Global Pet Expo, the Pet Industry’s premiere event, is back to near “normal”. The exhibitor count is up from 2023 and should reach 1136 (+11% vs 23) by showtime. This is lower than the 1173 peak in 2019 but it is still more than enough.

Live events are critical in the Pet Industry because of our attitude towards Pets and Pet Products. Pets are an integral part of our families, and we now increasingly personify them. Pet shows are primarily focused on Pet Products. Studies have shown that over 60% of consumers prefer to make initial buying decisions on Pet Products in person. This makes Pet Products 2nd only to fresh groceries in this behavior. This preference applies to all Pet Products buyers, not just consumers. The retailers and distributors attending GPE and SuperZoo want to see and touch a new product before they buy. Live shows are not just important, they are critical to the continued growth and strength of the Pet Industry.

The Pandemic crisis is over, but it has been replaced by a new worry – strong inflation. You will see evidence of its impact in the makeup of exhibitors at GPE 2024. Consumers are looking for Value (Quality + Price). One way to get it is through Private Label products. GPE 24 has over 120 companies actively soliciting EOM customers. Foreign companies are especially capable of EOM, so their booth share has surged to 36%. The previous peak was 25% in 2019. These trends have also affected individual product categories. Now, let’s take a brief look at what awaits attendees of GPE 2024.

As we said, the show is smaller than the 2019 peak, both in square footage (-2.5%) and number of exhibitors (-3.3%) but there is still more than enough to satisfy the needs and wants of every buyer that attends. Here are some relevant facts.

Will you see any new exhibitors or is it the usual group? There have been 8 live pet trade shows from 2019>23 – 4 GPEs and 4 SZs. There are 1110 exhibitors at GPE 24 but It took 3305 companies to fill all 9 shows. Of the GPE 2024 exhibitors:

The percentage of exhibitors new to GPE this year is slightly above “normal”. There is definitely plenty of “New” to see.

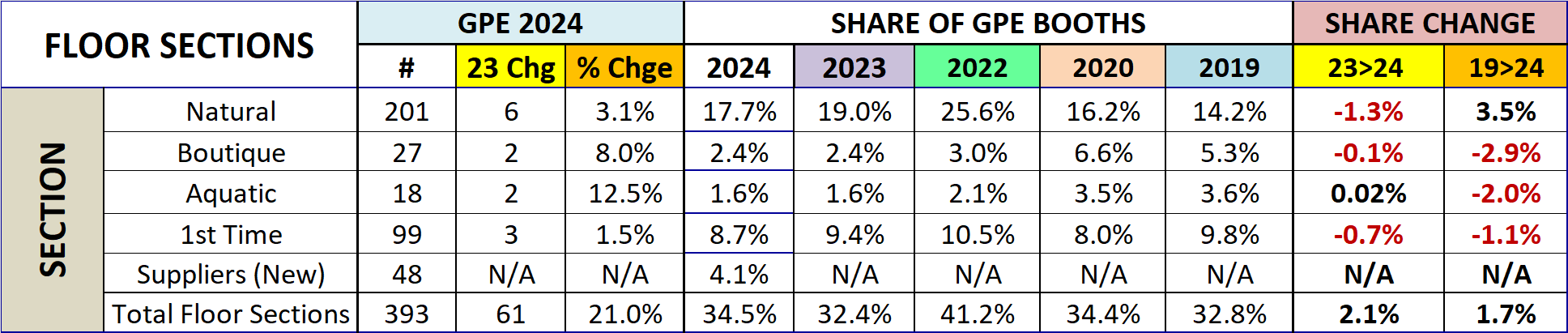

Special “Floor Sections” at GPE account for 34.5% of Booths, up from 32.8% in 2019. This was due to the addition of Suppliers. The primary comparison of GPE 2024 to previous years in this and other areas will be by share of booths.

There are large numbers of exhibitors in the “regular” floor space who would qualify for inclusion in these sections. You need to “work” the whole show to ensure that you get a full view of the product categories of interest to you. I will again be creating a GPE Exhibitor Visit Planner that allows attendees to plan their floor time by targeting the exhibitors with products of interest. The GPE 2024 SuperSearch will be made available by March 4th and be regularly updated with last minute changes. Now, let’s take a look at the results from this year’s research on exhibitors’ product offerings.

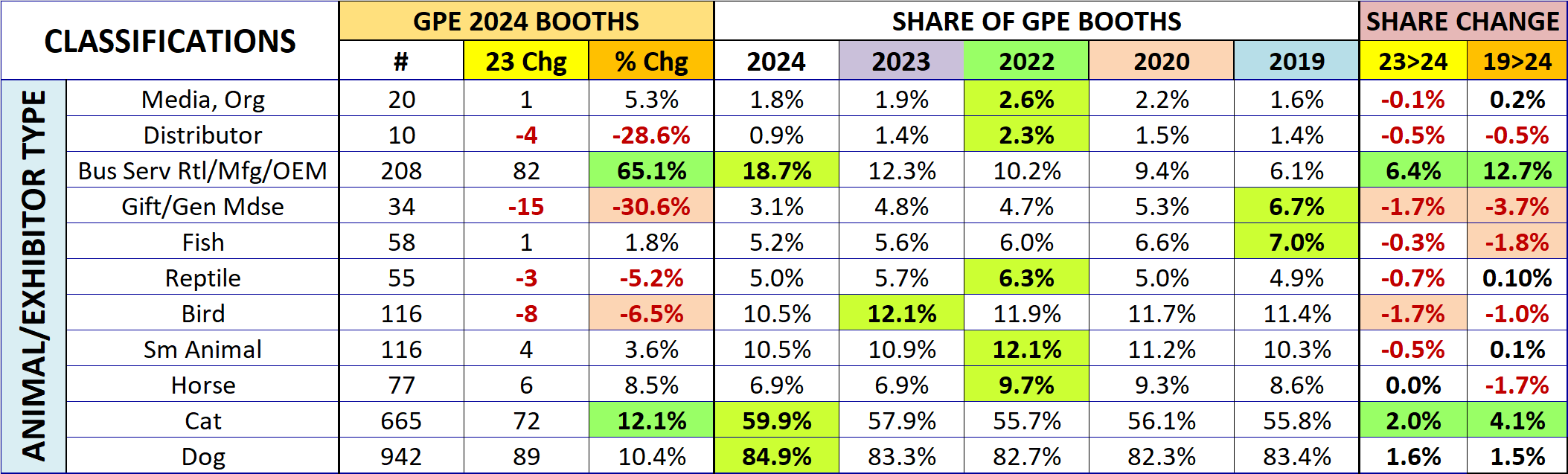

1st, we’ll Compare Exhibitor Types– By function: By Animal type (Numbers are based on booths assigned by 2/16/24)

Results were mostly negative as only 3 categories gained share from 2023.

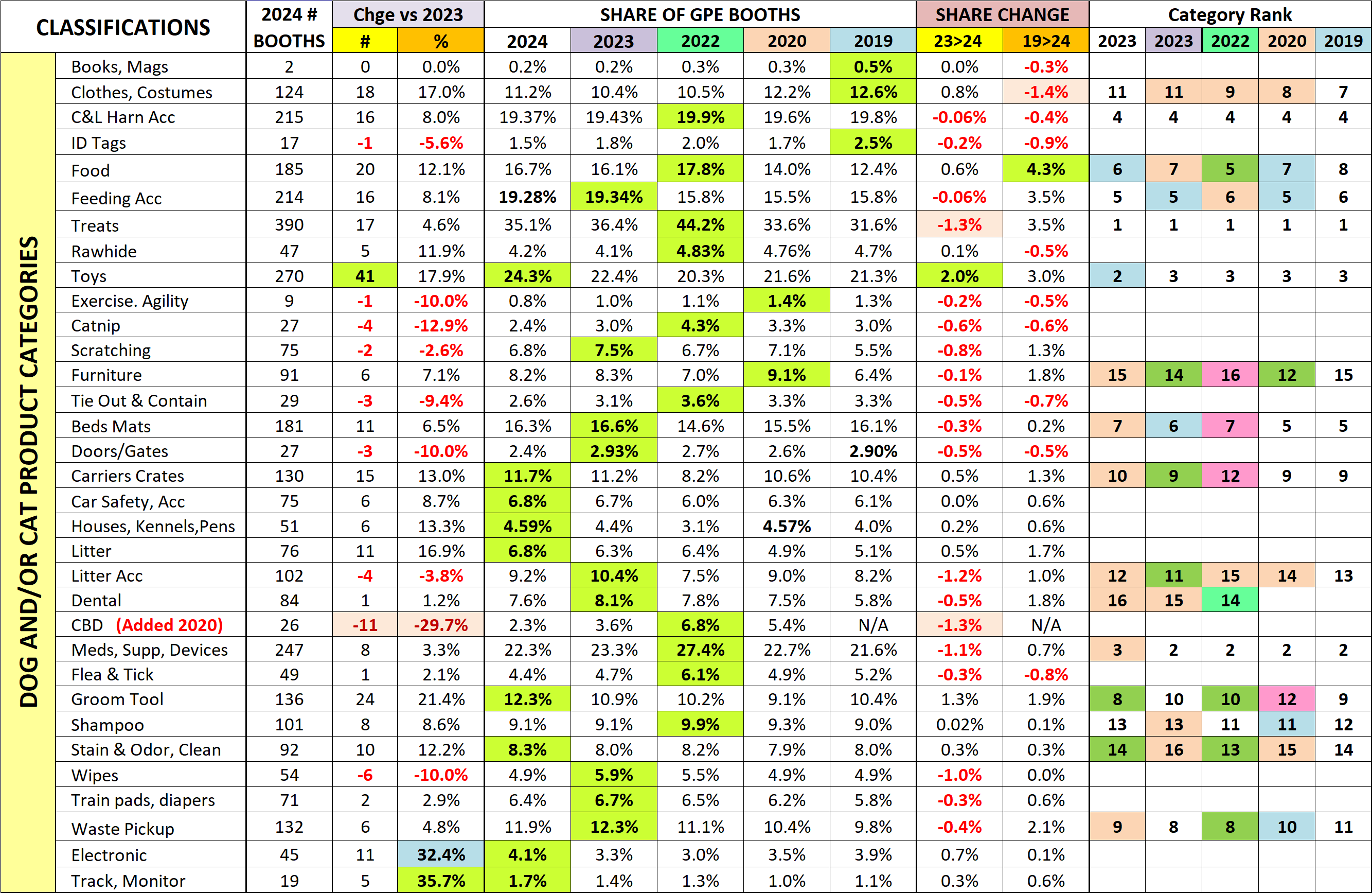

Dogs and Cats are still the undisputed royalty of Pet. Because of their huge impact on the industry. I have divided the products designed for them into 33 subcategories. Let’s see how this year’s GPE Top Ten (by booth count) are doing.

All have more booths than 2023, but the ranking changed for 7 – 3 up & 4 down, including the 1st change in the top 4 in years. The biggest share gain was by Toys, while Treats had the biggest loss.

Pet Parents’ concern for the overall health and wellness of their “pet children” remains a big priority but the impact of strong Petflation has pushed the “value” of Private Label products to the forefront. Their EOM capabilities plus the end of travel restrictions has caused an unparalleled surge in foreign exhibitors. They now occupy over 400 booths (36%). In pre-pandemic 2019 they had 295 booths (25%). You first see the impact at the animal type level. In EOM, Dog & Cat are where the $ are and both reached a record booth share in 2024. Some product categories are also showing an elevation in share including Toys, Bowls/Feeders, Beds, Carrier/Crates and Grooming Tools.

The last chart details the specifics for all 33 of the Dog/Cat product categories that I defined. Of note: All the data inputs for this report and the SuperSearch tool come from a review of the GPE online exhibitor product listings AND visits to over 1300 websites. They’re not 100% accurate, but pretty close. Which categories are of interest to your business?

GPE 2024 is about innovation and fulfilling needs. There are products, services and education to fulfill every need and…want. There is also an abundance of “new” – both in products and the 260+ exhibitors who are new to Pet Industry shows. However, to reap the benefits, you need a plan. Exhibitors must showcase the “right” items. Attendees need to strategically analyze their data, determine what they need to improve their business and develop a plan to find the products to fulfill their needs. Then…execute the plan. If they do nothing else at GPE, attendees will have 1 minute and 10 seconds to spend at each booth. You definitely need a plan! The GPE 2024 SuperSearch will be available the week of March 4th. It can help. Try it out. Good luck in Orlando!

Inflation slowed in January. The monthly Consumer Price Index peaked back in June 2022 at 9.1% then began to slow until turning up in Jul/Aug 2023. Prices fell in Oct>Dec but turned up in January. However, the CPI actually decreased to +3.1% from +3.4% due to a big monthly price lift in 2023. Grocery inflation continues to slow. After 12 straight months of double-digit YOY monthly increases, grocery inflation is now down to +1.2%, 11 consecutive months below 10%. As we have learned, even minor price changes can affect consumer pet spending, especially in the discretionary pet segments, so we will continue to publish monthly reports to track petflation as it evolves in the market.

Petflation was +4.1% in December 2021 while the overall CPI was +7.0%. The gap narrowed as Petflation accelerated and reached 96.7% of the national rate in June 2022. National inflation has slowed considerably since June 2022, but Petflation generally increased until June 2023. It passed the National CPI in July 2022 and at 4.7% in January, it is still 51.6% above the national rate of 3.1%. We will look deeper into the numbers. This and future reports will include:

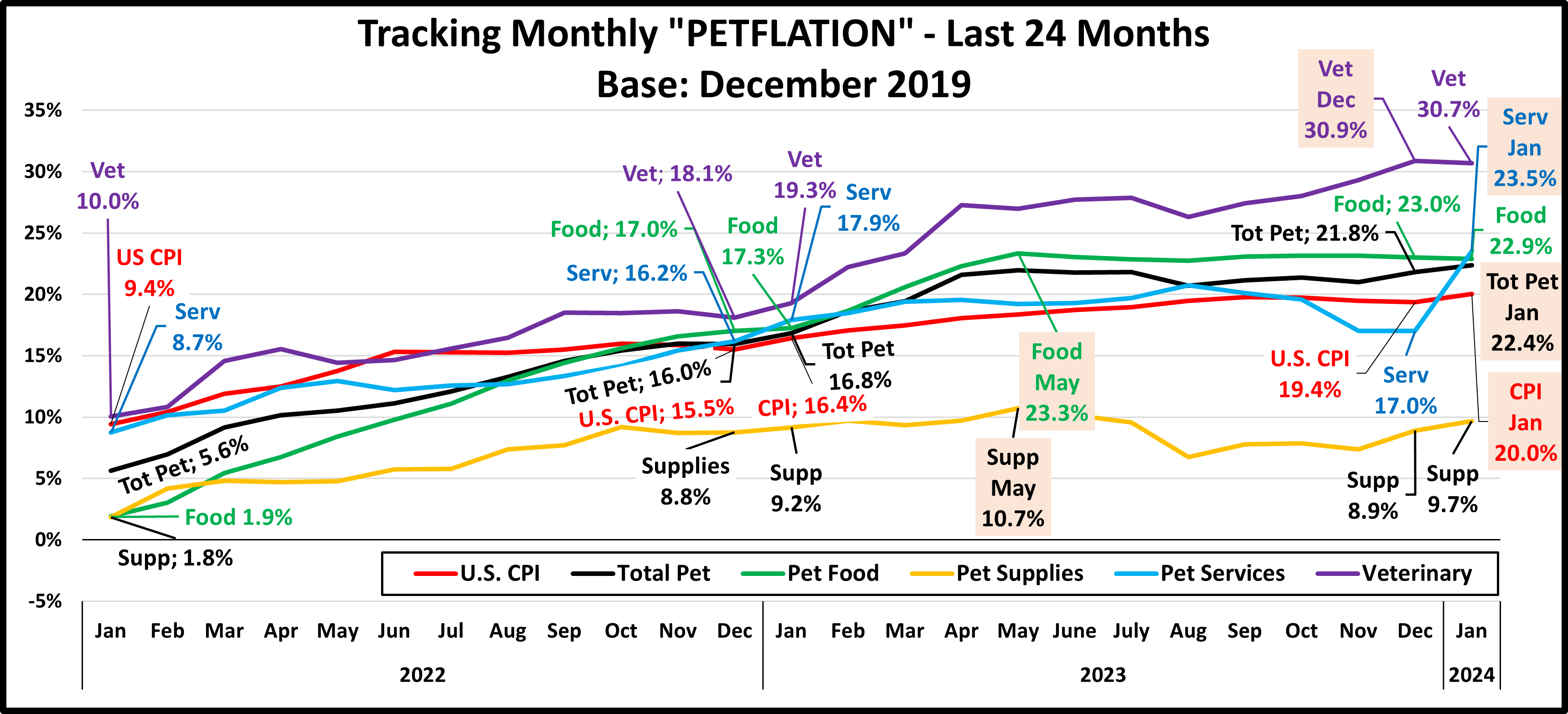

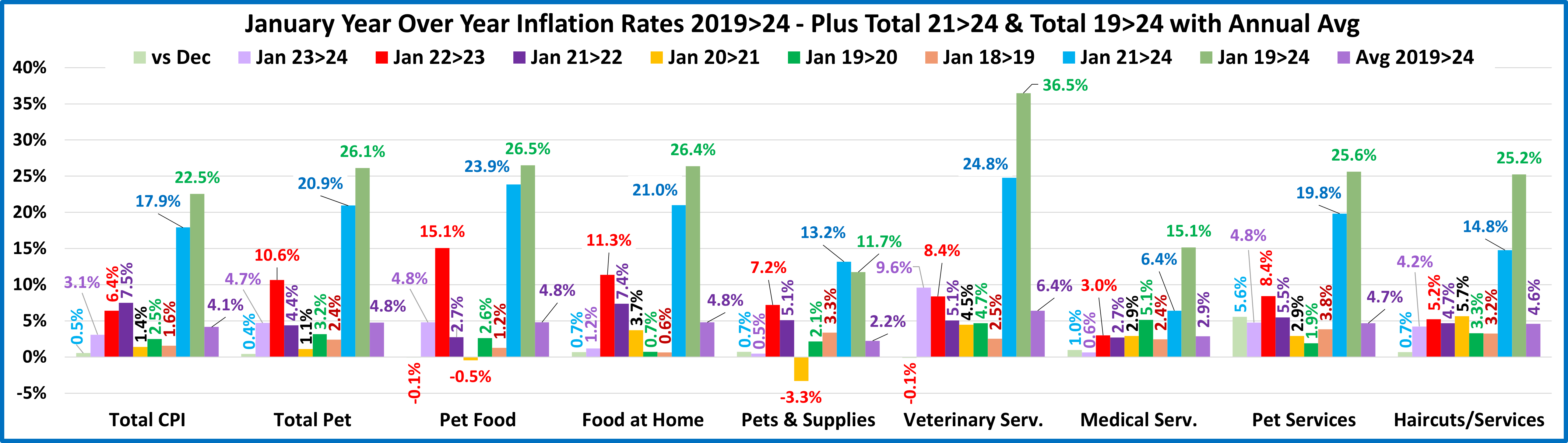

In our first graph we will track the monthly change in prices for the 24 months from January 22 to January 24. We will use December 2019 as a base number so we can track the progress from pre-pandemic times through an eventual recovery. This chart is designed to give you a visual image of the flow of pricing. You can see the similarities and differences in segment patterns and compare them to the overall U.S. CPI. The year-end numbers and those from 12 and 24 months earlier are included. We also included and highlighted (pink) the cumulative price peak for each segment. In January, Pet prices were up from last month as lifts in Services & Supplies overcame drops in Food & Veterinary.

In January 22, the cumulative CPI was +9.4% and Pet prices were +5.6%. Like the CPI, prices in the Services segments generally inflated after mid-2020, while Product inflation stayed low until late 21. In 22 Petflation took off. Food prices grew consistently but the other segments had mixed patterns until July 22, when all increased. In Aug>Oct Petflation took off. In Nov>Dec, Services & Food prices continued to grow while Vet & Supplies prices stabilized. In Jan>Apr 23, prices grew every month except for 1 dip by Supplies. In May Products prices grew while Services slowed. In June/July this was reversed. In August all but Services fell. In Sep/Oct this was reversed. In November, all but Food & Vet fell. In December Supplies & Vet drove Total Pet prices up. In January, Food & Vet prices fell while Supplies & especially Services prices surged. Note: With cumulative inflation, all but Supplies are now at or within 0.4% of their pricing peak.

Now, we’ll turn our attention to the Year Over Year inflation rate change for January and compare it to last month, last year and to previous years. We will also show total inflation from 21>24 & 19>24. Petflation slowed to 4.7%, down from 5.1% in December but it is still 1.5 times higher than the National rate. The chart will allow you to compare the inflation rates of 23>24 to other years but also see how much of the total inflation since 2019 came from the current pricing surge which took off in 2022. Again, we’ve included some human categories to put the pet numbers into perspective.

Overall, Prices were +0.5% from December but were +3.1% vs January 23, down from +3.4% last month. Grocery inflation is down again, to +1.2% from +1.3%. 7 of 9 categories had a price increase from last month – only Vet & Pet Food prices fell. There were 5 increases in December. Pet Services had a big turnaround. After 4 monthly drops, prices rose 5.6%. The national YOY monthly CPI rate of 3.1% is only 48% of the 22>23 rate and 41% of 21>22. The 23>24 inflation rate is below 22>23 for all categories but Veterinary Services. In our 2021>2024 measurement you also can see that over 65% of the cumulative inflation since 2019 occurred in all but 2 segments – Medical Services & Haircuts – both Services categories. Service Segments have generally had higher inflation rates so there was a smaller pricing lift in the recent surge. Pet Products have a very different pattern. The 21>24 inflation surge provided 95.6% of their overall inflation since 2019. This happened because Pet Products prices in 2021 were just starting to recover from a deflationary period. Services expenditures now account for 64.1% of the National CPI so they are very influential. Their current CPI is +4.9% while the CPI for Commodities is +0.1%. Services are driving virtually all of the current 3.1% inflation.

Petflation is slowing, but it is still strong, with the 4th highest rate for January and 2023 had the 2nd highest annual rate in history. It is also 1.5 times the National CPI. In 2021 it was only 75% of that rate. Even if it slows to 0%, you can’t ignore the fact that inflation is cumulative. Pet prices are 20.9% above 2021 and 26.1% higher than 2019. Those are big lifts. Since price/value is the biggest driver in consumer spending it is likely to affect the Pet Industry. The Non-Vet Services segment will be the least impacted as it is the most driven by high income CUs. Supplies and Veterinary will likely see a reduction in purchase frequency. Food is the most needed segment so the response will be complex. It could include a movement to online shopping, switching to private label or even downgrading the quality of food.

In fact, one impact of high cumulative inflation will be very visible soon at the industry’s preeminent trade show, Global Pet Expo 2024. There are over 1100 exhibitors with 120+ actively soliciting OEM (Private Label) customers. Because many have expertise in OEM this private label trend has caused a record surge in Foreign Exhibitors, 36% of all booths including 250 from China. Inflation has further enhanced the importance of “Value” to consumers.

Now we will turn to the final Industry Segment, Veterinary Services. For years, Veterinary Services have had high inflation. This has resulted in CU income becoming the dominant factor in spending and a reduction in visit frequency.

In 2017 low inflation spurred an unusual 7.2% increase in visit frequency and a $2.5B increase in spending. In 2018 inflation returned to more normal levels. Consumers spent $0.56B more (+2.7%), but inflation was 2.6% so virtually all of the lift was from increased prices. In 2019 the situation got worse. Consumers spent $0.58B (+2.7%) more but inflation was 4.14%. This means that there was an actual decrease in the amount of Veterinary Services purchased. In 2020 the pandemic hit, and Pet Parents focused on needs – Food & Veterinary. Veterinary spending grew $3.05B, (+14.0%). In 2021, this behavior grew even stronger and produced a record $7.82B (+31.5%) increase. In 2022 inflation reached 8.8%. Spending fell -$2.95B (-9.0%) but the amount of Veterinary Services sold fell 16.4%. Pricing matters to almost everyone.

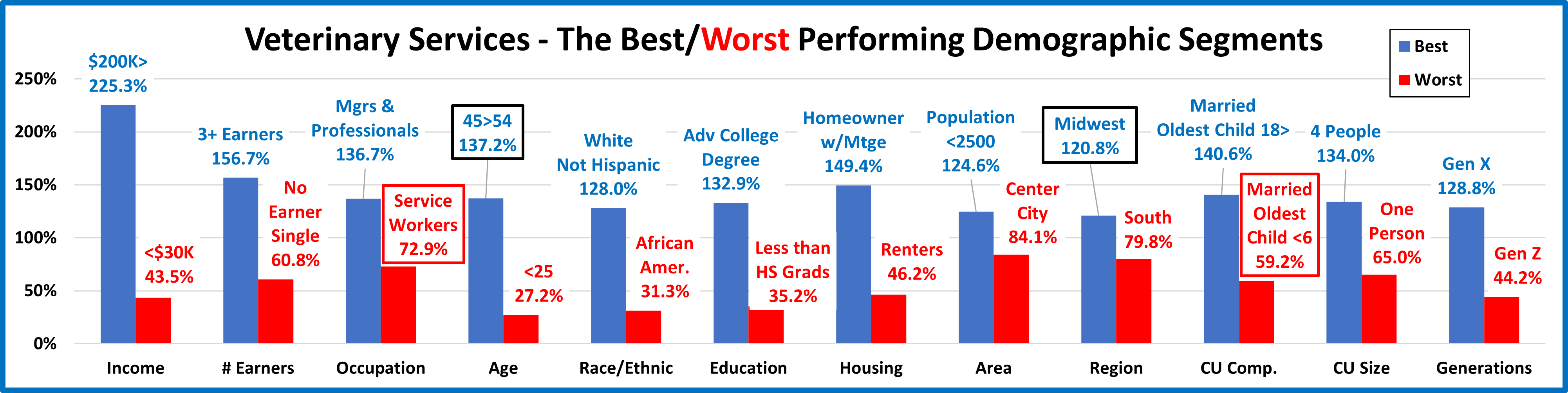

We’ll start our analysis with the groups who were responsible for the bulk of Veterinary spending in 2022 and the $2.95B decrease. The first chart details the biggest Veterinary spenders for each of 10 demographic categories. It shows their share of CU’s, share of Veterinary spending and their spending performance (Share of spending/share of CU’s). In terms of performance – 5 of 10 groups perform above 120%, 1 less than 2018>2021. This is currently 2 less than Supplies (7) and 1 less than Services (6) but 1 more than Food (4). This means that these big spenders are performing well but it also signals that there is still disparity between the best and worst performing demographics in this “needed” segment. Only the College Grads group is different from Total Pet and the categories are listed in the order that reflects their share of Total Pet $pending. Again, High Income is the most important factor in Spending.

Spending disparity fell in 6 categories and the average group performance was 123.2%, down from 125.7% in 2021. Spending became slightly more balanced. Notably, higher income & education became a little less important. Also, Married Couples reached #2 in iimportance. In 2020, they were #6.

Now, we’ll look at 2022’s best and worst performing Veterinary spending segments in each category.

Almost all of the best and worst performers are those that we would expect and there are only 4 that are different from 2021, down from 5 last year. This is 1 more than Services, but 1 less than Supplies and far fewer than the 11 in Food. Also, the average difference between Best & Worst was 88.8%, down from 94.4% in 2021.There was slightly less turmoil and spending disparity between segments in 2022. The changes from 2021 are “boxed”. We should note:

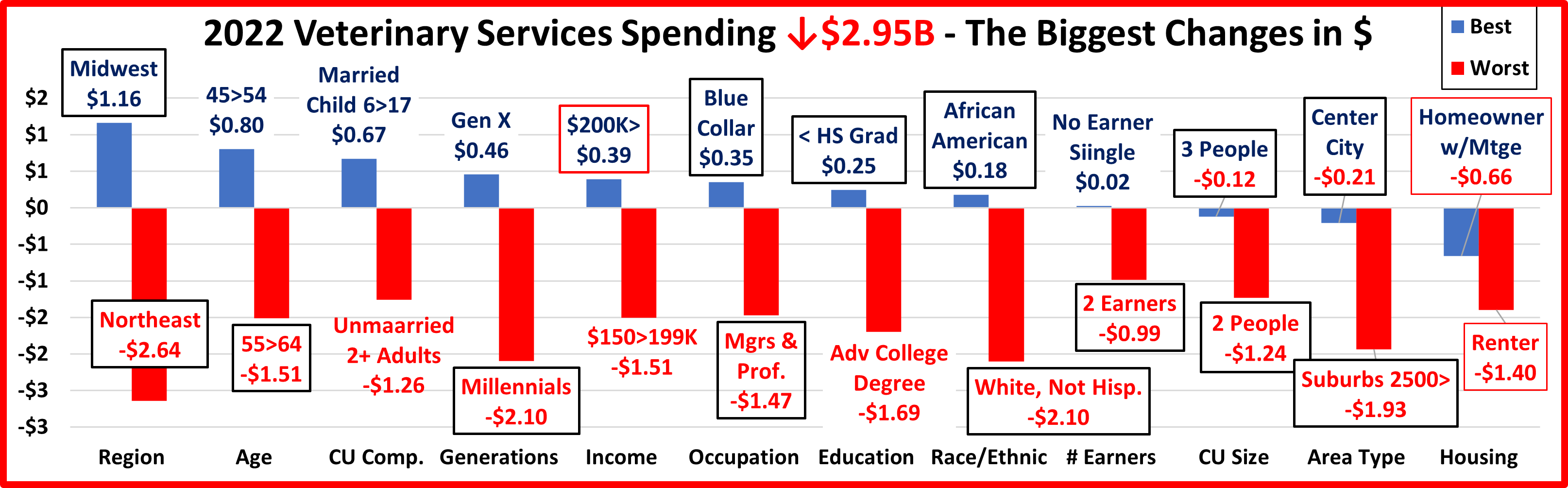

It’s time to “Show you the money”. Here are segments with the biggest $ changes in Veterinary Spending.

We saw little turmoil in performance. That’s not true here. There were 3 repeats and 14 segments flipped from 1st to last or vice versa. Last year there were 8 repeats and 3 flips. There were 5 surprise winners – Blue Collar, <HS Grads, African Americans, No Earner, Singles & Center City. There were only 3 losers that weren’t a surprise – Northeast, Unmarried, 2+ Adults & Renters. ln 3 categories all segments spent less. In 2021, there were 9 where all spent more. Plus, in 2021, 93% of 96 demographic segments spent more. That fell to 23% in 2022.

We’ve now seen the winners and losers in terms of increase/decrease in Veterinary Spending $ for 12 Demographic Categories. 2021 had a record lift but 2022 brought a $2.95B drop. The decrease brought little turmoil in performance as 88% held their position. However, the change in $ was a different story. Only 3 were the same as 2021 and 14 of 24 flipped from 1st to last or vice versa. However, the biggest difference was that in 2021, 93% of demographics spent more including 9 categories where all segments had increases. In 2022, only 23% spent more and there were 3 categories where all spent less. This made the “hidden gems” harder to find, but we did. Here are some segments that didn’t win but helped slow the drop in Veterinary spending. These groups don’t win an award, but they certainly deserve…

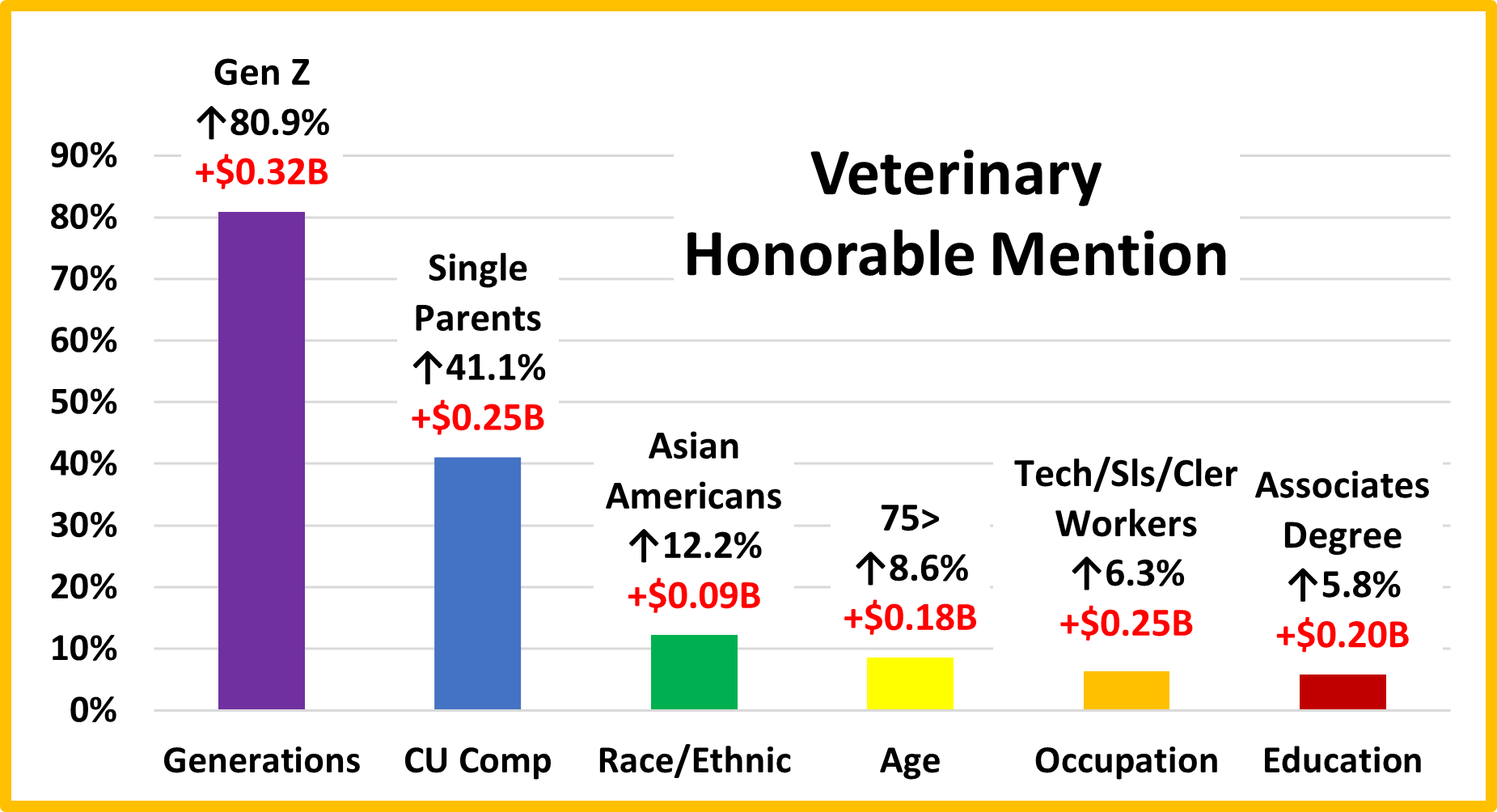

HONORABLE MENTION With huge lifts in all segments, Gen Z “got on board” with all aspects of Pet Parenting. Because of strong family and financial pressures, Single Parents are often at the bottom in Pet spending. In 2022, they spent 54.1% more with lifts in all segments but Supplies, including a 41% increase in Vet Services. Asians have the highest income but the lowest percentage of Pet Parents. In 2022, they focused on services, with lifts in both Non-Vet & Veterinary Services. The 75+ group is also under tremendous financial pressure. Inflation caused them to dial back Food spending, but they had lifts in all other segments. Tech/Sls/Clerical workers are low profile. In 2022, they stood out with lifts in all but Supplies. Associates Degree also usually gets little notice, but 2022 was different. They increased spending in all segments.

With huge lifts in all segments, Gen Z “got on board” with all aspects of Pet Parenting. Because of strong family and financial pressures, Single Parents are often at the bottom in Pet spending. In 2022, they spent 54.1% more with lifts in all segments but Supplies, including a 41% increase in Vet Services. Asians have the highest income but the lowest percentage of Pet Parents. In 2022, they focused on services, with lifts in both Non-Vet & Veterinary Services. The 75+ group is also under tremendous financial pressure. Inflation caused them to dial back Food spending, but they had lifts in all other segments. Tech/Sls/Clerical workers are low profile. In 2022, they stood out with lifts in all but Supplies. Associates Degree also usually gets little notice, but 2022 was different. They increased spending in all segments.

Summary

2016 & 2017 produced a combined increase of $3.6B in Veterinary Spending as inflation moved to record low levels. In 2018 & 2019 a Baby Boomer Spending “Bust” impacted Food & Veterinary. Fortunately, Gen X and Millennials stepped up to produce a 2.7% increase in both years. In 2020 the pandemic focused Pet Parents on the needed segments. This drove a $3B increase in Veterinary $. Boomers & Millennials led the way, but the lift was widespread as 85% of demographic segments spent more. In 2021 the lift grew to a record $7.82B with 93% of all segments spending more including 9 categories where all segments had increases. In 2022, the “binge” was not repeated. Inflation also increased radically to 8.8% and spending fell -$2.95B (-9.0%). There was little turmoil in the best and worst performing demographics as only 3 were different from 2021. However, there was considerable turmoil in the segments with the biggest changes. Only 3 of 24 winners & losers were the same as 2021 and 14 flipped from 1st to last or vice versa. 77% of all demographics spent less and in 3 categories, all segments decreased spending.

The performance of big spending groups is very important in all industry segments. In Veterinary we identified 5 demographic categories with high performing (120+%) large groups. That is 1 less than 2021. It is also 1 more than Pet Food, but 1 less than Services and 2 less than Supplies. The big groups with a high performance level in Veterinary are:

Consumers have no control over Race/Ethnicity but can make decisions in the other categories. Income is still the most important factor. The others are important but essentially equal in performance – 128>131%. Although spending fell, it became slightly more balanced with the drop from 6 to 5 big groups performing over 120%. Another indication of this is that the average spending disparity between the best and worst performing segments dropped from 94.4% to 88.8%.

Another big concern is high inflation. In 2021 spending grew 31.5% in the pandemic surge. Inflation was high at 4.2% but 84% of the growth was real. In 2022 spending fell -9.0%. Inflation was 8.8% so the amount sold was really down -16.4%. Also 77% of 96 demographic segments spent less $ but if we factor inflation into the numbers, 91% actually bought less Veterinary Services. If high inflation continues it could have a major impact on Veterinary Spending.

Finally – The “Ultimate” Veterinary Services Spending Consumer Unit consists of 4 people – a married couple with an oldest child over 18. They are 45>54 years old. They are White, but not of Hispanic origin. At least one of them has an Adv. College Degree and works as a Mgr/Professional. Their oldest child also works. Their total income is $200K>. They live in a small suburb, adjacent to a big city in the Midwest and are still paying off the mortgage on their home.

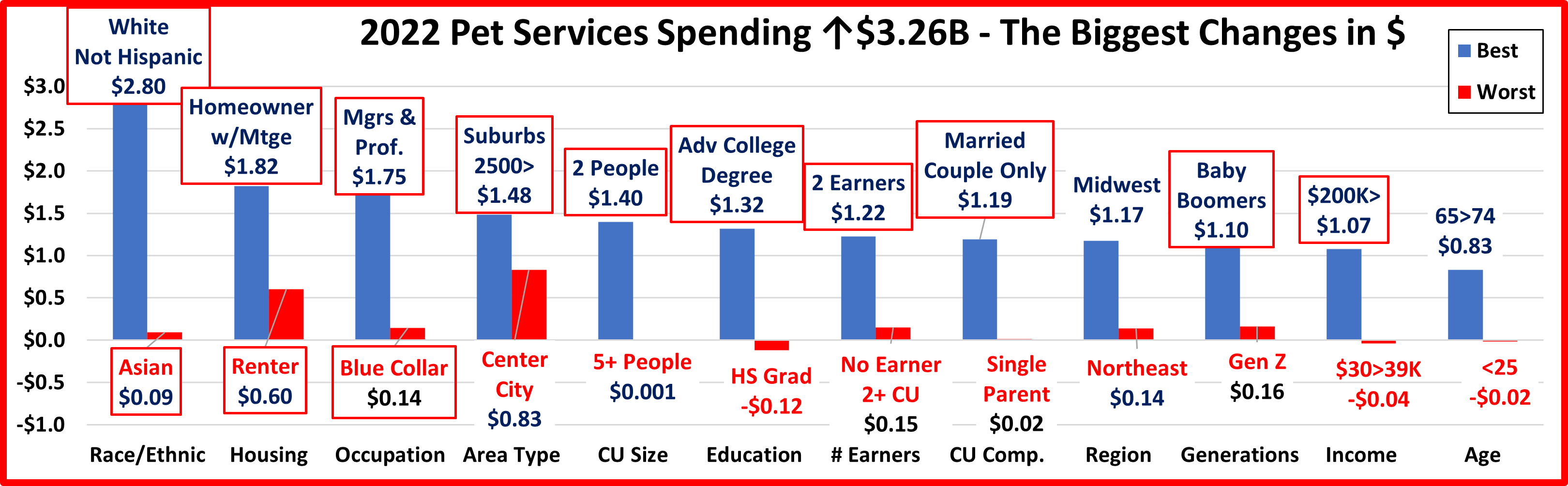

Next, we will look at Pet Services. It is still by far the smallest Segment, but like Supplies and Veterinary, it had a record increase in 2021. However, unlike them, there was no $ drop in 2022. The lift grew stronger, up $3.26 (+35.8%). After the great recession, Services’ annual spending slowly but steadily increased. During this time, the number of outlets offering Services strongly grew as brick ‘n mortar retailers looked for a way to combat the growing influence of online outlets. After all, you can buy products, but you can’t get your dog groomed on the Internet. This created a highly price competitive market for Pet Services. In 2017 there was a slight increase in visit frequency, but Pet Parents just paid less. This resulted in a 1.0% decrease in Services spending. In 2018 consumer behavior changed as a significant number decided to take advantage of the increased availability and convenience of Pet Services and spending literally took off, +$1.95B (+28.9%), the biggest increase in history. In 2019 Pet Parents, especially the younger ones, value shopped, and spending turned down $0.10B. In the 2020 pandemic Services outlets were often deemed nonessential and were subject to restrictions and closures which drove a huge drop in $. In 2021 things opened up again and Pet Parents came back to Services generating the biggest $ increase ever. The trend didn’t end in 2022. It accelerated with a new record increase.

Services spending is the most discretionary, but its reach is expanding. Let’s look deeper into the demographics.

Let’s start by identifying the groups most responsible for the bulk of Services spending in 2022 and the $3.26B increase. The first chart details the biggest Pet Services spenders for each of 10 demographic categories. It shows their share of CU’s, share of Services spending and their spending performance (Share of spending/share of CU’s). In order to better target the bulk of the spending we had to alter the groups in 3 categories – income, area & education. The performance level should also be noted as 6 of 10 groups have a performance level above 120%. This is 1 less than 2021 but the 2nd most for any segment only behind Supplies with 7. Veterinary and Total Pet have 5 and Food has only 4. This indicates that the disparity between the best and worst performing segments shrank a little in 2022, but it is still the highest of any segment. Income is still the biggest factor in Services Spending. The categories are presented in the order that reflects their share of Total Pet $ which highlights the differences of the 7 matching groups. For Services, the share ranking differences from Total Pet are small. The # of Earners and Occupation are more important in Services.

We changed 3 of the groups for Services – Income, Area & Education, to better target the biggest spenders. We should also note that Income is still more important to spending in Services than in any other segment. Only Race/Ethnic and Occupation gained in both share and performance. Also, Services now has 6 groups performing at 120+%, down from 7 in 2021. Overall, in 2022 Services spending became slightly more demographically balanced.

Now, we’ll look at 2022’s best and worst performing Pet Services spending segments in each category.

Except for Area, the best & worst performers are not a surprise. There are 3 that are different from 2021, all in the best group, 7 less than last year. Area shows the continued move away from high population. Income is a big factor for almost all categories. Gen X is still on top, but spending shifted towards their older members, 45>54. The average difference between Best & Worst is 100.3%, the highest of any segment. However, it is better than 108.5% in 2021. Pet Services spending became slightly more balanced in 2022. Changes from 2021 are “boxed”. We should note:

In Pet Services spending performance, income is still the major factor. Spending began skewing younger in 2018. They slipped a little in 2019 but they basically held their ground during the 2020 pandemic. In 2021, Boomers, Millennials and the younger Gen Xers got on board. In 2022, spending skewed a little towards the older Gen Xers – 45>54.

It’s time to “Show you the money”. Here are segments with the biggest $ changes in Pet Services Spending.

In this chart you immediately see the difference from last year. In 2022 you first notice stability. There were 13 repeats. In 2021 there were none. Also, no segments flipped from 1st to last or vice versa. In 2021 there were 13 flips. While 2021 brought a record increase, the lift in 2022 was even stronger and more widespread. In 9 categories all segments spent more compared to 5 in 2021. Also 93% of 96 demographic segments spent more, up from 90% In 2021. One thing is slightly worse. The biggest drop was -$0.12B. In 2021 it was only -$0.07B. 😊

Here are the specifics:

We’ve seen the winners and losers in terms of change in Services Spending $ for 12 Demographic Categories. The lift set another new record and was even more widespread than 2021. Here’s some data which shows the evolution from 2018 to 2022. Services were hit hard by the pandemic but recovered stronger than ever with 2 record lifts. They were the only segment to do this which reflects an attitudinal change by Pet Parents. You see the differences in the big swings.

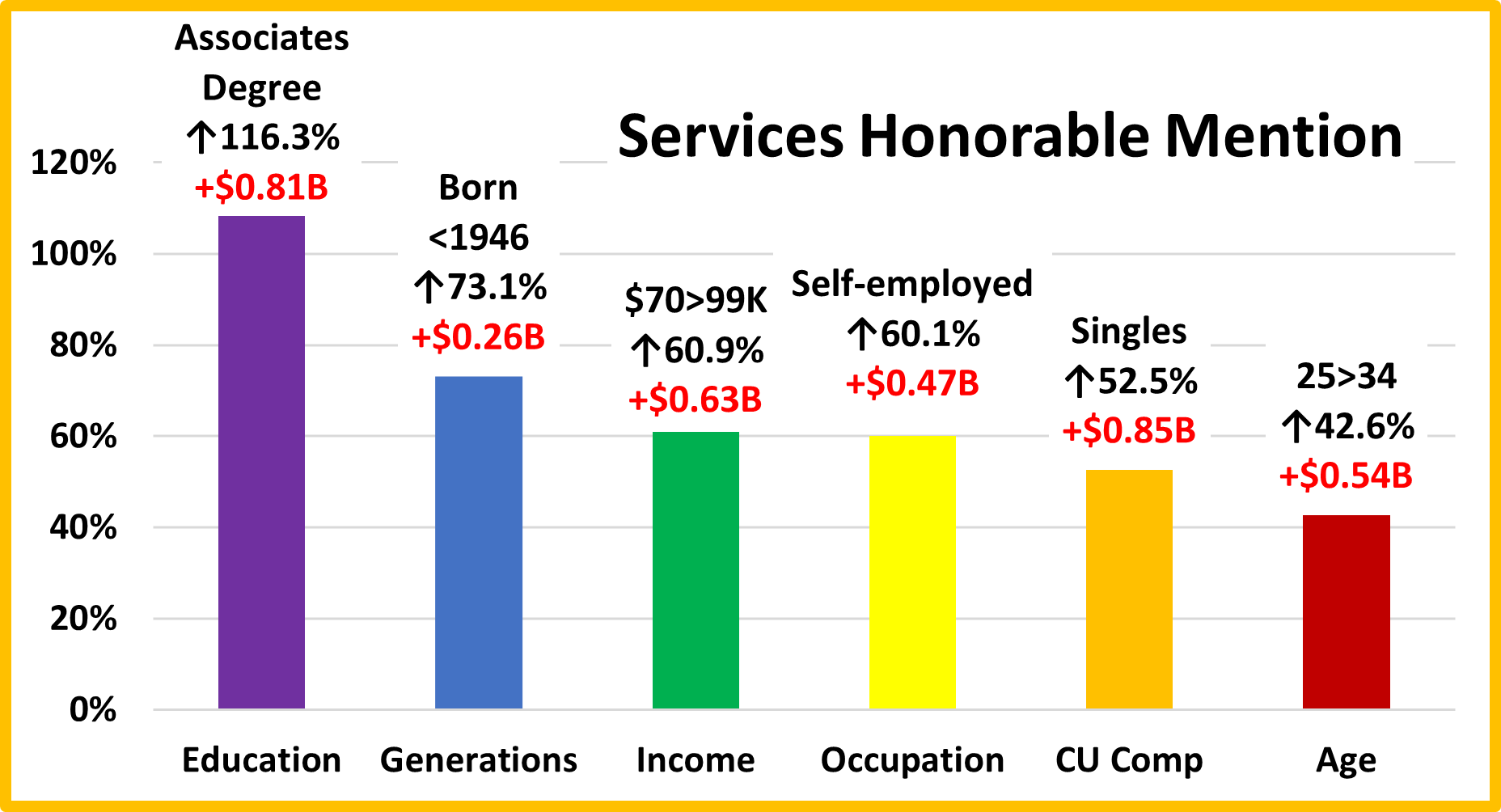

We found the winners in performance and $, but there were others who performed well but didn’t win. They deserve….

HONORABLE MENTION

As usual this group is an eclectic mix. The Associate’s degree group immediately stands out as they more than doubled their Services’ spending. While spending skewed a little older, it also became a little more balanced among age groups which is shown by the strong performances of 25>34 yr-olds and those Born <1946. The Self-Employed group is often a winner, so they are no surprise. Their big lift didn’t happen until 2022 but their Services spending has generally grown every year, including aa 24% increase in 2020. Singles are often at the bottom in spending. They too had a small, 8% increase in spending in 2021 and followed it up with a 52% lift in 2022. Finally, the $70>99K group. Their income is below average and they have big CUs. However, they still managed to have a huge 60.9% lift in spending. In 2022, 93% of all segments increased Services spending. That means that we could have added many more to this honored group.

Summary

For years, Services’ spending slowly but steadily increased. However, the number of outlets offering Services was radically increasing. In 2017, this competitive pressure caused Pet Parents to shop for value and spending fell 1%. In 2018, the abundance of outlets and competitive prices finally had their intended impact. Many more consumers took advantage of the convenience of Pet Services and spending literally took off with a record increase to a new all-time spending high. In 2019 Consumers held their ground at the new higher level but we saw turmoil similar to 2017. Again, value shopping likely contributed to the small decrease.

In 2020, pandemic Services outlets were often deemed nonessential, so they were subject to restrictions and closures. Services are definitely needed by some groups. However, for most demographics, Services are a convenience and spending is very discretionary in nature. The reduced availability and the pandemic driven focus on the “needed” segments – Food and Veterinary caused a 20% drop in Services $.

In 2021 the Retail Marketplace opened up again and many Pet Parents strongly returned to their previous Services mantra, “I need help with my Pet “children” and I have the money to pay for it!”. This behavior was widespread as 90% of all demographics spent more on Services, producing a record increase. In 2022 Services showed that it was different from other segments. All had record lifts related to the Pandemic followed by drops, except for Services. 2022 spending didn’t decrease, it grew even stronger, +$3.26B and more widespread as 93% of demographics increased spending. However, Services is the segment where spending is the most driven by income, so it has always had a big disparity between segments. This improved slightly in 2022. Performance differences are a key measurement of disparity. Let’s consider the performance of the big groups. There were 6 categories with a 120+% performing big group, down 1 from 2021, and now 1 less than Supplies (7) but more than Veterinary (5) and Food (4). There is an even better measure of the improvement. In 2021, the average difference between best & worst performers was 108.5%. In 2022 it was 100.3%.

Another key trend in 2022 was that Gen X & Boomers are still the top 2 spenders, but their older members drove the lift.

Services were hit the hardest by the pandemic in 2020 but they had a record, widespread recovery in 2021. They are the segment most driven by high income so the 6.3% inflation in 2022 had less of an impact. It affected the spending of some specific, financially challenged groups, but the 2022 lift was even bigger and more widespread than 2021.

At Last – The “Ultimate” Pet Services Spending Consumer Unit consists of 2 people – a married couple with no kids at home. They are 45>54 yrs-old and White, but not of Hispanic origin. They both work and at least one of them has an Advanced College Degree and is a Manager or Professional. They have an income of over $200K. They live in a small suburb of a metropolitan area of 2.5>5 MM in the Western U.S. and are still paying off their home mortgage.