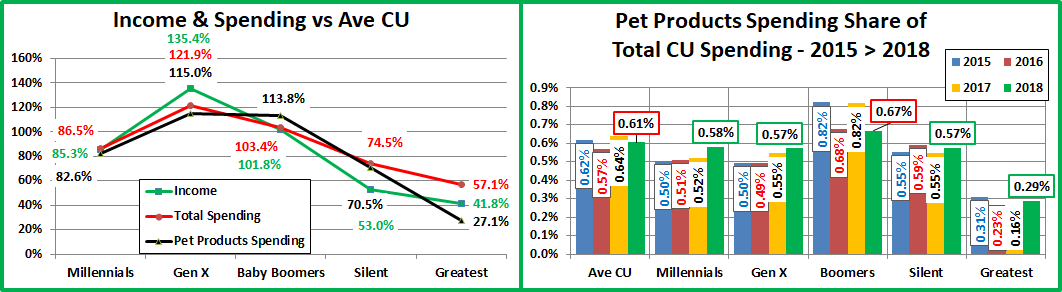

2018 Total Pet Spending was $78.60B – Where did it come from…?

Total Pet Spending in the U.S. reached $78.60B in 2018, a $1.47B (1.9%) increase from 2017. These figures and others in this report are calculated from data in the annual Consumer Expenditure Survey conducted by the US BLS. 2018 was a much more sedate year for the industry after the spectacular lift in 2017. However, it was only calm on the surface. When you look at each segment there was a certain amount of turmoil. The FDA warning on grain free dog food, the new tariffs on supplies and increased inflation in Veterinary all had a negative impact on spending in the second half. The good news was a record surge in Services Spending. 2018 also saw a $6.5B drop in spending by the Baby Boomers. Fortunately, other groups, especially the younger ones, stepped up. The situation certainly deserves a closer look.

The first question is, “Who is spending most of the $78+ billion dollars?” There are of course multiple answers. We will look at Total Pet Spending in terms of 10 demographic categories. In each category we will identify the group that is responsible for most of the overall spending. Our target number was to find demographic segments in each category that account for 60% or more of the total. To get the finalists, we started with the biggest spending segment then bundled related groups until we reached at least 60%.

Knowing the specific group within each demographic category that was responsible for generating the bulk of Total Pet $ is the first step in our analysis. Next, we will drill even deeper to show the best and worst performing demographic segments and finally, the segments that generated the biggest dollar gains or losses in 2018.

In the chart that follows, the demographic categories appear in ranked order by Total Pet market share from highest to lowest. We also included their share of total CU’s (Financially Independent Consumer Units) and their performance rating. Performance is their share of market vs their share of CU’s. This is an important number, not just for measuring the impact of a particular demographic group, but also in measuring the importance of the whole demographic category in Spending. These are all large groups with a high market share. A performance score over 120% means that this demographic measure is extremely important in generating increased Pet Spending. I have highlighted the 6 groups with 120+% performance. (I rounded up for the 35>64 age group).

The groups are the same as in 2017, but some rankings have changed. Everyone Works and Education gained in share ranking and performance. Suburban gained share but not rank. The performance of the other 7 groups fell, indicating more balanced spending. Homeowners, All Wage & Salaried, Married Couples and 35>64 yr olds fell in share ranking.

- Race/Ethnic – White, not Hispanic (86.3%) This is the 2nd largest group and accounts for the vast majority of Pet Spending. Their performance rating fell slightly to 125%. This category now officially ranks #5 in terms of importance in Pet Spending demographic characteristics but they are in a virtual tie for 3rd place with 2 other groups. Although this demographic, along with age, are 2 areas in which the consumers have no control. Spending disparities are enhanced by differences in other areas like Income, CU Composition and homeownership. There are also apparently cultural differences which impact Pet Spending. Asian Americans are first in income, education and spending but last in Pet Spending as a percentage of total spending – 0.33% vs a national average of 0.98%.

- # in CU – 2+ people (80.9%) It just takes two. Singles still have the lowest performance of any group, but they gained ground in 2018. This gain along with a drop in spending by 2 person CU’s caused the overall performance of 2+ CUs to drop to 114.7%. However, 4 person CUs also gained so only singles and 5+ person CU perform under 100%.

- Housing – Homeowners (79.8%) Controlling your “own space” has long been a key to larger pet families and more pet spending. However, 2018 was a good year for renters. Homeowners had the biggest drop in both share and performance. Their 125.7% performance dropped them to 3rd place in terms of importance for increased pet spending. The homeownership rate for Millennials is substantially lower than previous generations when they were the same age but it is increasing. We also saw an impact from more older Americans “downsizing”.

- Income – Over $50K (74.9%) Although Pet Parenting is common in all income groups, money does matter. With a performance rating of 138.9%, CU income is the single most important factor in increased Pet Spending. Their performance decreased from 141.6% in 2017. This was driven by a spending drop in the $50>99K range, along with a strong lift from those earning $30>49K.

- Education – Associates Degree or Higher (69.5%) Income generally increases with education level and so does Pet spending. Education can also be a key factor in recognizing the value in product improvements, like super premium foods. In 2018 this higher educated group spent $4.9B more on their pets and moved up from 7rd to 5th in share of pet spending. This move also reflects the spending lift by the younger groups as they are generally more educated than Boomers+. At the same time High School Grads with some College substantially decreased their Pet spending so the performance of the Associates Degree and More group moved up from 120.1% to 127.5% – from 6th to 2nd place. This moves Education back to the forefront in terms of importance in Pet Spending.

- Occupation – All Wage & Salary Earners (64.4%) – Pet ownership is widespread across all segments in this group. After a big lift In 2017, the blue-collar workers radically cut back their pet spending, especially on Food. All Wage & Salary Earners’ performance fell to 105.4%, by far the lowest of any group. It remains below 110% because there is still a big spending (and income) disparity within the group and the self-employed also had a great year!

- # Earners – “Everyone Works” (63.8%) This is a composite of CU’s, regardless of size, where all adults are employed. This group’s ranking in share of overall pet spending jumped from 9th to 7th. Their performance increased from 108.2% to 110.3%. Younger CUs have more earners. You see one sign of their increased 2018 Pet $ right here.

- Age – 35>64 (63.2%) This group’s share of spending fell from 6th to 8th because the 55>64 yr olds spent $4B less. The 35>54 group couldn’t quite make it up. The 65+ and under 35 groups also had a good year which pushed the 35>64 yr old’s performance down from 123.2% to 119.5%. However, they are still ranked 6th in overall importance.

- CU Composition – Married Couples (62.2%) With or without children, two people, committed to each other, is an ideal situation for Pet Parenting. In 2018, primarily due to a drop in spending by married couples only CU’s, this group fell from 8th to 9th in share of spending. A big spending lift by singles also contributed to a decrease in performance from 128.1% to 125.2%. which dropped them from 3rd to 4th in importance.

- Area – Suburban (61.0%) Homeownership is high and they have the “space” for pets. Their share of pet spending increased from 59.8%. Their performance also increased from 107.6 to 110.0%. The gain in share and performance was due to a great year for Suburbs over 2500 pop. All areas under 2500, both rural and suburban had a bad year. Rural areas were down $3.23B which drove Suburban performance up, despite a $2.7B increase by Center Cities.

Total Pet Spending is a sum of the spending in all four industry segments. The “big demographic spenders” listed above are determined by the total pet numbers. Although the share of spending and performance of these groups may vary between segments, every one of them generates a minimum of 58.2% of the spending in every segment. As we analyze individual segments, some of the groups will change to better reflect where most of the business is coming from.

The group performance is a very important measure. Any group that exceeds 120% indicates an increased concentration of the business which makes it easier for marketing to target the big spenders. Although Income over $50K is the clear winner, there are other strong performers. The high performance in 6 groups also indicates the presence of segments within these categories that are seriously underperforming. These can be identified and targeted for improvement.

Now, let’s drill deeper and look at 2018’s best and worst performing segments in each demographic category.

Most of the best and worst performers are just who we would expect and there are only 5 that are different from 2017. Changes from 2017 are “boxed”. We should note:

- Income is very important, which is shown by the 221.5% performance. All income groups over $70K have 100+% performance. However, there was also radically improved performance from the $30>49K group.

- Generation – Baby Boomers fell from the top spot for the first time since… However, the Gen Xers stepped up.

- Age – It was a youth movement. The 45>54 yr olds took over the lead from the 55>64 yr old Boomers and the under 25 group escaped the bottom to be replaced by the oldest Americans.

- Occupation – After a 1 year break, the high income Self-Employed Group moved back to the top.

- CU Composition – Although the performance of Married Couple Only fell, they are the winner for a 3rd consecutive year. Married w/children improved performance, but the big news is Singles moved up and out of the loser spot.

Except for the move from Boomers to GenX, there was little change in the “players”, so most expected winners are still doing well. In the next section we’ll look at the segments who literally made the biggest difference in spending in 2018.

We’ll “Show you the money”! This chart details the biggest $ changes in spending from 2017.

Now we will truly see the difference between 2018 and 2017. There are 24 Winners and Losers. 2 Losers and 1 Winner are repeats but 13 segments (54%) actually switched from the biggest increase to the biggest decrease or vice versa.

- Generation – The Boomer Bust had a widespread impact and the negatives were often incredibly big numbers.

- Winner – Gen X – Pet Spending: $25.15B; Up $3.81B (+17.9%)

- 2017: Baby Boomers

- Loser – Baby Boomers – Pet Spending: $29.61B; Down -$6.48B (-18.0%)

- 2017: Silent Generation

- Comment – It took the contribution of many segments to generate overall positive numbers for 2018.

- Winner – Gen X – Pet Spending: $25.15B; Up $3.81B (+17.9%)

- Housing – Homeowners w/Mtge, the biggest segment in this category, won for the first time since 2014.

- Winner – Homeowner w/Mtge – Pet Spending: $42.92B; Up $3.29B (+8.3%)

- 2017: Homeowner w/o Mtge

- Loser – Homeowner w/o Mtge– Pet Spending: $19.81B; Down -$3.37B (-14.6%)

- 2017: Homeowner w/Mtge

- Comment – Winner and loser flipped. W/O Mtge group was driven down by older workers with paid off homes.

- Winner – Homeowner w/Mtge – Pet Spending: $42.92B; Up $3.29B (+8.3%)

- Area Type – Central City led the way in the movement to Urbanize Total Pet Spending – another flip.

- Winner – Central City – Pet Spending: $23.59B; Up $2.66B (+12.7%)

- 2017: Rural

- Loser – Rural – Pet Spending: $7.05B; Down -$2.99B (-29.8%)

- 2017: Central City

- Comment – Areas under 2500 population – down -$3.23B. Areas over 2500 – up $4.7B.

- Winner – Central City – Pet Spending: $23.59B; Up $2.66B (+12.7%)

- Education – HS Grads with some College gave back 88% of their 2017 gain and flipped from winner to loser.

- Winner – BA/BS Degree – Pet Spending: $25.13B; Up $2.63B (+11.7%)

- 2017: HS Grad w/some College

- Loser – HS Grad w/some College – Pet Spending: $12.99B; Down -$3.47B (-21.1%)

- 2017: Assoc. Degree

- Comment – The BA/BS group led the way but groups with at least an Associate degree were up $4.87B. Higher Education, which generally generates higher income, has moved back up in importance in Total Pet Spending.

- Winner – BA/BS Degree – Pet Spending: $25.13B; Up $2.63B (+11.7%)

- Age – The 55>64 yr olds flipped again, but this time it was from winner to loser.

- Winner – 35>44 yrs – Pet Spending: $14.46B; Up $2.31B (+19.0%)

- 2017: 55>64 yrs

- Loser – 55>64 yrs – Pet Spending: $17.50B; Down $3.95B (-18.4%)

- 2017: <25 yrs

- Comment: The 55>64 yr olds stood alone as every other age group increased their Total Pet spending.

- Winner – 35>44 yrs – Pet Spending: $14.46B; Up $2.31B (+19.0%)

- Income – No repeats or flips here but the over $150K group was up $3.12B

- Winner – $150 to $199K – Pet Spending: $9.12B; Up $1.96B (+27.4%)

- 2017: $100 to $149K

- Loser – Under $30K – Pet Spending: $9.47B; Down -$1.44B (-13.2%)

- 2017: $30 to $39K

- Comment – Although the increase was definitely skewed towards higher incomes, it was a roller coaster ride. Over $100K – Up $3.45B; $50>99K – Down -$1.54B; $30>49K – Up $1.0B; Under $30K – Down -$1.44B

- Winner – $150 to $199K – Pet Spending: $9.12B; Up $1.96B (+27.4%)

- Occupation – Another dual flip between the winner and the loser and we’re back to a more “expected” outcome.

- Winner –– Self-Employed – Pet Spending: $7.24B; Up $1.83B (+33.8%)

- 2017: Blue Collar Workers

- Loser – Blue-Collar Workers – Pet Spending: $11.84B; Down -$2.77B (-18.9%)

- 2017: Self-Employed

- Comment – In 2017 Blue-Collar workers were the big movers. In 2018 they gave back 64% of their gain. In 2018 Self-employed workers gained 4% in CUs and 28% in Income and spent some of the extra $ on their pets.

- Winner –– Self-Employed – Pet Spending: $7.24B; Up $1.83B (+33.8%)

- CU Composition – Married Couples only, the perennially best performing segment, flipped from winner to loser.

- Winner –– Singles – $14.99; Up $1.64B (+12.2%)

- 2017: Married, Couple Only

- Loser – Married, Couple Only – $24.58B; Down -$1.72B (-6.5%)

- 2017: Married Oldest Child <6

- Comment – In 2018 there were 2 choices for increased pet spending. You needed to be single or a married couple with children of any age. Every other CU composition segment spent less.

- Winner –– Singles – $14.99; Up $1.64B (+12.2%)

- # in CU – This dual winner/loser flip is mind blowing and likely unprecedented.

- Winner – 1 Person – Pet Spending: $14.99B; Up $1.64B (+12.2%)

- 2017: 2 People

- Loser – 2 People – Pet Spending: $33.36B; Down -$1.96B (-5.6%)

- 2017: 1 Person

- Comment: In a “normal” year 2 people is the magic number. In 2018 the rules changed. 1, 3 or 4 person CUs spent more. 2 and 5+ person CUs spent less. I guess this shows that married couples are “limited” to 2 children.

- Winner – 1 Person – Pet Spending: $14.99B; Up $1.64B (+12.2%)

- Region – The Midwest held on to the winners spot in 2018.

- Winner – Midwest – Pet Spending: $17.76B; Up $1.32B (+8.0%)

- 2017: Midwest

- Loser – Northeast – Pet Spending: $13.85B; Down -$0.97B (-6.6%)

- 2017: West

- Comment – Only the Northeast spent less. The other regions had a combined increase of $2.44B.

- Winner – Midwest – Pet Spending: $17.76B; Up $1.32B (+8.0%)

- # Earners – 1 Earner, 2+ CUs went from Winner to Loser. More earners usually means more income and spending.

- Winner – 2 Earners – Pet Spending: $31.13B; Up $0.89B (+2.9%)

- 2017: 1 Earner, 2+ CU

- Loser – 1 Earner, 2+ CU – Pet Spending: $16.82B; Down -$1.23B (-6.8%)

- 2017: No Earner, Single

- Comment – CUs where everyone works were up $2.34B. Apparently the only situation that the # of earners didn’t matter in 2018 was for Singles – No Earner, Up $0.85B; 1 Earner, Up $0.79B.

- Winner – 2 Earners – Pet Spending: $31.13B; Up $0.89B (+2.9%)

- Race/Ethnic – Same Winner & Loser. White, Not Hispanics account for 86% of Pet $, but only 48% of the increase.

- Winner – White, Not Hispanic – Pet Spending: $67.86B; Up $0.71B (+1.1%)

- 2017: White, Not Hispanic

- Loser – Asian American – Pet Spending: $1.51B; Down -$0.11B (-6.9%)

- 2017: Asian American

- Comment – Only Asian Americans spent less. Hispanics and African Americans spent a total of $0.86B more.

- Winner – White, Not Hispanic – Pet Spending: $67.86B; Up $0.71B (+1.1%)

We’ve now seen the best overall performers and the “winners” and “losers” in terms of increase/decrease in Total Pet Spending $ for 12 Demographic Categories. Not every good performer can be a winner but some of these “hidden” segments should be recognized for their outstanding performance. They don’t win an award, but they deserve….

HONORABLE MENTION

Let’s start with the Millennials. The Gen Xers were the best performers and had the biggest increase, but the Millennials were not far behind with a $3.4B increase. You also see the impact of this youth “movement” in other honorees. The Under 25 group is officially getting in the Pet Parenting game with a 41% spending increase. Married with Children CUs had a $2.4B spending increase but the biggest lift, +45%, came from those with the youngest children and probably younger parents. Homeowners, with and without mortgages had a net spending drop of -$0.08B. Without Renters, the industry would have had no increase in Total Pet $. Renters are also more likely to be younger but there is also a growing number of downsizing older Americans in this segment.

College Grads get all the accolades. However, in 2018 the Associates Degree group was up $1.75B (+22.4%) with 111% performance. In Occupation, it is all about Managers or Self-Employed. The regular white collar workers had a $1.64B increase with 103% performance. Without the contribution of these 2 groups, 2018 Total Pet Spending was down.

Summary

Pet spending increased $12.8B (19.9%) from 2014 to 2017. It was primarily driven by the movement to upgrade to Super Premium Food, but it did not come easy. Value shopping, especially on the internet, and trading $ between segments created turmoil in the industry. Furthermore, 77% of the increase came in 2017. That brings us to 2018.

In 2018, the spending increase was minor, $1.47B (1.9%). This bland increase included a $2.3B drop Pet Food and a $2B record increase in Services. There were also outside factors at work. The FDA warning regarding grain free dog food and added tariffs to Supplies depressed spending in the second half of the year. However, the biggest change was a $6.5B drop in spending by the Baby Boomers. Fortunately, the other groups, especially the younger ones, stepped up to keep things positive but there were some changes in the spending demographics. The demographic groups responsible for most of Total Pet Spending were the same as those in 2017. However, there were changes in their spending share rankings. More Earners and Higher Education moved up in rank and performance, while 35>64 yr olds, Married Couples and Wage/Salary earners fell in rank. In fact, the performance of 7 groups fell indicating more balanced spending.

In terms of performance, the most influential demographic big spending groups remained at 6. However, Income now stands alone at the top with the other 5 clearly on a lower tier. Knowing the demographic segments in these categories allows industry participants to more effectively target their best customers and… those most in need of improvement.

The most significant change in the best and worst performing individual demographic segments was Gen Xers replacing Boomers at the top. The biggest changes occurred in $ and there was turmoil. 13 segments (54%) switched from Winner to Loser or vice versa. Overall, the youth movement was probably the key spending trend in 2018 and is reflected in the increased spending by a number of segments – not just age groups, including Center City, renters, singles and married couples with children. As always, to get to the heart of the matter and to more actionable data you must “drill down”. This will become even more apparent as we turn our analysis to the individual industry segments.

But before we go…The “Ultimate” Total Pet Spending Consumer Unit in 2018 consists of 2 people – a married couple, alone. They are in the 45 to 54 age range. They are White, but not of Hispanic origin. At least one of the them has an Advanced College Degree. They have their own business and are doing well – over $200K. They’re working to pay off their house located in a lovely, small suburb of a metropolitan area with a population of about 3,000,000 in the West.