2020 Pet Food Spending was $36.84B – Where did it come from…?

As we continue to drill ever deeper into the demographic Pet spending data from the US BLS, we have now reached the level of individual Industry segments. We will start with Pet Food, the largest and arguably most influential of all. We have previously noted the trendy nature of Pet Food Spending. In 2018 we broke a pattern which began in 1997 – 2 years up then spending goes flat or turns downward for a year. We expected a small increase in 2018 but what we got was a $2.27B decrease (-7.3%). This was due to the reaction to the unexpected FDA warning on grain free dog food. A pattern of over 20 years was broken by 1 statement. The grain free warning lost some credibility and spending rebounded in 2019, +$2.35B (+7.1%). In 2020 the market was hit by an even bigger outside influence – the pandemic. The impact varied by segment. In Pet Food, it created a wave of panic buying out of fear of shortages, resulting in a $5.65B (18.1%) lift.

First, we’ll see which groups were most responsible for the bulk of Pet Food spending and the $5.65B increase. The first chart details the biggest pet food spenders for each of 10 demographic categories. It shows their share of CU’s, share of pet Food spending and their spending performance (Share of spending/share of CU’s). 3 groups are different from Total Pet – 45>74, < College Grads & the newly created “I’m the Boss” group. The categories are presented in the order that reflects their share of Total Pet Spending. There is one big difference. In 2020 Pet Food spending, older age produced a higher share than higher income. While higher Income performed better in Food, it finished 2nd in importance to being “a boss”. The importance of higher education also plummeted. While Pet ownership is widely spread across demographic segments, in 2020 Pet Food spending was much more targeted in virtually all categories. As you will see in our analysis, that target was older, less educated but still with a high income – younger Baby Boomers. In 2019, Pet Food accounted for 65% of Pet Products $ and 40% of Total Pet. In 2020 the Food share rose to 70.8% in Products and 44.0% of Total Pet. The pandemic caused Pet Parents to focus on “needs” and at the top of that list was Pet Food.

- Race/Ethnic – White, not Hispanic (88.8%) – up from 87.0%. This large group accounts for the vast majority of spending in every segment. They gained in share and their performance increased to 129.9% from 126.9%, but this category fell from #4 to #6 in terms of importance in Pet Food Spending demographic characteristics. While Hispanics, African Americans and Asian Americans account for 31.6% of U.S. CU’s, they spend only 11.2% of Pet Food $. This is down from 17% in 2018. African Americans were the only minority to spend more on Pet Food in 2020, +0.5B which generated a $0.06B, lift for all minorities, about 1% of the +$5.6B increase by White, Not Hispanics.

- Housing – Homeowners (86.7%) – up from 81.9%. Homeownership is a huge factor in pet ownership and more pet spending. In 2020, homeowners gained allmost 5% in share and their performance grew from 128.5% to 131.7%. However, homeownership fell from 3rd to 5th in terms of importance for increased pet Food spending. It was a great year for Homeowners w/o a mortgage but spending fell for renters and especially for those with a mortgage.

- # in CU – 2+ people (82.5%) – up from 80.2%. The share of market for 2+ CU’s is over 80% for Pet Food and Total Pet. Last year they had 80+% in only Pet Food. Their performance grew from 114.9% to 117.5% but their rank fell from 6th to 9th. 5+ CUs were the only segment to increase in number and 4 person CUs drove the lift. Only CUs of 4 or more people performed above 100%. This is a big change from recent years. Singles performance also fell sharply, which helped drive the 2+ group’s increase. In 2020, more people meant more Pet Food spending.

- Area – Suburban + Rural (77.8%) up from 75.5%. Their performance grew from 118.6% to 123.4%. (7th) It was a bad year for large Suburbs (2500>) and a great year for Rural. We had to add the Rural and Suburban numbers together to reach our target of 60+%. Areas under 2500 population now account for 18.9% of CUs but 47.6% of Pet Food $.

- # Earners – “Everyone Works” (70.7%) – up from 66.4%. This was a big increase from last year and their performance also grew sharply from 113.6% to 123.3%. They only rank 8th but they now are in the 120+% club.

- CU Composition – Married Couples (71.1%) – up from 63.0%. They gained in share and their performance grew from 129.0% to 146.6%, but they fell from 2nd to 3rd. Only Married couples with an oldest child over 6 spent more.

- Income – Over $70K (65.3%) – up from 60.9%. Their performance rating also grew from 146.9% to 150.2% but they fell from 1st to 2nd in importance. High income is still very important in Pet Food Spending. In fact, the bar was raised in 2020. $100K+ CUs now account for 55% of Pet Food $. In 2019 their share was 42%. The $70>100K group had a bad year and other factors like occupation came to the forefront in the pandemic. Pet ownership is common across all income levels but in 2020 higher income remains critically important in Pet Food Spending.

- Age – 45>74 (68.6%) – up from 62.6%. This older group replaced 35>64 yr-olds and their performance grew from 124.3% to 132.2% so the “Age” category ranked #4 in importance. 45>64 is in both groups and 55>64 was the big driver. The change came because the 65>74 share grew from 15.7% to 16.1% while 35>44 fell from 16.0% to 11.9%.

- Education – Less than College Grads (57.9%) – up from 50.4%. Higher Education continues to fall in importance in Pet Food Spending as those without a degree gained share and their performance grew from 90.6% to 108.7%. Higher education, specifically a college degree, is now the least important factor in increased Pet Food Spending.

- Occupation – I’m the Boss – Mgrs/Profess/Self-Employed (58.5%) – up from 38.7% – Spending by Blue Collar workers and lower level White Collar workers fell while the spending by the “Bosses” took off. Their performance grew from 123.2% to 175.1% and amazingly moved Occupation to the top spot in Pet Food Spending importance.

Only 7 of the big spenders for Pet Food are the same as those for Total Pet and they generally performed better in Food. This is a marked contrast from past years. In 2020, Pet Food Spending grew $5.65B and all 7 of the matching groups gained in both share and performance. Pet Food spending became much less balanced which is best illustrated by the need for 3 new big groups and the fact that the performance of 8 of the groups exceeds 120%.

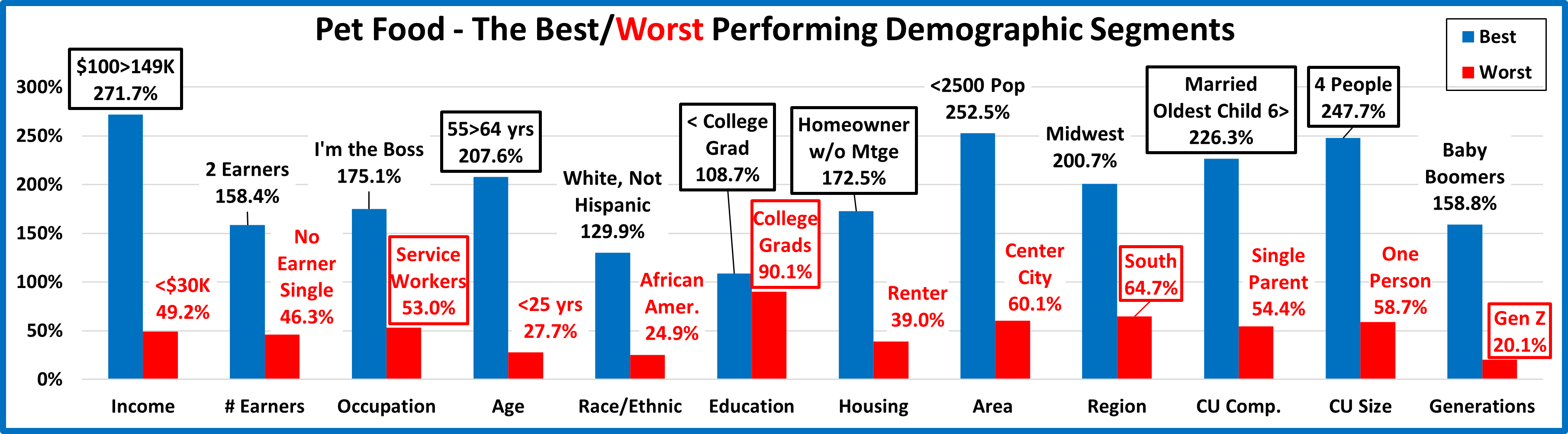

Now, we’ll look at 2020’s best and worst performing Pet Food spending segments in each category.

Many of the best and worst performers are the ones that we would expect but 2020 produced some surprise winners – <College Grads, Homeowners w/o Mtges, Married, Oldest Child 6>, 4 People CUs, and 1 surprise loser – College Grads. There are 10 that are different from 2019. This is 3 more than last year and 4 more than for Total Pet this year. Changes from 2019 are “boxed”. We should note:

- Income is important in every segment, but the Food winner makes less than the winner in other segments. However, the Food segment’s influence is so strong that it pushed the Total Pet winner down to $100>149K.

- Occupation – Service Workers replaced Retirees at the bottom, but you still see the importance of Income in Food.

- Age – The 55>64 yr olds (high income “Boomers”) returned to the top but the <25 group stayed on the bottom.

- Education – In 2020, having a College Degree truly did not matter in Pet Food Spending.

- Housing – Owning a home is always important. In 2020, some of the extra $ available from having a paid off mortgage were used to spend more on Pet Food.

- CU Composition – Married, Couples Only had won for 5 years in a row. Now, having older kids is more important.

- CU Size – 2 Person CUs used to be the perennial winner. Last year it was 3 people and in 2020 it moved up to 4.

- Generation – Boomers remain the best performers in Pet Food, but the youngest replaced the oldest at the bottom.

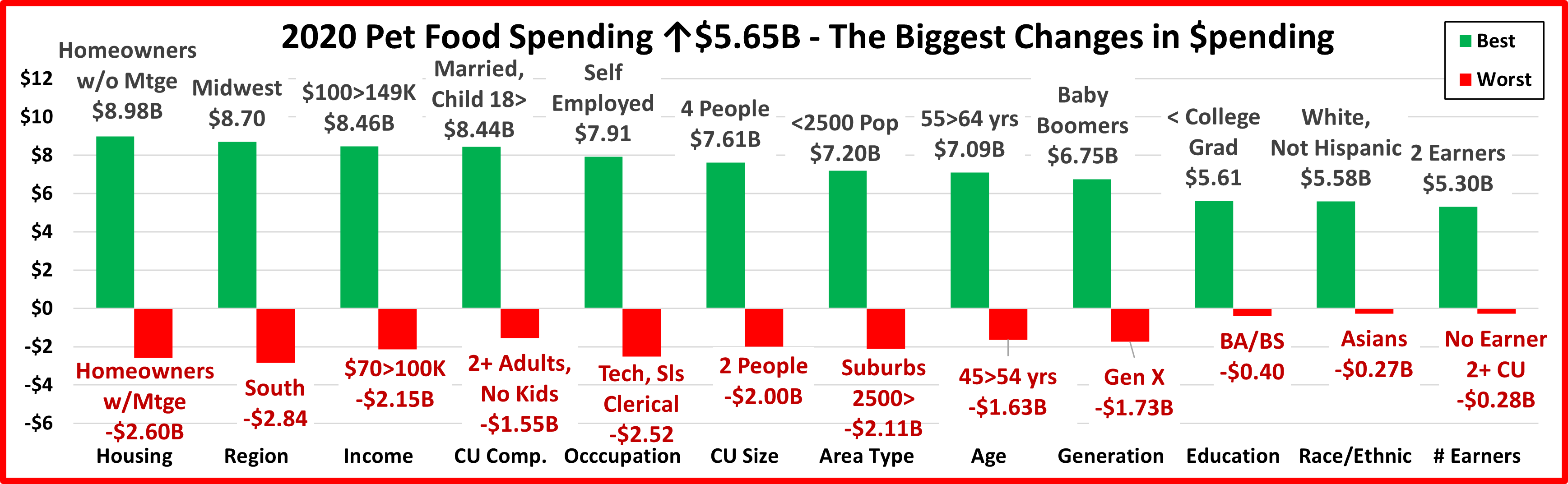

It’s time to “Show you the money”. Here are segments with the biggest $ changes in Pet Food Spending.

There are just 3 repeats from 2019 so 21 of the 24 segments (88%) are new, including 5 that flipped from 1st to last or vice versa. The winner and loser in Education and Housing are surprising but the biggest trend to note is the size of the increases in the winners. This shows the overall increase in Pet Food spending in 2020 was not widespread like 2019 but rather driven by very specific groups. Here are the specifics:

- Housing – Homeowners w/Mtges flipped from first to last.

- Winner – Homeowners w/o Mtge – Food: $17.18B; Up $8.98B (+109.4%) 2019: Homeowners w/Mtge

- Loser – Homeowners w/Mtge – Food: $14.75B; Down $2.60B (-15.0%) 2019: Renters

- Comment – Renters also spent less so the Food increase came solely from Homeowners with a paid off mortgage. However, it wasn’t driven by Retirees. 90% of the increase in Food $ came from those still working.

- Region – The 2019 winner and loser flipped positions.

- Winner – Midwest – Pet Food Spending: $15.72B; Up $8.70B (+123.9%) 2019: South

- Loser – South – Pet Food Spending: $9.19B; Down $2.84B (-23.6%) 2019: Midwest

- Comment – Last year all regions spent more. This was the 3rd consecutive year in which the spending change, whether up or down, was the same for all regions. In 2020, that pattern changed as only the Midwest and West spent more.

- Income – The income winner continues to trend down. $100>149K group won. In 2019, it was the $150>199K group.

- Winner – $100 to $149K – Pet Food Spending: $14.38B; Up $8.46B (+142.9%) 2019: $150 to $199K

- Loser – $70 to $100K – Pet Food Spending: $3.75B; Down $2.15B (-36.4%) 2019: $30 to $39K

- Comment – Truly a spending rollercoaster: <$40K: +$1.52B;$40>99K:-$3.07B;$100>149K:+$8.46K; $150>199K: -$1.68B;$200K>: +$0.43B.

- CU Composition – CU’s with Children, especially older children, came to the forefront.

- Winner – Married, Oldest Child 18> – Food: $11.74B; Up $8.44B (+256.1%) 2019: Married, Couple Only

- Loser – 2+ Adults, No Kids – Food: $3.20B; Down $1.55B (-32.6%) 2019: Single Parents

- Comment – In 2019, 85% of the increase came from all adult CUs – Singles & 2+ CUs, married or unmarried – just no kids. In 2020, the spending behavior essentially flipped. Singles again spent more but overall, CUs with kids, including Single Parents, spent $8.81B more while all adult CUs with no kids spent $3.16B less.

- Occupation – Self-Employed won for the 3rd consecutive year.

- Winner – Self-Employed– Pet Food Spending: $11.29B; Up $7.91B (+234.2%) 2019: Self-Employed

- Loser – Tech, Sales, Clerical – Pet Food Spending: $2.99B; Down $2.52B (-45.8%) 2019: Retired

- Comment – Those with more control, Self-Employed, Managers & Professionals and Retirees, spent more. With the exception of Service Workers, who spent 1.8% more, all other occupations, blue and white collar, spent less.

- # in CU – After 2 straight wins, 3 People CUs was replaced at the top by 4 person CUs.

- Winner – 4 People – Pet Food Spending: $11.56B; Up $7.61B (+192.8%) 2019: 3 People

- Loser – 2 People – Pet Food Spending: $10.77B; Down $2.00B (-15.7%) 2019: 5+ People

- Comment: Although Singles again had an increase, the movement to larger CUs continues as 4+ CUs spent $9.3B more. The previously magic “2” number continues to decline.

- Area Type – In 2020, driven by Rural, the lower population areas continued to spend more.

- Winner – All Areas <2500 – Pet Food Spending: $17.54B; Up $7.20B (+69.7%) 2019: Suburbs <2500

- Loser – Suburbs 2500> – Pet Food Spending: $11.12B; Down $2.11B (-15.9%) 2019: Center City

- Comment – Only Cities with a population above 5 million and areas with a population under 2500 spent more. The larger Suburbs, 2500+ people, took the biggest hit, -$2.11B. Their share of Pet Food $ fell from 42% to 30%.

- Age – The highest income group, 45>54 flipped from the top to the bottom.

- Winner – 55>64 yrs – Pet Food Spending: $14.63B; Up $7.09B (+94.0%) 2019: 45>54 yrs

- Loser – 45>54 yrs – Pet Food Spending: $5.45B; Down $1.63B (-23.1%) 2019: <25 yrs

- Comment: Although the 55>64 yr olds drove almost all of the increase, there was another spending rollercoaster. <25: -$0.37B; 25>34: +$0.87B; 35>54: -$2.24B; 55>74: +$7.41B; 75>: -$0.02B.

- Generation – Boomers are back on top, while Gen X flipped from 1st to last.

- Winner – Baby Boomers – Pet Food Spending: $19.31B; Up $6.75B (+53.7%) 2019: Gen X

- Loser – Gen X – Pet Food Spending: $8.29B; Down $1.73B (-17.3%) 2019: Born <1946

- Comment – Much of the Pet Food spending lift was an emotional reaction to the pandemic so it is not surprising that Boomers, the 1st pet parents, led the way. Another rollercoaster – Gen Z, Gen X and those born before 1946 all spent less while Millennials and Boomers spent more.

- Education – Higher education has been becoming less important in Pet Food spending. The trend continues.

- Winner – <College Grad – Food Spending: $21.33B; Up $5.61B (+35.7%) 2019: HS Grads

- Loser – BA/BS Degree – Food Spending: $7.75B; Down $0.40B (-4.9%) 2019: <HS Grad

- Comment – Driven by those with an advanced degree, College Grads did spend $0.04B more. However, almost all of the 2020 spending lift came from those without a degree.

- Race/Ethnic – White, Not Hispanic kept their position at the top.

- Winner –– White, Not Hispanic – Pet Food Spending: $32.73B; Up $5.58B (+20.6%) 2019: White, Not Hispanic

- Loser ––- Asians – Pet Food Spending: $0.43B; Down $0.27B (-38.4%) 2019: Hispanic

- Comment – The U.S. is slowly becoming more racially/ethnically diverse but White, Not Hispanic is still by far the biggest spender in every Pet Industry Segment. In 2020 their share of Food spending hit 88.8%, the largest in any segment. African Americans also spent more on Pet Food in 2020, but Asians and Hispanics spent less.

- # Earners – 2 Earner CUs kept their place at the top and accounted for 94% of the Pet Food Spending lift.

- Winner –– 2 Earners – Pet Food Spending: $18.28B; Up $5.30B (+40.8%) 2019: 2 Earners

- Loser – No Earner, 2+ CU – Pet Food Spending: $2.48B; Down $0.28B (-10.3%) 2019: 1 Earner, 2+ CU

- Comment – As we have seen, an income over $100K is important as it occupation. While everyone works CUs now perform above 120%, the real key to increased Pet Food spending is having 2 or more earners.

We’ve now seen the “winners” and “losers” in terms of increase/decrease in Pet Food Spending $ for 12 Demographic Categories. 1n 2019, the rebound lift from the FDA warning was widespread. In 2020, the big spending lift due to the pandemic occurred in very specific segments. Most of America remains firmly committed to high quality Pet Food. However, super premium Food comes with high prices, so income has grown in importance in Pet Food spending. I suspect that the internet and value shopping will become even more important in this segment. We have identified the winning segments in performance and $ increase but they were not alone. Not every good performer can be a winner. Some “hidden” segments should also be recognized for performance. They don’t win an award, but they get…

HONORABLE MENTION

5+ Person CUs came in 2nd to 4 person CUs but this is also representative of the movement in food spending to larger CUs. Single Parents have the lowest performance in the category, but it is improving. African Americans have the lowest income and lowest percentage of pet ownership, but they are still committed to the wellbeing of their Pet Children. In recent years, Millennials have led the way in Pet Food spending trends. Their behavior was then followed by their Boomer parents. In 2020, the situation was reversed as many got on board with the move by the older group. Managers and Professionals have very high income and often lead the way in spending trends, especially in the era of super premium foods. In 2020, they finished second behind the incredible lift by the self-employed group.

Summary

Pet Food has been ruled by trends over the years. The drop in 2018 due to the FDA grain free warning broke a pattern of 2 years up followed by 1 year of flat or declining sales which had been going on since 1997. This trendy nature increased with the first significant move to premium foods in 2004. The Melamine crisis in 2007 intensified the pattern and resulted in a series of “waves” which became a tsunami with the introduction of Super Premium Foods.

The 25 to 34 yr old Millennials were the first to “get on board” with Super Premium in the second half of 2014. In 2015 a substantial portion of consumers began to upgrade to this new trend. The result was a $5.4B spending increase. These consumers were generally more educated, often worked as managers or were self-employed and had higher incomes. One negative was that they often paid for the upgrade by spending less in other segments. In 2016 the anticipated drop in spending happened. The “upgraded” group began value shopping for their new food and found great deals online and in some stores. They spent some of the $3.0B “saved” Food dollars in other segments but not enough to make up for the drop in Food. Total Pet Spending was down $0.46B. In 2017 we were ready for a new “wave”. Thanks to a very price competitive market, what we got was a deeper penetration of Super Premium foods. This group of upgraders was mostly middle-income, not college educated and often Blue-collars workers. Most also were in the 55>64 year old age group. The result was a $4.6B increase but this time there was no trading $ with other segments.

In 2018 we were “due” a small annual increase in Pet Food and spending in the first half was up $0.25B. Then the bottom dropped out as spending fell $2.51B in the second half in reaction to the FDA warning on grain free dog food. It turned out that the big decrease in pet food spending came directly from the groups who had fueled the big 2017 increase. This turmoil was illustrated by the fact that 71% of the demographic groups with the biggest change in Pet Food $ switched from first to last or vice versa from their position in 2017.

That brought us to 2019. The impact of the FDA warning faded as there was little evidence to back it up. Pet Parents either returned to Super Premium or chose even higher priced options. Supplement $ also grew as the health and wellbeing of their Pet Children remained the #1 priority. Pet Food $ grew $2.35B with 75% of demographic segments spending more. Education became less important but income and related categories mattered more. Pet Food Spending became a little less demographically balanced in 2019 and the 2020 Pandemic accelerated this trend. Fear of shortages led to binge buying and a $5.65B increase. This behavior was driven by very specific groups, including 55>64 yr old Boomers, Self-Employed & Managers, Homeowners w/o Mtges, $100>149K incomes and less populated areas. This spending disparity was manifested in the fact that the performance of 8 of 10 big spending groups exceeded 120% while 49% of all segments spent less. The retail market strongly recovered in 2021. We’ll see if/how this impacted Pet Food $.

Finally – 2020’s “Ultimate” Pet Food Spending CU is 4 people – a married couple, with at least 1 child over 18. They are 55>64 years old and White, but not of Hispanic origin. Neither graduated from college but they both work in their own business. They earn $100>$150K but have paid off the mortgage on their house in a rural area in the Midwest.