We looked at the Total Pet Spending for 2016 and its key demographic sources. Now it’s time to start drilling down into the data. We will ultimately look at each individual segment but the first stop in our journey of discovery will be Pet Products – Pet Food and Supplies. Taken as a total, this classification accounted for $42.34B (63%) of the $67.29 in Total Pet spending in 2016. This was down $2.05B (-4.5%) from the $44.39B that was spent in 2015. We have seen that this drop in spending came largely as a result of intense value shopping for premium foods. It’s also important to remember that although the products’ share of spending fell slightly from (65%) in 2015, Food and Supplies are the industry segments that are most familiar to consumers. They are stocked in over 200,000 U.S. retail outlets, including over 17,000 Vet Clinics, plus the internet. Every week over 20,000,000 U.S. households buy food and/or treats for their pet children.

Pet Food spending dropped by $2.99B in 2016 but at the same time spending on Pet Supplies spending increased by $0.94B. We’ll bundle them together and see where the bulk of Pet Products spending comes from?

We will proceed with the same methodology that we used in our Total Pet Analysis. First, we will look at Pet Products Spending in terms of 10 demographic categories to determine what groups are responsible for 60+% of the spending. Then we will look for the best and worst performing segments in each category and finally, the segments that generated the biggest dollar gains or losses in 2016.

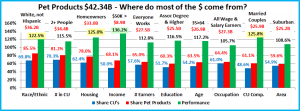

The first chart details the biggest pet product spenders for each demographic category. It shows their share of CU’s, share of pet products spending and their spending performance (Share of spending/share of CU’s). Although their share of the total products $ may be different from their share of the Total Pet $, all of the big spending groups are the same. The categories are presented in the order that reflects their share of Total Pet Spending. This highlights the differences in importance. In Pet Products spending, higher education is less important while the wage and salary earners have a slightly higher share of the business. We should also note that, like Total Pet Spending, Income is the highest performing demographic characteristic. However, for Pet Products there are only 4 groups with a performance rating of over 120%. Total Pet had 5. This indicates that Pet Products spending is spread a little bit more evenly across the category segments.

- Race/Ethnic – White, not Hispanic (85.5%) This is the largest group and accounts for the vast majority of spending in every segment. With a 122.5% performance rating, this category ranks #4 in terms of importance in Pet Products Spending demographic characteristics. While Hispanics, African Americans and Asian American account for over 30% of U.S. CU’s, they spend less than 15% of Pet Products $. Although pet ownership is relatively high in Hispanic American households, it is significantly lower for African Americans and Asian Americans.

- # in CU – 2+ people (81.2%) The spending numbers for Pet Products are very close to those for Total Pet. If you put 2 people together pets very likely will follow. If you have a pet, you must spend money on food and supplies. Their overall performance of 115.5% is lower because performance decreases as the number of people in the CU increases. However, it is still relatively high at 85.5% for CU’s with 5 or more people. The key is “It just takes two.”

- Housing – Homeowners (78.0%) Controlling your “own space” has long been the key to pet ownership, larger pet families and more pet spending. At 125.0% performance, homeownership ranks 3rd in terms of importance for increased pet products spending. Since Homeownership relates directly to pet ownership and spending, the lower homeownership rate for Millennials should be a concern for the future of the industry.

- Income – Over $50K (68.1%) Pet Parenting is common in all income groups but money (income) does matter in spending behavior for all industry segments. With a performance rating of 136.2%, CU income is also the single most important factor in increased Pet Products Spending. We have the same anomalies of behavior as we had with Total Pet. Older Americans spend more on their pets than their income would suggest and the higher income, Asian Americans spend much less. However, as a general rule, Higher Income = Higher Pet Products Spending.

- # Earners – “Everyone Works” (65.0%) In this group, all adults in the CU are employed. This group’s high share of pet products spending is more evidence of the growing importance of income in pet products spending. However, the performance of 112.8% is slightly lower than Total Pet. It is also much lower than that of the income category. Remember, retired folks and CU’s with 2+ people and only one earner have a lot of pets and spend a lot of money.

- Occupation – All Wage & Salary Earners (64.4%) – Pet ownership is widespread across all segments in this group. The low performance, 105.7% demonstates this and also reflects the substantial contributions being made by the Self-employed and retired groups.

- Age – 35>64 (63.5%) In recent years the 45>74 year age group dominated the spending. With the Baby Boomers value shopping for premium Pet Food and the Gen Xers buying significantly more supplies, the bulk of Pet Products spending shifted slightly. The 65>74 group was edged out in Pet Products spending by the 35>44 group. The overall 35>64 age group includes the 3 highest income levels so this change isn’t a total surprise. The 117.2% performance level indicates that pet parenting is common among all ages.

- CU Composition – Married Couples (61.1%) Pet parenting and marriage both represent strong commitments. With a performance of 125.8% marriage moves up to second place in terms of importance to Pet Products spending.

- Education – Associates Degree or Higher (60.3%) Pet Products Spending generally increases with education. However, much of Pet Products spending is about buying the things that are absolutely required in order to be a good Pet Parent. With a performance level of 116.5%, higher education dropped out of the top 5 and fell below the “magic” 120% level. This truly indicates how widespread pets are across all education levels in America.

- Area – Suburban (59.6%) Suburban households are still the biggest pet spenders, but the relatively low market share and low performance of 108.6% indicate that more and more pets are finding homes in Central Cities.

The biggest spending groups are the same for Pet Products as for Total Pet. However, there are subtle differences in market share and in performance. Money still matters most but there are only 4 groups performing above the 120% level in Pet Products spending, one less than in Total Pet. In general, the Pet Product spending analysis better represents the demographic diversity of Pet ownership in the U.S.

Now, let’s drill deeper and look at 2016’s best and worst performing Products spending segments in each category.

Most of the best and worst performers are the ones that we would expect. There are only 5 that are different from 2015 but that is 2 more than for Total Pet. Changes from 2015 are “boxed”. We should note:

- Income is growing more important as the 205% performance is up 9.6% from last year. This increase is magnified as it comes in a year in which the performance of the average winner fell 14% and that of the average loser rose 4%. Except for income, spending is becoming more diverse across the segments in demographic categories.

- CU Composition – Last year the winner was married couples with a child over 18. This year it is the married couple only. The exceptionally high performance reflects the influence of Millennials just getting started added to that of the aging Baby Boomers. Single Parents replaced Singles as the lowest performing segment in this category. This is understandable as they are generally under intense financial pressure.

- Region – The South had a great year and they wrested the top spot from the perennial winner, the West. Although the Northeast finished last again, their performance radically improved from 79.7% in 2015. Spending on Pet Products seems to be becoming more balanced across the regions.

- # Earners – Money matters and 2+ earners generally means higher income. This year 2 Earner CU’s just edged out the 3 Earner CU’s for the top spot.

- Age – The Under 25 group improved their performance slightly (+1%) in 2016 but they fell into the bottom spot because the performance of the Over 75 group jumped from 39% to 54% – an amazing improvement!

It’s time to “Show you the money”. Here are segments with the biggest $ changes in Pet Products Spending.

In this section we will see just how tumultuous 2016 was. There are no repeats from 2015. In 2 categories the 2015 winners and losers switched positions. In 3 other categories, last year’s winner is this year’s loser. However, there are also other surprises, like the performance of the 75+ age group and the good and bad performance of no earner CU’s.

- Area Type – The Central City had the single biggest increase of any demographic segment.

- Winner – Central City – Products: $12.19B; Up $2.28B (+23.0%)

- Loser – Suburbs >2500 – Products: $18.43B; Down $1.82B (-9.0%)

- Comment – The largest Suburbs, the area with the biggest share of the business, had the biggest decrease.

- Occupation – The traditionally big spending self-employed group value shopped their way to a big decrease.

- Winner – Tech, Sales & Clerical – Products: $7.14B; Up $1.32B (+22.6%)

- 2015: Mgrs. & Professionals

- Loser – Self-employed – Products: $3.66B; Down $1.32B (-26.5%)

- 2015: Operators & Laborers

- Comment – The Tech, sales & clerical group’s increase is even more impressive, considering the fact that they have 4% fewer CU’s. For the first time, their Pet Products’ spending exceeds the national CU average.

- CU Composition – The big spending changes usually come from some sub-segment of married couples. However…

- Winner – Unmarried, 2+ Adults – Products: $7.25B; Up $0.92B (+14.5%)

- 2015: Married Couple Only

- Loser – Married, oldest child >18 – Products: $3.73B; Down $1.21B (-24.5%)

- 2015: Married All Children <18

- Comment – Unmarried, 2+ adults and married couples with their oldest child under 6 were the only segments in this category to have an increase. This is corroborating evidence of the positive impact of the younger groups.

- Income – Last year’s winner and loser just swapped places in 2016. Value shopping for Food created turmoil.

- Winner – $70 to $99K – Products: $7.77B; Up $0.83B (+12.0%)

- Loser – $100 to $149K – Products: $7.18B; Down $1.38B (-16.1%)

- Comment – The loser wasn’t the biggest loser in either Food or Supplies but spending fell significantly in both.

- Region – Last year’s winner is this year’s biggest loser. Out West, it was all about Value shopping for Food.

- Winner – Northeast – Products: $7.20B; Up $0.74B (+11.5%)

- Loser – West – Products: $9.70B; Down $2.21B (-18.6%)

- Comment – The success of the Northeast is directly related to the great increase in Central City spending.

- Housing – In 2015 all segments had an increase in Pet Products spending. In 2016, there is only one.

- Winner – Renters – Products: $9.31B; Up $0.63B (+7.2%)

- Loser – Homeowner w/o Mtge – Products: $10.24B; Down $2.26B (-18.1%)

- Comment – Another big position switch which reflects the “youth spending lift” and the Boomer decline.

- Age – Ready for a really big surprise? The Silent generation spoke up in 2016.

- Winner – 75+ yrs – Products: $2.27B; Up $0.57B (+33.4%)

- Loser – 55>64 yrs – Products: $10.76B; Down $2.61B (-19.5%)

- Comment: All the groups under 45 increased Products’ spending but they were all up and down between food and supplies. The over 75 group was the only age group with increased spending on both food and supplies.

- Education – Apparently College prepares you for a lot of things, including value shopping for Food…down $2.66B

- Winner – Associates Degree – Products: $5.25B; Up $0.56B (+11.9%)

- Loser – BA/BS Degree – Products: $11.08B; Down $1.42B (-11.4%)

- Comment – CU’s with an Associates’ Degree or a HS diploma and some college credits were the only segments with increased spending on Pet Products. BA/BS wasn’t the worst in Supplies or Food but spending fell in both.

- Race/Ethnic – 85.5% of Pet Products’ Spending comes from White, Non-Hispanics so even a small change = Big $.

- Winner – Hispanic – Products: $3.51B; Up $0.28B (+8.8%)

- 2015: White. Not Hispanic

- Loser – White, Not Hispanic – Products: $36.18B; Down $2.6B (-6.7%)

- Comment – In addition to Hispanics, both African Americans and Asian Americans increased their Pet Products spending in 2016. African Americans came in 2nd with a $0.21B increase and they were also the only group in this demographic category to spend more on both food and supplies.

- # Earners – More earners generally means a higher income and more Spending, so no Earners means….

- Winner – No Earner, Single – Products: $2.73B; Up $0.19B (+7.3%)

- Loser – No Earner, 2+ in CU – Products: $3.36B; Down $1.05B (-23.8%)

- 2015: 2+ in CU with 1 Earner

- Comment – The loser is understandable. There were only 2 segments with increased spending in this category – 2 earners and no earner, singles. The no earner, single CU wasn’t a winner in either Food or Supplies. They won Products by being 75+, living alone in a rental property in a Central City with a retirement income of $30>40K.

- # in CU – In 2016 only CU’s with 4 people showed increased Pet Products spending.

- Winner – 4 People – Products: $5.70B; Up $0.11B (+2.1%)

- Loser – 5+ People – Products: $3.44B; Down $0.79B (-18.7%)

- Comment: 4 person CU’s had increased spending on Food but bought slightly less Supplies. There are 3 other segments in different categories that match that pattern – married couples with the oldest child under 6, the 25>34 year age group and of course, Millennials.

We’ve now seen the “winners” and “losers” in terms of increase/decrease in Pet Products Spending $ for 11 Demographic Categories. It has truly been an eye opener. In 5 cases last year’s winner was this year’s loser. We have seen evidence of the significant contributions made by the younger groups in 2016 and we have had some truly surprising winners like the over 75 age group, no earner – singles and renters. Of course, not every good performer can be a winner but some of these “hidden” segments should be recognized for their outstanding performance. They don’t win an award but they deserve….

Honorable Mention

Pet Products spending was down over $2B in 2016 so any increase is significant. These 5 groups were not the best performers or groups with the biggest $ increase. However, together they generated an increase of $1.6B in Pet Products spending. The HS Grads with some college and the 35>44 age group together produced an extra $1B. African Americans and Construction Workers & Mechanics had a big percentage increase. The $30>39K group had the only spending increase by a group making under $70K.

Summary

In both 2015 and 2016 we saw significant changes in spending behavior which strongly impacted the Pet Products sector of the industry. In 2015 a large number of households opted to upgrade to Super Premium foods. This resulted in a huge increase in Food spending but also reduced spending in other segments, especially Supplies. In 2016, consumers began a concerted effort to find the best price on their premium pet foods. They were successful and they saved a lot of money – $2.99B. This freed up funds for increased spending in the other segments, including $0.94B on Supplies.

On the surface, this seems like a very simple explanation – spent much less on Food and somewhat more on Supplies. Just do the addition and subtraction and our analysis should be done. However, as we have learned, “simple” rarely applies in the Pet Industry. This is especially true of the Pet Products sector. Food and Supplies represent roughly 2/3 of all Pet Spending but it is more than just $.

Spending money on Food and Supplies is an absolute necessity in Pet Parenting. Obviously, your pet needs food every day so you must buy it regularly and often. Although Supply items are somewhat more discretionary in nature there are plenty of supplies that are also necessities for good pet parenting. Depending on the pet, you need things like a collar and lead, a feeding bowl and cat litter. Even durable dog toys are a “must have” in some situations. The big difference between Food and Supplies is the frequency of purchase. On average, Food is bought about every 3 weeks. Consumers buy dog toys every month or two. Collars are purchased annually at best and feeding bowls are bought about every 5-6 years. Cat litter is purchased on a regular routine because it is definitely a “must have” item for cat owners.

Because of the necessity, the spending behavior on Pet Products can be a more important reflection of the percentage of pet ownership in a demographic category than the data for Total Pet. The performance of a group is also very important. We identified three demographic categories with high performing large groups. (There were 4 for Total Pet)

- Income

- Homeownership

- CU Composition

Increased income, homeownership and being married all generate increased pet products spending. These are all demographic characteristics in which the consumer has some control. The demographic segments in these categories allow industry participants to more effectively target their best customers and… those most in need of improvement.

Regarding big spenders, the age group skewed a little younger this year but there was very little change in the best and worst performing individual segments. The big changes occurred in $. There were some surprising winners – Central City, 75+ yrs & No Earner Singles, to name a few. Next up: We will drill even deeper into the Food & Supplies Segments.

Finally…The “Ultimate” Pet Products Spending Consumer Unit is down to 2 – a married couple, alone – their last child finally moved out. They are still in the 55 to 64 age range. They are White, but not of Hispanic origin. At least one of them has an advanced College Degree. They both still work in their own business and they’re earning over $200K. They still have a mortgage on their house located in a small suburb adjacent to a big city in the South. (Total Pet was West)