2021 U.S. Pet Spending by Generation – Gen X Moves to the Top!

In 2021 Americans spent $99.98B on our companion animals, 1.12% of $8.94 Trillion in total expenditures. Pet Spending was up $16.23B (+19.4%), the biggest increase in history. In 2020 Consumers focused on the necessary segments – Food and Veterinary, while the discretionary segments – Supplies and Services, suffered. Out of fear of shortages, Pet Parents binge bought Food early in the pandemic. On the negative side, closures caused Services to have a radical reduction in frequency. In 2021 there was no repeat of the Food binge so $ fell. However, all other segments had record increases.

In this report we will look at the post pandemic surge in Pet Spending for the most popular demographic measurement – by Generation. Although Gen Z $ are often bundled with Millennials for long term comparisons, we will also compare their 2021 spending vs 2020. Using data from the US BLS Consumer Expenditure Survey we’ll compare the Generations.

We’ll start by defining the generations and looking at their share of U.S. Consumer Units (CUs are basically Households)

GENERATIONS DEFINED

Gen Z: Born after 1996

In 2021, Age under 25

Millennials: Born 1981 to 1996

In 2021, Age 25 to 40

Gen X: Born 1965 to 1980

In 2021, Age 41 to 56

Baby Boomers: Born 1946 to 1964

In 2021 Age 57 to 75

Silent/Greatest: Born before 1946

In 2021, Age 75+

- Baby Boomers still have the largest number of CU’s at 43.6M and 32.7% of the total. They had a slight increase in 2021 but generally they have been losing ground. In fact, they have 1.5M fewer CU’s than in 2016.

- The Oldest Generations will continue to lose CUs primarily due to death or movement to permanent care facilities.

- Gen X has the second most CUs but lost a little ground in 2021.

- Millennials have the largest number of individuals, but they rank only third in the number of CU’s.

- Both Gen Z & Millennials gained CUs. The pandemic recovery saw many younger folks leave their parents’ homes.

Now let’s look at some key CU Characteristics

Significant changes were the decrease in homeownership and CU size. This was primarily driven by the oldest group. Gen Xers still have the biggest CUs and the most Earners while Millennials have the most children <18 per CU.

- CU Size – is down from 2.5 due to a decrease by the Silent/Greatest generations. CUs with 2+ people still account for 69.5% of all U.S. CUs (down from 70.2% in 2020) and 80.6% of pet $ (up from 80.3% primarily due to a huge lift by 2 person CUs). Millennials are actively building their H/Hs. However, CU size, with all the related responsibilities, still peaks with the Gen Xers and then starts dropping. The Boomers are the last group with 2+ CUs but that will end soon. Gen Z joined the 2+ group for the 1st time in 2020 and moved to 2.1 in 2021.

- # Children <18 – 27.1% of U.S. CU’s have children, down from 27.6% and they generate 31.9% of Pet Spending, down from 38.4%. The slight drop in CUs came from families with an oldest child under 6 or over 18. The drop in Total Pet Spending came solely from an $8B decrease by families with an oldest child over 18. All other CUs, with or without children spent more. The net result was CUs without children spent $16.53B more while those with children spent -$0.3B less. Overall, there was no change in the # of children per CU in 2021 but there was 1 change within groups. Gen X CUs fell from 0.9 to 0.8 in the average number of children <18. We noted the $8B drop in spending with an oldest child over 18. This group is often Baby Boomers.

- # Earners – Pet spending is often tied to the number of earners in a CU. In 2021, all Earner & No Earner CUs spent more on their pets. 2+ earner CUs still spent the most, but No Earner CUs had the biggest increase, +$6.3B (+60.5%). No Earners are usually older and retired. This includes the oldest Boomers but also the Silent/Greatest generations.

- Homeownership – Owning and controlling your own space has always been a major factor in increased Pet Ownership and spending. In 2021 homeownership decreased to 64.72% from 65.81%. Gen Z & Millennials had increases but Gen X and the oldest group had decreases. The homeowners share of Total Pet Spending fell from 83.3% to 80.0% due to a -$3.7B drop from those without a mortgage. This is the group that binge bought food in 2020. Homeowners with mortgages and Renters spent $19.9B more on their pets. We should also note that the number of homeowners w/no Mtge was unchanged overall and for Boomers & Gen X. It grew slightly for Gen Z & Millennials but this was offset by a decrease from the Silent/Greatest generations.

- As expected, Gen Z are the most common renters in society. Homeownership by Millennials has moved up to 49% but it is still only 75% of the national average.

- Gen Xers have been above the national avg since 2018 and Homeownership continues to increase with age.

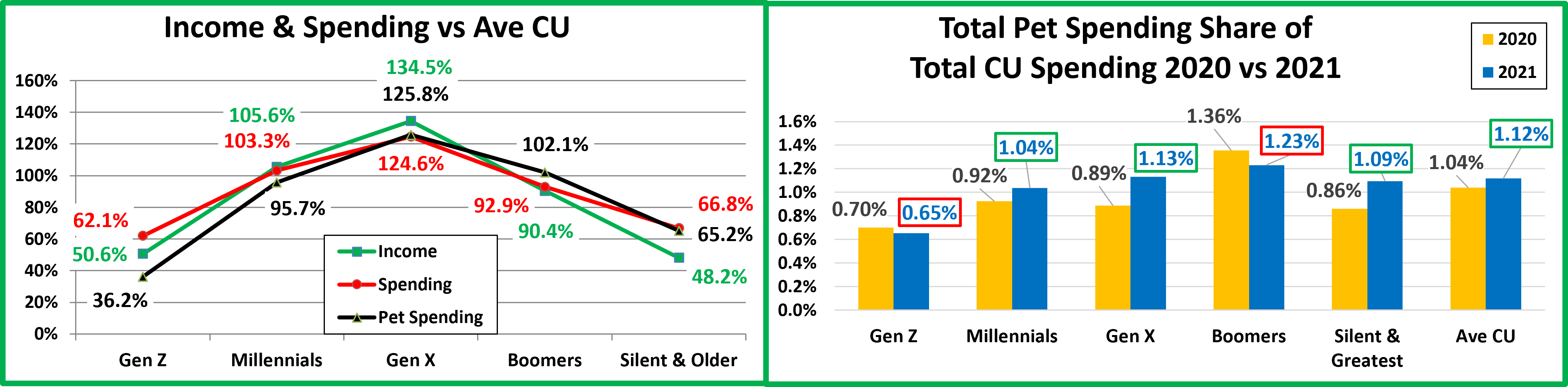

Next, we’ll compare the Generations to the National Avg.:

In Income, Total CU Spending, Total Pet Spending and the Pet Share of Total CU Spending

CU National Avg: Income – $87,432; Total CU Spending – $66,906; Total Pet Spending – $748.93; Pet Share – 1.12%

- Income – The Gen Xers are still at the top but their lead fell slightly. The incomes of Boomers and Silent/Greatest continued to fall. Millennials’ income beat the national average in 2020 and continues to grow. The income of Gen Z passed that of the oldest Americans so they are no longer in last place.

- Total Spending – The Gen Xers make the most and spend the most but it’s not out of line with their income. Millennials increased their spending so that it now beats the national average. Like their income, Boomers’ spending fell even further below the national average. Due to a big lift in spending in relation to income, the oldest group is once again deficit spending in relation to their after tax income. With continued strong increases in both Income and spending, the retail importance of Millennials is growing.

- Pet Spending – Again only 2 groups exceed the national average, but Gen X returned to the top spot. Millennials are still 3rd, 24% below Gen X but only 6% below Boomers. The oldest and youngest groups still trail.

- Pet Spending Share of Total Spending – The national number grew from 1.04% to 1.12%. The growth was driven by increases from all groups but Gen Z and Boomers. In 2020 Boomers were the only group to spend more than 1% of their total expenditures on their pets. In 2021 Boomers are still the leaders but only Gen Z spent less than 1% of their total expenditures on their pets – perhaps the surest sign of the growing importance of the Pet industry.

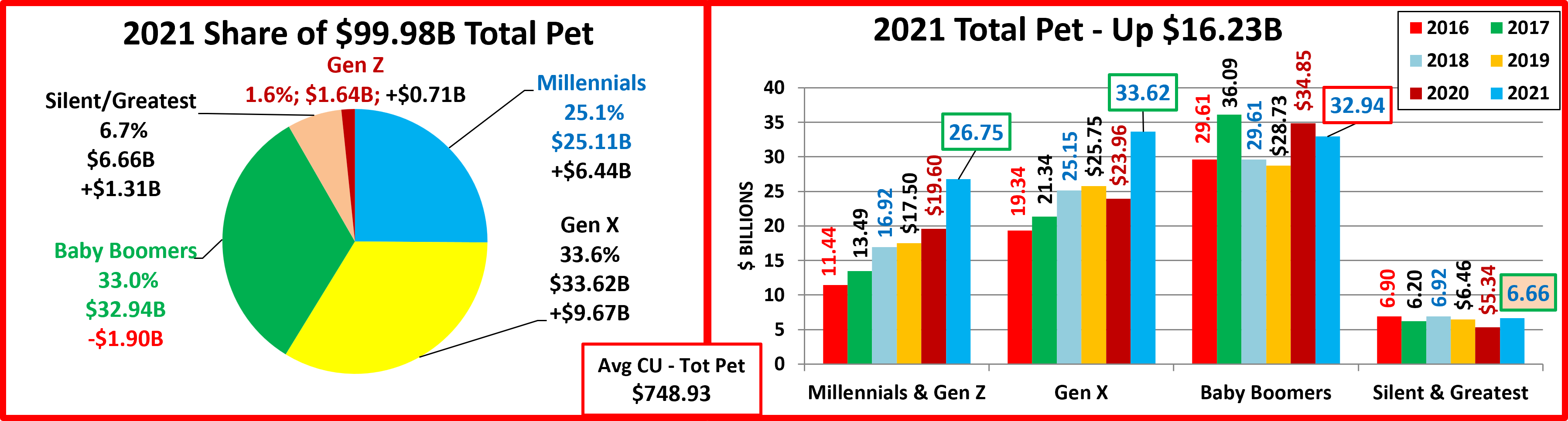

Now, let’s look at Total Pet Spending by Generation in terms of market share as well as the actual annual $ spent for 2016 through 2021. The 2021 numbers are boxed in red (decrease) or green (increase) to note the change from 2020.

- Boomers are no longer the biggest force in Pet Spending. Gen X took over the top spot in 2021…barely.

- The pandemic both continued and broke some long-term spending patterns. Spending in the oldest group is low and had been slowly falling. It surged in 2022. In contrast, the youngest group (combined Millennials & Gen Z) is the only one showing consistent year after year growth. Gen X had also been growing every year… until 2020. They did have the biggest “recovery” in 2021. The Boomers have been on a rollercoaster ride because they are the most likely group to have a strong reaction to trends, especially in this era of super premium foods. They also have the money to act on their feelings. In 2020 this was very apparent as they were the primary group that panic bought Pet Food out of fear of possible shortages due to the pandemic. In 2021 they couldn’t quite equal their 2020 $.

- In 2021, only Boomers spent less. Silent/Greatest: +$1.31B. Boomers: -1.90B. Gen X: +9.67B. Millennials: +$6.44B. Gen Z: +$0.71B.

- Boomers – Ave CU spent $764.68 (-36.10); 2021 Total Pet spending = $32.94B, Down $1.90B (-5.5%)

- 2016>2021: Up $3.33B; They stayed on the roller coaster as spending turned down but is still +10.2% vs 2016.

- Gen X – Ave CU spent $941.87 (+276.65); 2021 Total Pet Spending = $33.62B, Up $9.67B (+40.3%)

- 2016>2021: Up $14.28B Their annual Pet spending growth since 2015 had been strong and consistent until a drop in 2020. In 2021 they became #1 in CU Pet spending and Total $. Their spending is up 74% from 2016.

- Millennials + Gen Z – Ave CU spent $650.97 (+$117.16); 2021 Total Pet Spending = $26.75B, Up $7.15B (+36.5%)

- 2016>2021: Up $15.31B; As the income and overall spending of Millennials grows, their pet spending has also grown every year. The “youngsters” have the biggest increase in $ since 2016 of any group, $15.31B, +134%.

- Millennials Only– Ave CU spent $716.51 (+$151.44); 2021 Total Pet Spending= $25.11B, Up $6.44B (+34.5%)

- Gen Z Only – Ave CU spent $271.27 (+$16.59); 2021 Total Pet Spending= $1.64B, Up $0.71 (+76.9%)

- Silent + Greatest – Ave CU spent $488.50 (+$134.30); 2021 Total Pet Spending = $6.66B, Up $1.31B (+24.6%)

- 2016>2021: Down $0.24B; They also had a huge lift in CU pet spending but CU count fell 12.3%, -30% from 2016.

Gen X took over the top spot in Total Pet Spending, but Millennials’ performance was also strong. Only Boomers spent less in 2021, but their CU spending still exceeds the national average. The pet spending “torch” is slowly being passed.

Let’s look at the individual segments. First, Pet Food…

- Pet Food trends are more pronounced for Boomers, and they had the only decrease. Pet parenting is fading In the older generations, but they finally moved to Super Premium. The younger groups have had more consistent growth.

- Since 2014, Millennials’ have led the way in food trends, and they are the only group with an annual increase every year since 2016. The panic food buying in 2020 by Boomers was more of an emotional reaction than a trend.

- Boomers – Ave CU spent $280.45 (-161.61); 2021 Pet Food spending = $11.82, Down $7.49B (-38.8%)

- 2016>2021: Down $0.1B Big reactions to every trend. They spent less than 2020 and even less than in 2016.

- Gen X – Ave CU spent $306.27 (+$75.91); 2021 Pet Food spending = $11.12B, Up $2.82B (+34.0%)

- 2016>2021: Up $4.26B They reacted to the FDA warning by further upgrading their food. No pandemic panic buying for them. They value shopped. In 2021 they surged to the top in CU Pet Food Spending.

- Millennials + Gen Z – Ave CU spent $191.28 (+$0.26); 2021 Pet Food Spending = $7.86B, Up $0.79B (+11.2%)

- 2016>2021: Up $3.05B They are the only group with increased spending every year since 2016. Their income is growing as is a commitment to their pets. They often pioneer food upgrades and the pandemic had little impact.

- Millennials Only – Ave CU spent $206.12 (-$0.82); 2021 Pet Food spending = $7.23B, Up $0.37B (+5.4%)

- Gen Z Only – Ave CU spent $104.44 (+$51.47); 2021 Pet Food spending = $0.63B, Up $0.42B (+209.0%)

- Silent/Greatest – Ave CU spent $262.00 (+$114.43); 2021 Pet Food spending = $3.61B, Up $1.44B (+66.1%)

- 2016>2021: Up $0.57B; Their CU #s are fading but they are committed to pets as they upgraded food in 2021.

Pet Food Spending is driven by trends – new Super Premium Foods, FDA warnings and even fear of pandemic shortages. Millennials lead in thoughtful changes and Boomers lead in emotion but Gen X leads in CU $. Now, Supplies Spending.

- All groups spent more but Gen X increased their lead at the top with a 71% spending increase.. The younger groups dominate this segment as Gen Xers and Millennials/Gen Z together account for 68% of Supplies spending.

- Gen X – Ave CU spent $265.43 (+$112.96); 2021 Pet Supplies spending = $9.40B, Up $3.91B (+71.2%)

- 2016>2021: Up $4.15B; Gen Xers are again the leader in CU spending. They were affected by tarifflation in 2019, but essentially held their ground in 2020. In 2021 spending exploded as they made up for 2019 & 2020.

- Baby Boomers – Ave CU spent $154.03 (+$52.18); 2021 Pet Supplies spending = $6.72B, Up $2.31B (+52.3%)

- 2016>2021: Up $0.35B In 2019 tarifflation hit. In 2020 they focused on Food! In 2021 they made it back to 2018 $

- Millennials + Gen Z – Ave CU spent $165.99 (+$42.23); 2021 Pet Supplies spending = $6.82B, Up $2.30B (+50.8%)

- 2016>2021: Up $4.01B; Millennials earn their share in Supplies spending. They were the least impacted by the tariffs in 2019 and spent more in 2020. Their spending then took off in 2021, with a 53% increase.

- Millennials Only– Ave CU spent $180.37 (+$55.32) 2021 Pet Supplies spending= $6.32B, Up $2.20B (+53.3%)

- Gen Z Only – Ave CU spent $82.95 (-$28.97); 2021 Pet Supplies spending = $0.50B, Up $0.10B (+25.4%)

- Silent + Greatest – Ave CU spent $64.27 (+$16.52); 2021 Pet Supplies spending = $0.87B, Up $0.13B (+18.0%)

- 2016>2021: Down $0.63B; This $ conscious group was hit hard by tariffs and the pandemic, but had a small lift.

In 2016 most Consumers value shopped for super premium food and spent some of their savings on Supplies. Supply prices dropped in 2017 and everyone under 72 spent more! Late 2018 saw added tariffs but only Boomers dialed back spending. In 2019 the sharply rising prices drove spending down in all groups. In 2020 Millennials and Gen X spent a little more while the older groups spent a lot less. In 2021 spending took off in all groups as they made up for recent years.

Next, we’ll turn our attention to the Service Segments. First, Non-Veterinary Pet Services

- Gen Z & the oldest group spent less. Gen X is still #1 in CU spending and $. Gen X/Millennial/Gen Z share = 62.5%

- Gen X – Ave CU spent $91.64 (+$21.66); 2021 Pet Services spending = $3.25B, Up $0.72B (+28.7%)

- 2016>2021: Up $1.52B; In 2020 they had the 2nd biggest drop. In 2021 they had the 2nd biggest lift but are still #1.

- Baby Boomers – Ave CU spent $70.06 (+$19.46); 2021 Pet Services spending = $3.06B, Up $0.86B (+39.5%)

- 2016>2021: Down $0.15B; The biggest $ drop in 2020 and the biggest lift in 2021, but they’re still behind 2016 $.

- Millennials + Gen Z – Ave CU spent $59.51 (+$11.43); 2021 Pet Services spending = $2.45B, Up $0.69B (+39.1%)

- 2016>2021: Up $1.32B; In 2020 they had the smallest decrease of any group and with the 2021 lift they have more than doubled their 2016 spending. Despite a 31% increase in CUs Gen Z’s Services spending fell.

- Millennials Only– Ave CU spent $66.61 (+$17.09); 2021 Pet Services spending = $2.33B, Up $0.70 (+42.9%)

- Gen Z – Ave CU spent $18.53 (-$16.39); 2021 Pet Services spending = $0.11B, Down $0.01B (-10.2%)

- Silent + Greatest – Ave CU spent $26.29 (-$1.29); 2021 Pet Services spending = $0.35B, Down $0.07B (-16.4%)

- 2016>2021: Down $0.42B; They definitely have the need but spending continues to fall, down 55% from 2016.

This segment had slow annual growth until 2017 which saw a small drop in spending due to an extremely competitive environment. In 2018, the increased number of outlets really hit home and spending exploded. 2019 brought another small decrease as Gen Xers & Millennials looked for and found a better deal. 2020 brought pandemic restrictions and closures. 2021 produced a record lift due to a 9.2% increase in spending and an 18.8% increase in frequency.

Now, Veterinary Services

- Boomers are still the biggest spenders in this segment, but they only lead Gen Xers in $ because of more CUs.

- The younger groups have a consistently growing commitment to this Pet Parenting responsibility. The combined Veterinary spending of Millennials/Gen Z and Gen Xers has increased $11.29B (+138%) since 2016.

- Boomers – Ave CU spent $260.14 (+$53.87); 2021 Veterinary spending= $11.35B, Up $2.41B (+27.0%)

- 2016>2021: Up $3.24B; In 2020, Boomers focused on needed segments – Food & Veterinary. In 2021 they changed their focus to Supplies, Services and Veterinary, including a Veterinary spending increase of $2.4B.

- Gen X – Ave CU spent $278.53 (+$66.12); 2021 Veterinary spending= $9.86B, Up $2.21B (+28.9%)

- 2016>2021: Up $4.37B; In 2016 their Veterinary spending exceeded the national CU Average. In 2018, they took over the top spot in CU spending and increased their lead in 2021. This produced a $2.2B lift in Veterinary $.

- Millennials + Gen Z– Ave CU spent $234.18 (+$63.24); 2021 Veterinary Spending $9.62B, Up $3.38B (+54.0%)

- 2016>2021: Up $6.92B; They had the biggest lift and spending is up 256% from 2016. Veterinary is a big priority.

- Millennials Only – Ave CU spent $263.41 (+$79.85); 2021 Veterinary spending = $9.23B, Up $3.18B (+52.5%)

- Gen Z Only – Ave CU spent $65.35 (+$10.48); 2021 Veterinary spending = $0.40B, Up $0.20B (+101.5%)

- Silent + Greatest – Ave CU spent $135.94 (+$4.64); 2021 Veterinary spending $1.83B, Down $0.19B (-9.2%)

- 2016>2021: Up $0.02B; Their pets’ health is still a priority. Spending fell due to a 12.3% decrease in CUs.

Gen Xers and Millennials have consistently increased their commitment to Veterinary Services. Back in 2015, their share of Veterinary Spending was 36%. It is now 60%. This indicates a big, fundamental change in spending behavior.

One last chart to compare the share of spending to the share of total CU’s to see who is “earning their share”.

- Gen X Performance – Total: 126.9%; Food: 121.9%; Supplies: 149.0%; Services: 134.5%; Veterinary: 113.9%

- Gen Xers returned to the top spot in performance. This year they earned their share in Total Pet and all industry segments. Except for the 2020 dip they increased their Total Pet Spending every year since 2016. In 2021 they made up for the dip with a big increase in every segment. Their spending has become more balanced and they are now the performance leader in every segment. Gen Xers range in age from 41 to 56 so they are just entering the peak earning years. Expect their commitment and pet spending to continue to grow.

- Baby Boomers Performance – Total: 100.9%; Food: 105.2%; Supplies: 86.4%; Services: 102.8%; Veterinary: 106.4%

- Boomers led the way in building the industry but are no longer the “top dogs” in $. They earn their share in all but Supplies and are still the spending leader in the “needed” segments – Food & Veterinary. They are also the most emotional Pet Parents, so their spending is subject to radical swings like 2020’s panic, binge buying of Pet Food. They should still be a major force in the Pet Industry for many more years, but the Gen Xers have now stepped up and the Millennials are also preparing to eventually take their turn at the top.

- Millennials Performance – Total: 95.8%; Food: 80.2%; Supplies: 101.2%; Services: 97.8%; Veterinary: 107.7%

- Millennials are now the only group to have increased their pet spending every year since 2016. Their spending is more evenly balanced, and performance has improved but their future as the Pet Parenting spending leaders is still a long way off. Their income, home ownership and pet spending are all increasing. They are educated and well connected. Indications are that they may lead the way in adopting new trends, especially in food. Their progress is good news, but in reality, their leadership is probably at least a decade away.

- Silent/Greatest Performance – Total: 66.1%; Food: 104.1%; Supplies: 36.1%; Services: 38.6%; Veterinary: 55.6%

- Pet Parenting is more challenging in old age, but they remain committed. 1.09% of their total spending is on pets.

- Gen Z Performance – Total: 36.1%; Food: 40.1; Supplies: 46.6%; Services: 27.2%; Veterinary: 26.7%

- They are just beginning so the numbers are low. Their performance actually fell due to a 31% increase in CUs.

Baby Boomers are still the heart of the industry, but Gen Xers are now the $ leaders. Expect Gen X’ growth to continue as they are pursued by Millennials. Both groups seem ready, willing and able to take their turn at the top. Pet Spending has become more balanced across the generations. This bodes well for the continued strong growth of the industry.