Petflation 2023 – September Update: Drops again to +5.7% vs 2022

While inflation is slowing, it is still a concern. The huge YOY increases in the monthly Consumer Price Index peaked in June 2022 at 9.1% then began to slow until turning up in July & August 2023. In September prices grew 0.2% from August but the CPI remained stable at +3.7% vs 2022. However, Grocery inflation continued to drop. After 12 straight months of double-digit YOY monthly increases, grocery inflation is down to +2.4%, 7 consecutive months below 10%. As we have learned, even minor price changes can affect consumer pet spending, especially in the discretionary pet segments, so we will continue to publish monthly reports to track petflation as it evolves in the market.

Petflation was +4.1% in December 2021 while the overall CPI was +7.0%. The gap narrowed as Petflation accelerated and reached 96.7% of the national rate in June 2022. National inflation has slowed considerably since June 2022, but Petflation generally increased until June 2023. It passed the National CPI in July 2022 and at 5.7% in September, it is still 1.5 times the national rate of 3.7%. We will look deeper into the numbers. This and future reports will include:

- A rolling 24 month tracking of the CPI for all pet segments and the national CPI. The base number will be pre-pandemic December 2019 in this and future reports, which will facilitate comparisons.

- Monthly comparisons of 23 vs 22 which will include Pet Segments and relevant Human spending categories. Plus

- CPI change from the previous month.

- Inflation changes for recent years (21>22, 20>21, 19>20, 18>19)

- Total Inflation for the current month in 2023 vs 2019 and now vs 2021 to see the full inflation surge.

- Average annual Year Over Year inflation rate from 2019 to 2023

- YTD comparisons

- YTD numbers for the monthly comparisons #2>4 above

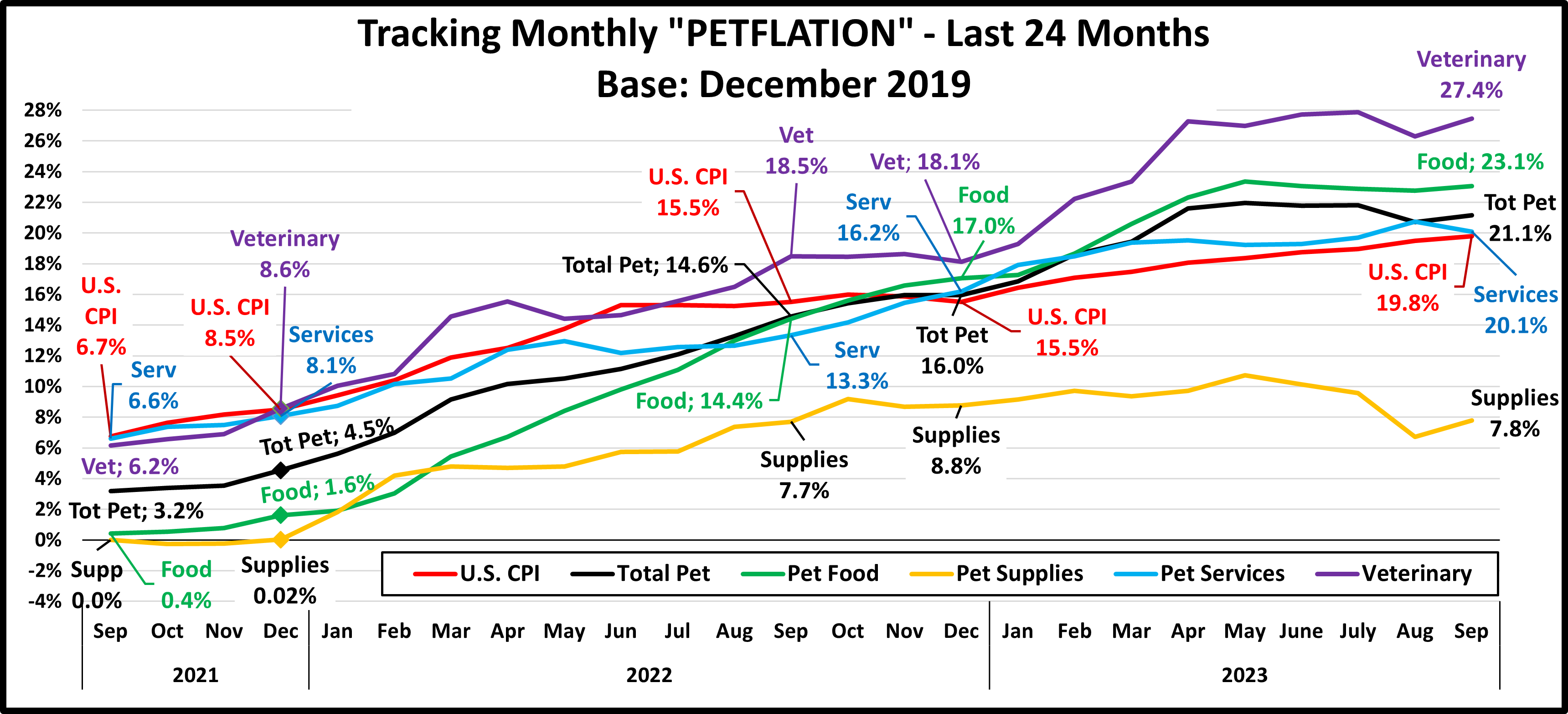

In our first graph we will track the monthly change in prices for the 24 months from September 2021 to September 2023. We will use December 2019 as a base number so we can track the progress from pre-pandemic times through an eventual recovery. Inflation is a complex issue. This chart is designed to give you a visual image of the flow of pricing. You can see the similarities and differences in patterns between segments and compare them to the overall U.S. CPI. The current numbers plus yearend and those from 12 and 24 months earlier are included. This will give you some key waypoints. In September, Pet prices were up from last month overall and in all segments but Non-Vet Services.

In September 21, the CPI was +6.7% and Pet prices were +3.2%. Like the CPI, prices in the Services segments generally inflated after mid-2020, while Product inflation stayed low until late 21. In 22 Petflation took off. Food prices grew consistently but the other segments had mixed patterns until July 22, when all increased. In Aug>Oct Petflation accelerated. In Nov>Dec, Services & Food prices continued to grow while Vet & Supplies prices stabilized. In Jan>Apr, prices grew every month except for 1 dip by Supplies. In May Products prices grew while Services slowed. In June/July this was reversed. In August all but Services fell. In September this pattern was reversed. Petflation has been above the CPI since November 2022.

- U.S. CPI – The inflation rate was below 2% through 2020. It turned up in January 21 and continued to grow until flattening out in Jul>Dec 22. Prices turned up again in Jan>Sep but 34% of the overall 19.8% increase in the 45 months since December 2019 happened in the 6 months from January>June 2022 – 13% of the time.

- Pet Food – Prices were at or below December 2019 levels from Apr 20>Sep 21. They turned up with a sharp lift in Dec which continued until the Jun>Aug 23 dip. Prices then grew in September. 93% of the 23.1% increase since 2019 has occurred since 2022.

- Pet Supplies – Supplies prices were high in December 2019 due to the added tariffs. They then had a “deflated” roller coaster ride until mid-2021 when they returned to December 2019 prices and essentially stayed there until 2022. They turned up in January and hit an all-time high, beating the 2009 record. They plateaued Feb> May, grew in June, flattened in July, then turned up in Aug>Oct setting a new record. Prices stabilized in Nov>Dec but turned up in Jan>Feb 23, a new record. They fell in March, set a record in May, fell in Jun>Aug then grew in September.

- Pet Services– Normally inflation is 2+%. Perhaps due to closures, prices increased at a lower rate in 2020. In 2021 consumer demand increased but there were fewer outlets. Inflation grew in 2021 with the biggest lift in Jan>Apr. Inflation was stronger in 2022 but it got on a rollercoaster in Mar>June. It turned up again July 22>Mar 23 but the increase slowed to +0.1% in April. Prices fell -0.3% in May, turned up again in Jun>Aug, then fell in September.

- Veterinary – Inflation has been consistent in Veterinary. Prices turned up in March 2020 and grew through 2021. A surge began in December 21 which put them above the overall CPI. In May 22 prices fell and stabilized in June causing them to fall below the National CPI. However, prices turned up again and despite some dips they have stayed above the CPI since July 22. In 2023 prices grew Jan>May, stabilized Jun>Jul, fell in August, then increased in September.

- Total Pet – Petflation is a sum of the segments. In December 21 the pricing surge began. In Mar>Jun 22 the segments had ups & downs, but Petflation grew again from Jul>Nov. It slowed in December, turned up Jan>May 23, fell in Jun>Aug, then grew in September. Except for 5 individual monthly dips, prices in all segments increased monthly Jan>Jun 23. In Jul>Aug there 5 more dips but only 1 in September – Services. Petflation has been above the U.S. CPI since November. 2022.

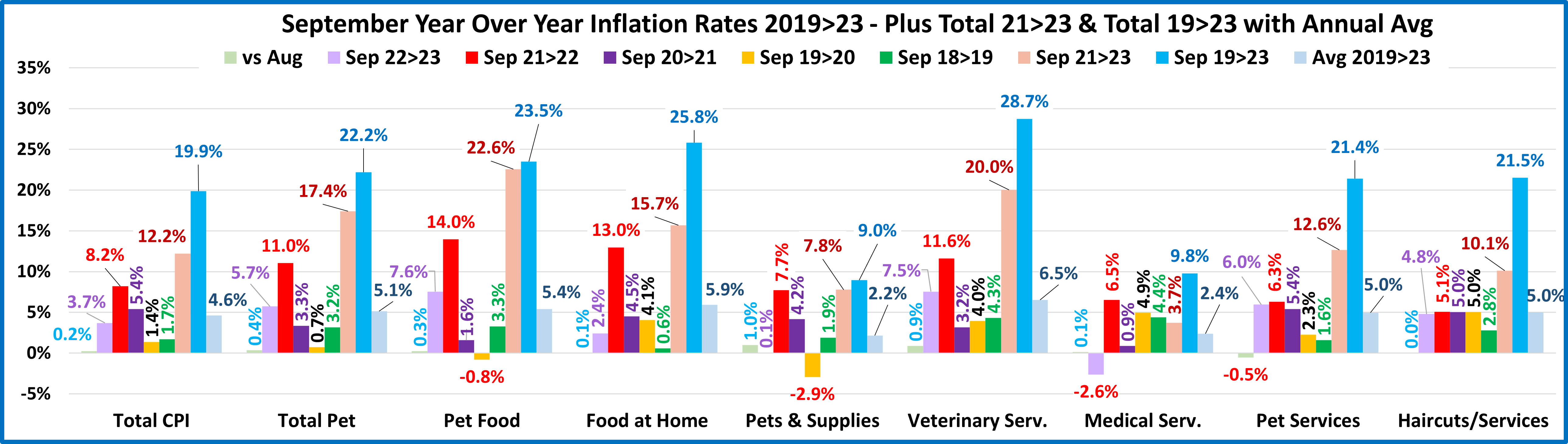

Next, we’ll turn our attention to the Year Over Year inflation rate change for September and compare it to last month, last year and to previous years. We will also show total inflation from 21>23 & 19>23. Petflation fell again to 5.7% in September, but it is still 1.5 times the National rate. The chart will allow you to compare the inflation rates of 22>23 to 21>22 and other years but also see how much of the total inflation since 2019 came from the current pricing surge. Again, we’ve included some human categories to put the pet numbers into perspective.

Overall, Prices were +0.2% vs August and were up 3.7% vs September 22 the same as August. Grocery inflation is down again, to +2.4% from +3.0%. Haircuts prices were unchanged from last month but only 1 of 9 categories had a decrease, compared to 4 in August. Pet Services had the decrease, -0.5%. The national YOY monthly inflation rate for September is unchanged from August but only 45% of the 21>22 rate. The 22>23 inflation rate for all categories is now below 21>22. However, the difference is slight for Non-Vet Services and Haircuts. In our 2021>2023 measurement you also can see that over 65% of the cumulative inflation since 2019 occurred in only 4 segments – Total Pet, Pet Food, Pet Supplies and Veterinary – All Pet. We should also note that the segments with the lowest percentages are Haircuts, Pet Services and Medical Services. Service Segments have generally had higher inflation rates so there was a smaller pricing lift in the recent surge. Services expenditures account for 60% of the National CPI so they are very influential. We also see that Pet Products have a very different patttern. The 21>23 inflation surge provided over 93% of their overall inflation since 2019. This happened because Pet Products prices in 2021 were just starting to recover from a deflationary period.

- U.S. CPI– Prices are +0.2% from August. The YOY increase remained stable at +3.7%. It peaked at +9.1% back in June 2022. The targeted inflation rate is <2% so we are still 85% higher than the target. After 12 straight declines, we had 2 lifts, so stability is an improvement. The current inflation rate is below 21>22 but the 21>23 rate is still 12.2%, 62% of total inflation since 2019. How many households “broke even” by increasing their income by 12% in 2 yrs.

- Pet Food– Prices are +0.3% vs August and +7.6% vs September 2022. They are also 3.2 times the Food at Home inflation rate – not good news! The YOY increase of 7.6% is being measured against a time when prices were 14.4% above the 2019 level, but that increase is still 2.3 times the pre-pandemic 3.3% increase from 2018 to 2019. The 2021>2023 inflation surge has generated 96.2% of the total 23.5% inflation since 2019.

- Food at Home – Prices are up +0.1% from August. The monthly YOY increase is 2.4%, down from 3.0% in August and considerably lower than Jul>Sep 2022 when it exceeded 13%. The 25.8% Inflation for this category since 2019 is 30% more than the national CPI and remains 2nd to Veterinary. 61% of the inflation since 2019 occurred from 2021>2023. The pattern mirrors the national CPI, but we should note that Grocery prices began inflating in 2020>2021 then the rate accelerated. It appears that the pandemic supply chain issues in Food which contributed to higher prices started early and foreshadowed problems in other categories and the overall CPI tsunami.

- Pets & Supplies– Prices were up +1.0% from August but only +0.1% vs September 2022. They still have the lowest increase since 2019. As we noted, prices were deflated for much of 2021. However, even with recent price drops the 2021>2023 inflation surge accounted for 87% of the total price increase since 2019. They reached an all-time high in October 2022 then prices deflated. 3 straight months of increases pushed them to a new record high in February. Prices fell in March, bounced back in Apr>May to a new record high, fell in Jun>Aug, then turned up in September.

- Veterinary Services – Prices are up +0.9% from August. They are +7.5% from 2022 and are still in 2nd place behind Food (+7.6%) in the Pet Industry. However, they are still the leader in the increase since 2019 with 28.7% compared to Food at home at 25.8%. For Veterinary Services, relatively high annual inflation is the norm. The rate did increase during the current surge so 70% of the 4 years’ worth of inflation occurred in the 2 years from 2021>2023.

- Medical Services – Prices turned sharply up at the start of the pandemic but then inflation slowed and fell to a low rate in 20>21. Prices grew 1% from August but are -2.6% vs 2022. Prices have now deflated for 5 straight months. Medical Services are not a big part of the current surge as only 38% of the 2019>23 increase happened from 21>23.

- Pet Services – Inflation slowed in 2020 but began to grow in 2021. September 23 prices were -0.5% from August but +6.0% vs 2022, which is down from 7.2% in last month and much lower than 8.0% in March. Initially their inflation was tied to the current surge, but it may be becoming the norm as only 59% of the total since 2019 occurred from 21>23.

- Haircuts/Other Personal Services – Prices are unchanged from August but +4.8% from 2022, the lowest rate since 2019. Inflation has been rather consistent as just 47% of the inflation from 19>23 happened from 21>23.

- Total Pet– Petflation is now 48% lower than the 21>22 rate, but stll 1.5 times the National CPI. For September, +5.7% is the 3rd highest rate since 1997 (2022: 11.0%; 2008: 9.5%). Vs August, prices grew for all but Services so Total Pet was +0.4%. An Aug>Sep increase has happened in 13 of the last 24 years so it was not a surprise. Food & Veterinary are still the Petflation leaders, but all segments have an influence. Pet Food has been immune to inflation as Pet Parents are used to paying a lot, but inflation can reduce purchase frequency in the other segments.

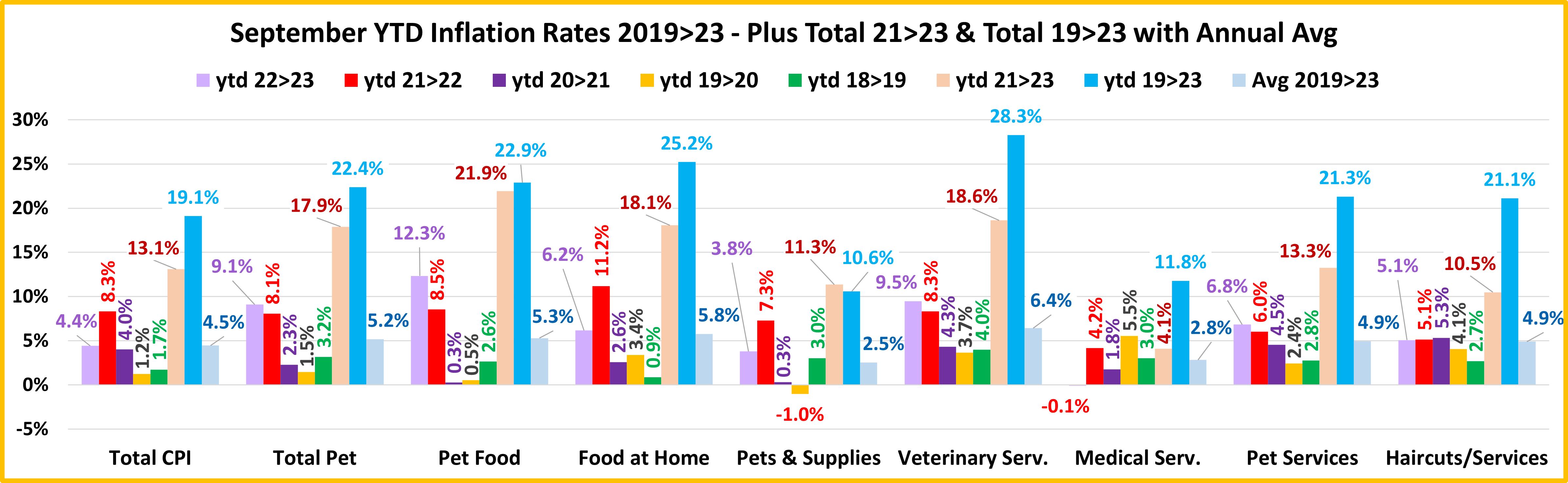

Now, let’s look at the YTD numbers

The increase from 2022 to 2023 is the biggest for 4 of 9 categories – All Pet. The 22>23 rate for Haircuts is equal to 21>22. However, the Total CPI, Pet Supplies, Medical Services and Food at Home are significantly down from 21>22. The average annual increase since 2019 is 4.5% or more for all but Medical Services (2.8%) and Pet Supplies (2.5%).

- U.S. CPI – The current increase is down 47% from 21>22 and 2.2% less than the average increase from 2019>2023, but it’s 91% more than the average annual increase from 2018>2021. 69% of the 19.0% inflation since 2019 occurred from 2021>23. Inflation is a big problem that started recently.

- Pet Food – Strong inflation continues with the highest 22>23 & 21>23 rates on the chart. Deflation in the 1st half of 2021 kept YTD prices low then prices surged in 2022. 95.6% of the inflation since 2019 occurred from 2021>23.

- Food at Home – The 2023 YTD inflation rate has slowed but still beat the U.S. CPI by 41%. You can see the impact of supply chain issues on the Grocery category as 72% of the inflation since 2019 occurred from 2021>23.

- Pets & Pet Supplies – Although prices rose in September, the YTD inflation rate is down to 3.8%. Prices deflated significantly in both 2020 & 2021 which helped to create a very unique situation. Prices are up 10.6% from 2019 but 107% of this increase happened from 2021>23. Prices are up 11.3% from their 2021 “bottom”.

- Veterinary Services – They are still #1 in inflation since 2019 but they have only the 2nd highest rate since 2021. At +6.4%, they have the highest average annual inflation rate since 2019. Except for a sight slowing in 2020, inflation has consistently increased since 2019. Regardless of the situation, strong Inflation is the norm in Veterinary Services.

- Medical Services – Prices went up significantly at the beginning of the pandemic, but inflation slowed in 2021. In 2023 prices have been deflating and are now at -0.1% YTD, the only deflation in any segment.

- Pet Services – May 22 set a record for the biggest year over year monthly increase in history. Prices fell in June but began to grow again in July, reaching record highs in Sep>Apr 23. The January 2023 increase of 8.4% set a new record. YTD September fell a little from 7.0% to 6.8%. Interestingly, although the rates are not as high, they have the exact same annual inflation pattern as Veterinary. The Services segments in the Pet Industry are definitely unique.

- Haircuts & Personal Services – The services segments, essential & non-essential, were hit hardest by the pandemic. After a small decrease in March 22, prices turned up again. Since 2021 inflation has been a consistent 5+%, 90% higher than 18>19. Consumers are paying 21% more than in 2019, which usually reduces the purchase frequency.

- Total Pet – There were two different patterns. After 2019, Prices in the Services segments continued to increase, and the rate grew as we moved into 2021. Pet products – Food and Supplies, took a different path. They deflated in 2020 and didn’t return to 2019 levels until mid-year 2021. Food prices began a slow increase, but Supplies remained stable until near yearend. In 2022, Food and Supplies prices turned sharply up. Food prices grew until Jun>Aug 23. Supplies prices stabilized Apr>May, grew Jun>Oct, fell in Nov, rose in Dec>Feb, fell in Mar, rose in Apr>May then fell in Jun>Aug. Prices in both segments turned up in September. The Services segments have also had ups & downs but have generally inflated. The net is a YTD Petflation rate vs 2022 of 9.1%, 2.1 times the CPI. In May 22 it was 5.8% below the CPI.

Petflation is slowing, but still strong. Petflation dropped from 6.6% in August to 5.7% in September. This is less than half of the record 12.0% set in November, but still the 3rd highest rate for the month. More bad news is that 9 of the last 14 months have been over 10% and the current rate is still 3.6 times the 1.6% average rate from 2010>2021. It’s also 1.5 times the national rate. There is no doubt that the current pricing tsunami is a significant event in the history of the Pet Industry, but will it affect Pet Parents’ spending. In our demographic analysis of the annual Consumer Expenditure Survey which is conducted by the US BLS with help from the Census Bureau we have seen that Pet spending continues to move to higher income groups. However, the impact of inflation varies by segment. Supplies is the most affected as since 2009 many categories have become commoditized which makes them more price sensitive. Super Premium Food has become widespread because the perceived value has grown. Higher prices generally just push people to value shop. Veterinary prices have strongly inflated for years, resulting in a decrease in visit frequency. Spending in the Services segment is the most driven by higher incomes, so inflation is less impactful. This spending behavior of Pet Parents suggests that we should look a little deeper. Inflation is not just a singular event. It is cumulative. Total Pet Prices are up 5.7% from 2022 but they are up 17.4% from 2021 and 22.2% from 2019. That is a huge increase in a very short period. It puts tremendous monetary pressure on Pet Parents to prioritize their expenditures. We know that the needs of their pet children are always a high priority but let’s hope for a little relief – stabilized prices and even deflation. This is not likely in the Service segments, but it has happened before in Products. The Pet Food inflation rate is dropping, and Pet Supplies prices are now only up 0.1% vs September 22. It’s just a start. Let’s hope that it accelerates “down”.

Trackbacks & Pingbacks

[…] Gibbons of PetBusinessProfessor.com, who compiles and analyzes “petflation” data from the U.S. Bureau of Labor Statistics (BLS), […]

Comments are closed.