PET STORES – CHAINS vs INDIES

In our 30 year history of Pet Stores, we tracked their rise to the top spot in pet products sales, which was largely due to the creation and rapid growth of chains and Pet SuperStores. They gained the #1 position in 1997 and have held it ever since. However, that journey has not been without challenges. They maintained a 40% market share in Pet Products in 1997 and 2002 but that fell to 33.1% in 2012 due to increased competition from the mass market. From 2012 to 2017, there was a new challenger – the Internet, but Pet Stores remained strong. They increased their share of Pet Products sales slightly to 33.3%. This was a small, but very significant gain as Pet Stores and $ Stores were the only 2 retail channels to gain market share in Pet Products $ in this 1st Internet Tsunami.

There is no doubt that that Pet Stores are resilient and a key consumer channel for Pet Parents. However, not all pet stores are the same. There is the key difference of Indies vs Chains. However, not all chains are created equal. They range from small local chains to regional to the national behemoths. In this report we will look at how these groups have progressed from 2002 to 2017, with an especially deep look at who stood their ground from 2012 to 2017 and how they did it.

We’ll start with the share of stores and Total $ for 2017 for independents and various sizes of chains. Remember, there were 9984 pet stores (with employees) in 2017, an increase of 1192 (+13.6%) from 2012. $ales showed even stronger growth, up $3.6B (+24.7%) to $18.4B in 2017.

Pet Store Numbers – Indies lost a little ground while the big chains are growing at a staggering rate. The small local chains (2>9 Stores) are also growing, especially the 5>9 group. The 10>24 group lost share, but they are basically in a transitional step on their way to 25+ stores. Chain Stores have more than half of all pet outlets with employees, 51.5%.

Pet Store $ales – The big chains dominate Pet Store $, 71.5%. However, $ales in the Indies and small local chains are still growing. $ales in the small chains are actually growing at a significantly higher rate than the big guys.

This shows where the pet store channel is at. Let’s see how it got there with data from 2002 to 2017. First # of Stores

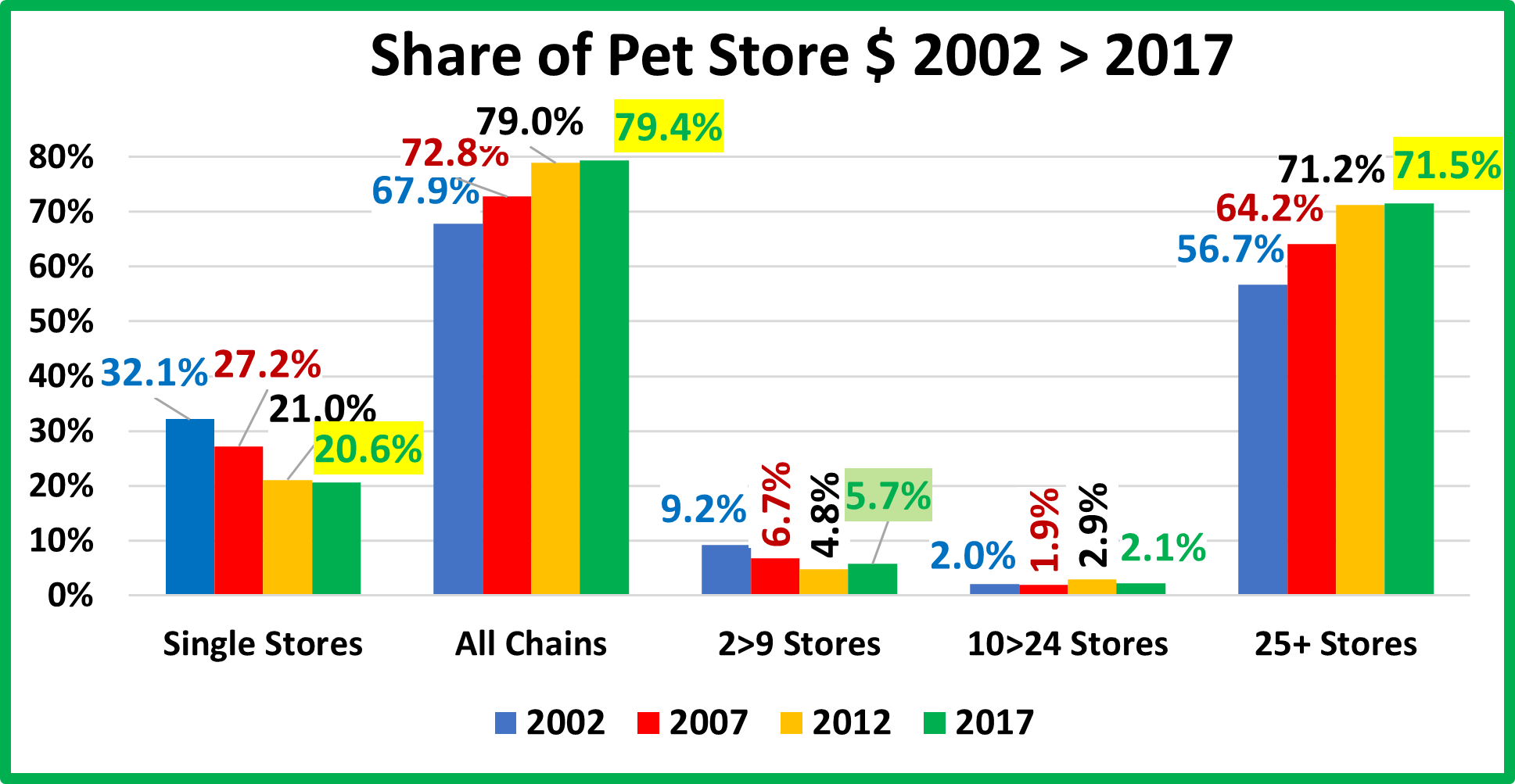

Share of Pet Stores

- The number of Pet Stores grew from 7626 in 2002 to 9984 in 2017, an increase of 2358 (+30.9%).

- The number of Indies has slowly but steadily declined from 5285 in 2002 to 4839 in 2017, -446 (-8.4%)

- During the same period, chain store outlets have more than doubled, from 2341 in 2002 to 5145 in 2017, +2804 (+119.8%).

- That makes 2017 a very significant year. Independent Pet Stores were a key part of the foundation of the Pet Industry. For the 1st time they were outnumbered by chain stores.

- The big chains, 25+ stores, have been the driving force in the growth in the number of Pet Stores in the 21st century. They went from 1512 stores in 2002 to 4287 in 2017, +2775 (+183.5%) – almost triple.

- The 10>24 Store chains are a transitional phase, so their market share has been up and down. They are often focused on growing numbers for a stronger regional or even national presence so many move up to the 25+ group.

- The 2>9 group is a combination of the 2>4 and 5>9 store groups and was created because their growth pattern is very similar. As you can see, their share of stores fell consistently from 2002 to 2012. Their store count fell from 646 to 554, -14.2% during this period. Then they turned it around. They added 16 more companies and 72 stores (+13.0%) between 2012 and 2017. They didn’t gain share but held their ground vs the big guys.

Now let’s look how the share of Pet Store $ have “evolved” over the same period.

Share of Pet Store $

- Pet Store $ales grew from $7.6B in 2002 to $18.4B in 2017, a $10.8B (+142.1%) increase.

- Independent Store $ increased from $2.4B to $3.8B, +$1.4B (+58.3%) during those years. That’s a 3.1% annual increase but it wasn’t nearly enough as they lost significant share through 2012. 2012>2017 was a different story. Their sales increased +22.1%. They lost 0.4% in share but essentially “held their ground”.

- Chain stores have dominated the $ in this channel since 1997. Between 2002 and 2017 their total sales grew from $5.2B to $14.6B (+180.8%). As Indies lost share, they gained. From 2012 to 2017, their sales increased +$2.9B (+25.4%). However, like the Indies, their share essentially plateaued.

- Like store count, the big chains have driven the growth in Pet Store $. Their sales grew $4.3B, +104.7% between 2002 and 2017. However, their growth from 2012 to 2017 was 25.1%, slightly below the rate of total chain $.

- The transitional 10>24 Store chains had an up and down pattern that exactly mirrored their pattern in store count. They had a 2.1% increase in $ from 2012 to 2017 which resulted in a 27.6% drop in share, from 2.9% to 2.1%.

- The 2>9 Store local chain group earned the only green highlight on the chart. From 2002 to 2012 their $ grew +2.7% but Their share of $ was nearly cut in half. The 2012>2017 period had a radically different story. Their $ales grew +$0.34B (+47.1%), by far the biggest percentage increase of any group. At $1.05B, they broke the “billion $ barrier” for the first time. Their share of $ grew 0.9% to 5.7%, an 18.8% increase.

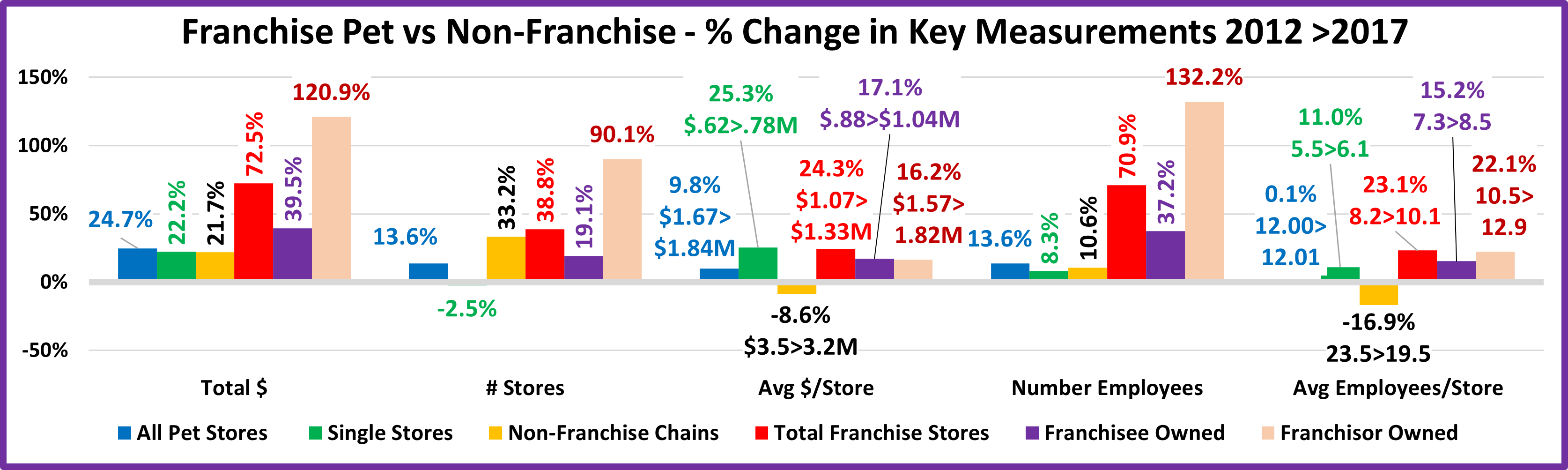

This last chart on share of $ told a similar story to the store count chart up until 2012. Then some patterns changed. This suggests that we should take a closer look at what happened between 2012 and 2017. In this next chart we look at the % change in some key measurements from 2012 to 2017 for the different groups of Pet Stores.

Before we get to the specifics for each group, we’ll comment about how each measurement relates to our “deep dive”.

- Total $ – The gap between share of $ for Chains and Independents had been growing through 2012. Then the growth flattened out in 2017. This change in pattern indicated that we should look a little deeper. There are 2 primary drivers behind a change in $ – Number of Stores and Average Sales per store.

- # of Stores – This is often the main reason behind a change in $. If your business model remains unchanged, then your $ are connected to your store count – up or down.

- Avg $/Store – This can reflect product trends in the industry and is also a measure of your consumer appeal. The movement to Super Premium Pet Foods began in 2014/15 and had a differing impact upon the groups.

- # of Employees – If you don’t change your in store business model, this should be directly tied to store count.

- Avg # Employees/Store – Employees have a variety of functions, including stocking shelves, building displays and keeping the store “cleaned and polished”. However, the most important responsibility may be interacting with customers. Pet Parents want interaction and discussion when they are shopping for products for their Pet “Children”. This has been a key reason that Pet Stores have maintained the top $ position over other channels.

Now, let’s see how the various Pet Store groups performed in these areas between 2012 and 2017.

- All Pet Stores – This will be a key group for comparison as it reflects the progress of the entire Pet Store Channel.

- Total $: $18.4B, +24.7%

- # Stores: 9984, +13.6%

- Avg $/Str: $1.84M, +9.8%

- # Employees: 119.9K, +13.6%

- # Employ/Str: 12.01, +0.01%

The growth in Total $ came from both increased store count and $ per store but more stores was the biggest driver. In terms of employees, the overall model was unchanged as employees/store went from 12.0 to 12.01.

- Single Stores – They don’t have the most number of stores for the 1st time in history.

- Total $: $3.8B, +22.2%

- # Stores: 4839, -2.5%

- Avg $/Str: $0.78M, +25.3%

- # Employees: 29.3K, +8.3%

- # Employ/Str: 6.1, +11.0%

They lost some stores but radically increased the $ per store. Specialty Super Premium foods and increased consumer connection from more employees per store were factors in holding their ground in share of $.

- All Chains – Now, the biggest group in both $ and Stores. We’ll look for similarities and differences within the group.

- Total $: $14.6B, +25.3%

- # Stores: 5145, +34.3%

- Avg $/Str: $2.83M, -6.7%

- # Employees: 90.6K, +15.5%

- # Employ/Str: 17.6, -14.0%

Overall, their $ growth slightly exceeded the channels growth rate, but it was entirely driven by more stores as the average store sales fell. They also added a lot of employees but the employees per store fell significantly. One factor is that some chains began adding smaller format stores to save money and have a more personal experience.

- 2>4 Store Chains – We added this group back in to look for differences between them and the 5>9 Store group.

- Total $: $0.55B, +37.3%

- # Stores: 362, +7.4%

- Avg $/Str: $1.53M, +27.8%

- # Employees: 4.4K, +26.3

- # Employ/Str: 12.2, +17.6%

This group represents a critical time for Pet Store owners. They have a successful store. Could they do even better if they added another location or 2. In 2017, more companies opted in, but others continued to grow and moved up to the 5>9 group. They grew 7.4% in stores but increased the number of employees per store by twice that amount, +17.6%. This is important any time, but it was extremely important in the movement to Super Premium food. They offered the product but also had the personnel to discuss the consumers’ wants and needs. This helped drive their per store sales up 27.8%, to a level double that of Single Stores and produced a 37.3% increase in Total $.

- 5>9 Store Chains – This group, with more stores and better coverage can become a major force in local markets.

- Total $: $0.50B, +59.9%

- # Stores: 264, +21.7%

- Avg $/Str: $1.89M, +31.4%

- # Employees: 3.1K, +34.7%

- # Employ/Str: 11.7, +10.8%

This group had a game plan similar to the 2>4 group but with even stronger results. They added even more stores. This, in combination with increased store sales drove Total $ up 60%. They have the stores and people to be strong competition to the big chains in their local market.

- 10>24 Store Chains – Most are committed to further growth so there is a continual influx and outflow of companies.

- Total $: $0.39B, -7.2%

- # Stores: 232, -15.0%

- Avg $/Str: $1.69M, +9.2%

- # Employees: 2.3K, -0.4%

- # Employ/Str: 9.7, +17.2%

This is a transitional group, on their way up. They added employees per store and increased Store sales. Their Total $ fell solely because of a 15% drop in the number of stores.

- 25+ Store Chains – This group is the dominant force in the Pet Store Channel and has been since the 90’s.

- Total $: $13.1B, +25.1%

- # Stores: 4287, +42.7%

- Avg $/Str: $3.06M, -12.3%

- # Employees: 80.8K, +14.8%

- # Employ/Str: 18.8, -19.5%

With 42.9% of the stores and 71.5% of the $, there is no doubt this is the dominant group in the Pet Store channel. Their $2.6B (+25.1%) increase was also 72.6% of the Total $ increase for Pet Stores. They are the group that allowed Pet Stores to maintain and gain in market share of pet products against the Mass Market and an Internet Tsunami. With that being said, the group continues to evolve with many new smaller footprint stores designed to give Pet Parents an even more personal retail experience. This contributed to fewer employees per store and reduced Store volume. One thing hasn’t changed. They continue to open stores at a spectacular pace.

Observations

The movement to personalize our pets really came to the forefront of Pet $ with the strong movement to Super Premium Foods which began in the 2nd half of 2014 with Millennials and then spread to Boomers and ultimately became widespread across the consumer marketplace. The big chains remain the bulwark of the Pet Store channel. However, they provided a wall of protection which allowed small, localized chains to grow and prosper. They offer a more personal shopping experience and often were the first to stock and sell some new Super Premium pet foods. You see the results of this broadened appeal in the increase in per store sales for all pet stores with fewer than 25 outlets, including Indies. The biggest % growth in store $ occurred in the 2>4 and 5>9 groups. The 5>9 store group became especially stronger with a 60% increase in Total $. The reason is twofold. They offer a personalized experience but have enough outlets in any given local market to be a convenient option for consumers. We also shouldn’t forget the progress of the 2>4 Store group. I did a year long investigation of Pet Stores 3 years ago to validate the numbers. I found that a large number of new independents entered the market, but over the course of the year, over 8% of existing indies “closed their doors”.

The chain stores, big and small, lost virtually no outlets. There is a lesson here, that is almost as old as humanity but also applies to retail pet stores. “There is safety in numbers!” It just takes 2 or maybe 5 or you could move up to 15. After that the sky is the limit! Chain stores began in the 90’s. The big guys will remain dominant but there is room for all sizes!

There is another classification of Pet Stores that has come more to the forefront….

Pet Store Franchises

Let’s take a closer look. These stores are either owned by the Franchisee or the Franchisor.

In 2017 their share of stores was:

- All Franchise Stores: 10.6%

- Franchisee owned: 6%

- Franchisor Owned: 4.0%

And their share of $ was:

- All Franchise Stores: 7.7%

- Franchisee Owned: 3.7%

- Franchisor Owned: 4.0%

About 1 in every 9 Pet Stores is a Franchise outlet but they take in only 1 of every 13 dollars spent at U.S. Pet Stores. Franchisee Owned lead the way in number of stores, but Franchisor Owned stores produce more $.

This is where they were at in 2017. Let’s take a look at how they got there by viewing the changes in key measurements from 2012 to 2017.

These are the same key measurements, just for groups most relevant to franchises, including their biggest competitor.

- Non-Franchise Chains – This is their biggest competitor and accounts for 40.9% of stores and 71.6% of Pet Store $.

- Total $: $13.15B, +21.7%

- # Stores: 4082, +33.2%

- Avg $: $3.22M, -8.6%

- # Employees: 79.8K, +10.6%

- # Employ/Str: 19.5, -16.9%

Being on top creates a lot of pressure. They had a huge $ increase from opening more stores. Their percentage increase in $ was actually, even smaller than Indies, who closed 2.5% of their stores. They were the only group to have drops in Average Store $ and the number of employees per store.

- Total Franchise Stores – They gained ground in share of stores and $ but 1 subgroup was a bigger driver.

- Total $: $1.42B, +72.5%

- # Stores: 1063, +38.8%

- Avg $: $1.33M, +24.3%

- # Employees: 10.8K, +70.9%

- # Employ/Str: 10.1, +23.1%

Their growth rate in stores and Total $ was basically triple that of the whole Pet Store channel. The growth rate for Average Store $ was slightly behind the rate for Indies but it was 70% higher in actual $. They also led the way in employee increases and broke the 10 employee per store “barrier”.

- Franchisee Owned Stores – Same name and business model, but different levels of execution from corporate stores.

- Total $: $0.68B, +39.5%

- # Stores: 660, +19.1%

- Avg $: $1.04M, +17.1%

- # Employees: 5.6K, +37.2%

- # Employ/Str: 8.5, +15.2%

Although they lost some share to Franchisor Owned stores, they are still 62.1% of all Franchise Stores. They had significant growth in all measurements, but the store level execution of the Franchise business model can vary between stores producing a lower growth rate. In many ways the business behavior of these stores is more like that of an enhanced Independent Store. They have the 2nd lowest Store $ and number of employees per store. Both these measurements are 30+ higher than Indies and 30+% lower than Franchisor Owned stores. The growth in stores is promoted and driven by the Corporation and the increase in store $ over an independent store likely comes from the impact of the store Brand name and the Franchise business model.

- Franchisor Owned Stores – These stores are classified as Franchises but essentially operate like a regular chain.

- Total $: $0.73B, +120.9%

- # Stores: 403, +90.1%

- Avg $: $1.82M, +16.2%

- # Employees: 5.2K, +132.2%

- # Employ/Str: 12.9, +22.1%

Like the big regular chains, this group made a commitment to store growth. They increased the number of stores by an amazing 90%. This combined with a 16% increase in store $ produced a 121% increase in total $. Not to rain on their parade, but their average $ per store is still slightly below the $1.84M for Total Pet Stores and 43% lower than the $3.22M for Non-Franchise Chains. Their 22% growth in employees per store should also come with an (*). They have the lowest annual pay per employee for any group, even 29% below that for Indies, and it fell -6.8% between 2012 and 2017. It is likely that they have a high and growing percentage of part-time employees.

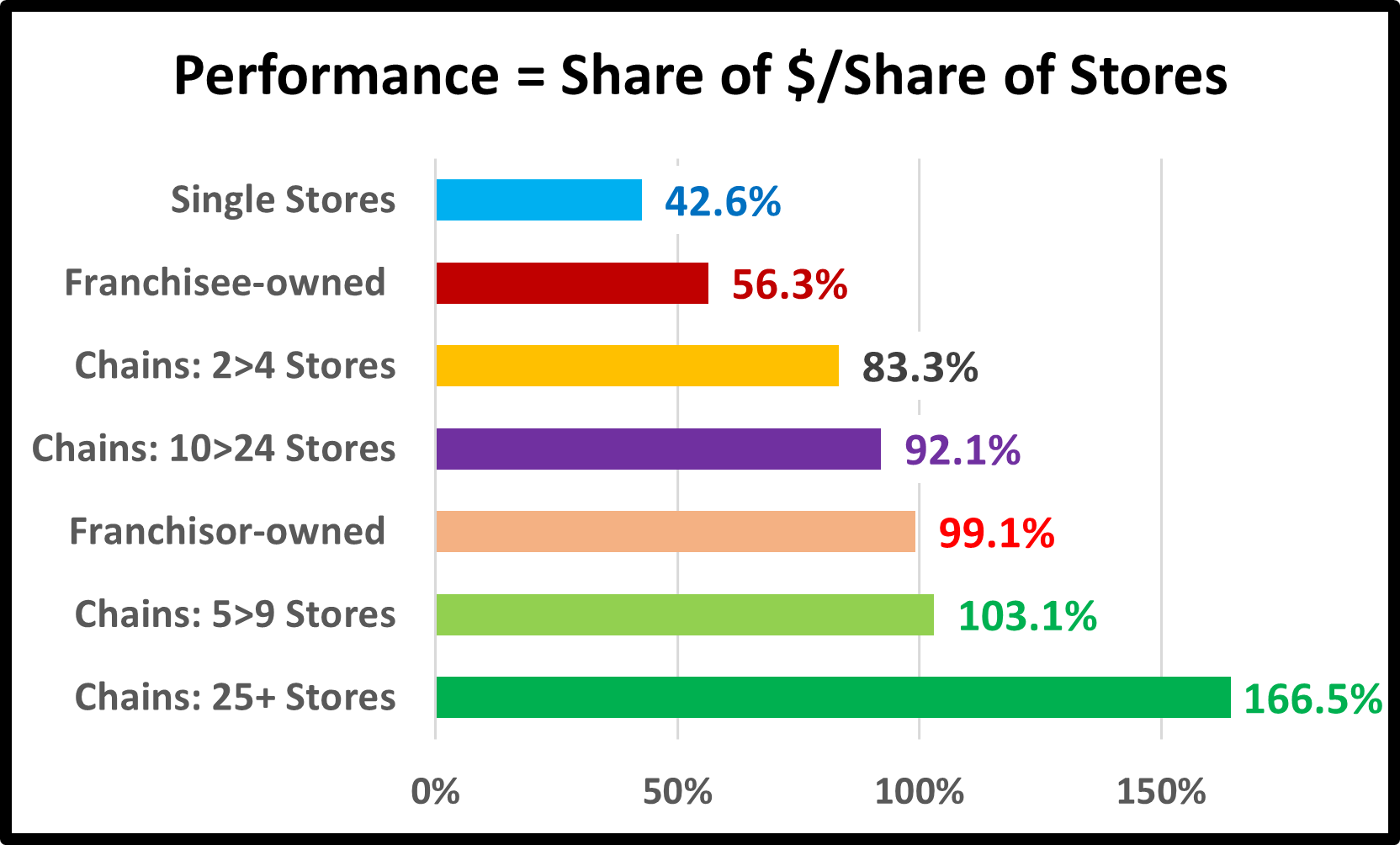

That wraps up our look at Franchised Pet Stores. We saw that Franchisee owned stores outperform Independent Stores, but Franchisor owned significantly outperformed them in store $ and growth. True performance is the share of $ divided by the share of stores. A score of 100+% means that a group is “earning their share”. Performance provides us a method to compare the subsets of Franchises to the subsets of store count. We will end our Pet Store analysis with this graph:

As expected, singles are the worst performers. If you’re considering opening a store, buying a franchise might offer more success. If you already have a successful store, should you open another? The answer appears to be yes. There is safety in numbers and greatly improved performance in the 2>4 group. Now comes the big question. Do you have the will and the resources to become a “force” in your local market? If so, then go for it. The 5>9 store group is 1 of only 2 groups performing above 100%. They even outperform the Franchisor owned group. The final step to 25+ stores is difficult and open to few. You first transition to 10>24 stores, where you learn the challenges of attaining regional success in possible anticipation of a national goal. That goal is truly “gold” as 25+ are the best performers and responsible for Pet Stores holding their ground in 2017 vs the Mass/Internet.