. Let’s hope for a turnaround.

Here’s a more detailed look at April by Key Channels in the Stacked Bar Graph Format

- Relevant Retail: Avg Growth Rate: +8.5%, Real: +4.4%. Only 3 channels were up from March but 5 were up vs 22 & 7 vs 21. Only 3 had a “real” increase vs 22 and 5 vs 21. The negative impact of inflation is visible in both actual & real data.

- All Dept Stores – This group was struggling before the pandemic hit them hard. They began recovery in March 2020. Their Actual $ are down from March but up for all comparisons but vs April 22. However, their real sales are down in all measurements, even vs 2019. Avg 2019>23 Growth: +1.0%, Real: -1.7%.

- Club/SuprCtr/$ – They fueled a big part of the overall recovery because they focus on value which has broad consumer appeal. $ales are up from March and in all other measurements. Their real sales are also up slightly in all measurements but Ytd vs 21. Only 36% of their 28.5% 19>23 lift is real – the impact of inflation. Avg Growth: +6.5%, Real: +2.5%.

- Grocery- These stores depend on frequent purchases, so except for the binge buying in 2020, their changes are usually less radical. $ are down from March but up in all measurements vs 22, 21 & 19. However, inflation hit them hard. Real sales are down for all but Ytd vs 2019 and only 9.6% of the growth since 2019 is real. Avg Growth: +6.4%, Real: +0.7%.

- Health/Drug Stores – Many stores in this group are essential, but consumers visit far less frequently than Grocery stores. Sales are down from March but up in all other measurements, both actual and real vs 22, 21 & 19. Their inflation rate has been low so 75% of their 22.1% growth from 2019 is real. Avg 2019>23 Growth: +5.1%, Real: +3.9%.

- Clothing and Accessories – Clothes initially mattered less when you stayed home. That changed in March 21 with strong growth through 2022. Actual Sales are down from March and vs April 22. Real sales are down vs April 22 & 21 and Ytd vs 22. However, 62% of their 2019>23 growth is real. Avg 2019>23 Growth: +3.7%, Real:+2.4%

- Home Furnishings – In mid-2020 consumers’ focus turned to their homes and furniture became a priority. Inflation has slowed but was very high in 2022. Sales are down from March and in all measurements but Ytd vs 21 & 19. Their real sales are all down vs 22 & 21 and only 8% of their 19>23 growth is real. Avg 2019>23 Growth: +4.7%, Real: +0.4%.

- Electronic & Appliances – This channel has many problems. Sales fell in Apr>May of 2020 and didn’t reach 2019 levels until March 2021. $ales are down vs March and in all measurements but Ytd vs 21 & 19. However, real sales are up for all but vs April 22. This happened because of strong deflation, -6.4>-7.6%. Avg 2019>23 Growth: +0.6%, Real: +2.4%.

- Building Material, Farm & Garden & Hardware –They truly benefited from the consumers’ focus on home. In 2022 the lift slowed as inflation grew to double digits. Sales are up 4% vs last month – 2 consecutive increases. The only other positives are Ytd vs 21 & 19. They have the highest Inflation of any channel so real sales are negative in all but Ytd vs 2019. Also, just 22% of their % sales growth since 2019 is real. Avg 2019>23 Growth is: +7.9%, Real: +1.9%.

- Sporting Goods, Hobby and Book Stores – Consumers turned their attention to recreation and Sporting Goods stores sales took off. Book & Hobby Stores recovered more slowly. $ales are down from March and in all other measurements but Ytd vs 22 & 19. Real sales are all down except vs 19. Just 3 months ago all measurements were positive. Their inflation is lower than most groups so 62% of their growth since 2019 is real. Avg 2019>23 Growth: +6.5%, Real: +4.1%.

- All Miscellaneous Stores – Pet Stores have been a key part of the strong and growing recovery of this group. They finished 2020 at +0.9% but sales took off in March 21 and have continued to grow. Sales are up from March and for all but real April 23 vs 22. They still have the biggest increase vs 2021 and vs 2019 they are 2nd only to NonStore. 68% of their 42.8% 19>23 growth and even 50% of their 21>23 growth is real. Their Avg 19>23 Growth is: 9.9%, Real: 7.0%.

- NonStore Retailers – 90% of their volume comes from Internet/Mail Order/TV. The pandemic accelerated online spending. They ended 2020 +21.4%. The growth continued in 2021 as sales exceeded $100B for the 1st time and they broke the $1 Trillion barrier. Their growth slowed significantly in 2022 and now 2023. $ are down from March but all measurements are positive. 78% of their 89.2% growth since 2019 is real. Their Avg Growth: +17.3%, Real: +14.1%.

Note: Almost without exception, online sales by brick ‘n mortar retailers are recorded with their regular store sales.

Recap – The Retail recovery from the pandemic was largely driven by Relevant Retail and by the end of 2021 it had become very widespread. In 2022, there was a new challenge, the worst inflation in 40 years. Overall, and in most product categories it has slowed in Jul>Apr which should improve the Retail Situation. Sales were down from March for all big groups and 8 of 11 smaller channels. While Inflation continues to slow in most channels, some channels like Auto, Gas Stations, Grocery and Bldg Material stores still have high cumulative inflation rates so they are still struggling. Only a few channels are doing well. The new problem is that the sales increase rate vs 2022 for many channels has slowed and is now below the lower inflation rate. This is evident in Relevant Retail as Real sales are now negative for all but Ytd vs 2019. However, actual & real sales vs 22 are now negative for most channels. Only 3 – NonStore, Clubs/$ Strs & Health Care are both actually and really positive vs 22. We seem to have returned to Inflation, Phase II, increased $ales but a decrease in the amount sold. However, some channels may be moving to Phase III, when actual $ales also decrease.

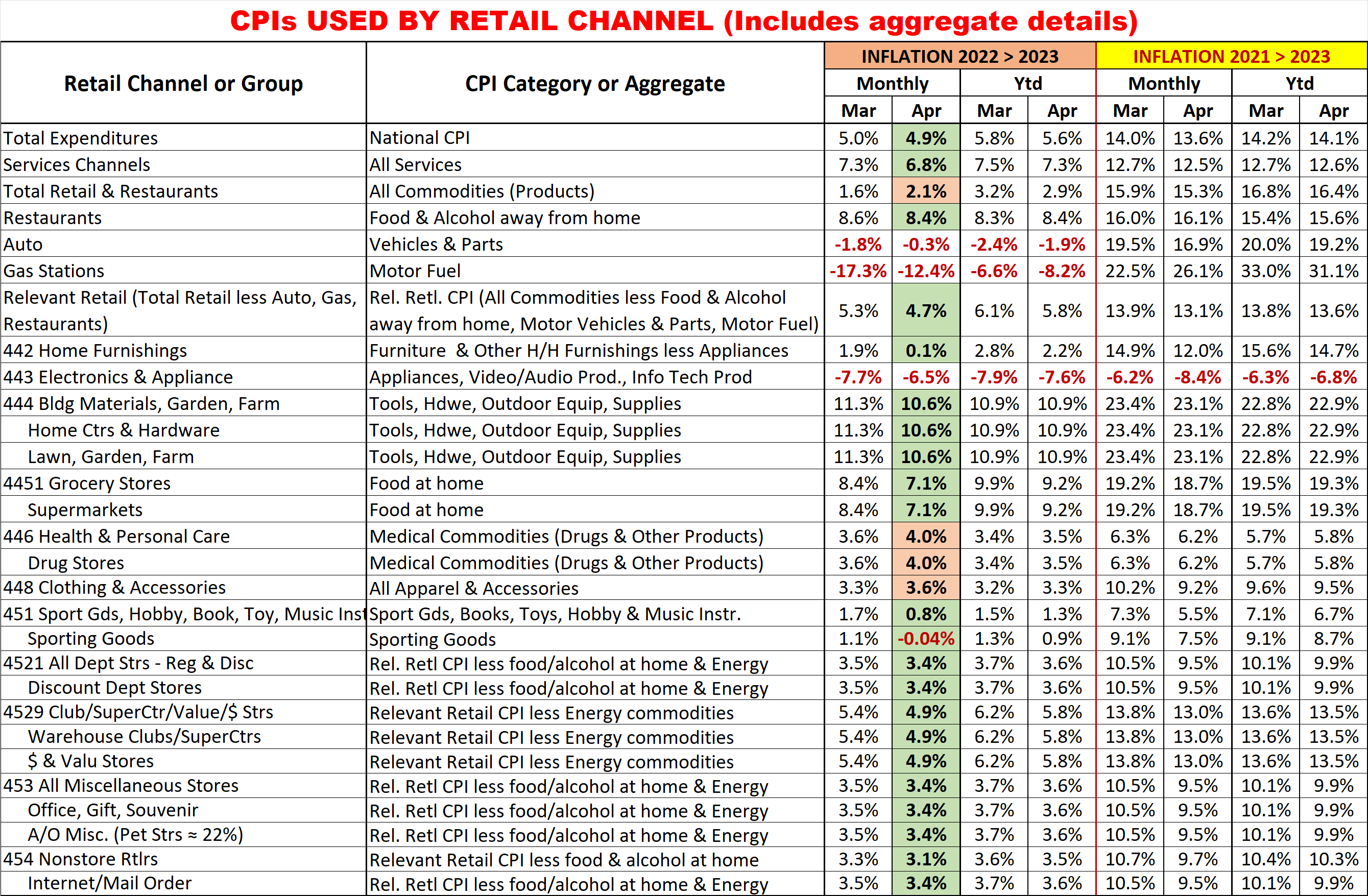

Finally, here are the details and updated inflation rates for the CPIs used to calculate the impact of inflation on retail groups and channels. This includes special aggregate CPIs created with the instruction and guidance of personnel from the US BLS. I also researched data from the last Economic Census to review the share of sales by product category for the various channels to help in selecting what expenditures to include in specific aggregates. Of course, none of these specially created aggregates are 100% accurate but they are much closer than the overall CPI or available aggregates. The data also includes the CPI changes from 2021 to 2023 to show cumulative inflation.

Monthly 22>23 CPI changes of 0.2% or more are highlighted. (Green = lower; Pink = higher)

I’m sure that this list raises some questions. Here are some answers to some of the more obvious ones.

- Why is the group for Non-store different from the Internet?

- Non-store is not all internet. It also includes Fuel Oil Dealers, the non-motor fuel Energy Commodity.

- Why is there no Food at home included in Non-store or Internet?

- Online Grocery purchasing is becoming popular but almost all is from companies whose major business is brick ‘n mortar. These online sales are recorded under their primary channel.

- 6 Channels have the same CPI aggregate but represent a variety of business types.

- They also have a wide range of product types. Rather than try to build aggregates of a multitude of small expenditure categories, it seemed better to eliminate the biggest, influential groups that they don’t sell. This method is not perfect, but it is certainly closer than any existing aggregate.

- Why are Grocery and Supermarkets only tied to the Grocery CPI?

- According to the Economic Census, 76% of their sales comes from Grocery products. Grocery Products are the driver. The balance of their sales comes from a collection of a multitude of categories.

- What about Drug/Health Stores only being tied to Medical Commodities.

- An answer similar to the one for Grocery/Supermarkets. However, in this case Medical Commodities account for over 80% of these stores’ total sales.

- Why do SuperCtrs/Clubs and $ Stores have the same CPI?

- While the Big Stores sell much more fresh groceries, Groceries account for ¼ of $ Store sales. Both Channels generally offer most of the same product categories, but the actual product mix is different.