2022 Top 100 U.S. Retailers – Sales: $2.85 Trillion, Up 6.8% 165,205 Stores with Pet Products……plus the Internet!

The U.S. Retail market reached $8.07 Trillion in 2022 from all channels – Auto Dealers, Supermarkets, Restaurants, Online retailers and even Pet Stores. The $705B, +9.6% lift was down significantly from the pandemic recovery of +$1.14T, +18.4% in 2021. However, the Total Retail market is now $1.9T, 30.8% ahead of 2019. That’s a strong annual growth rate of +9.4%. (Data courtesy of the Census Bureau’s monthly retail trade report.)

In this report we will focus on the top 100 Retailers in the U.S. Market. The base data on the Top 100 comes from Kantar Research and was published by the National Retail Federation (NRF). The historical data for some companies that weren’t in the Top 100 all years from 2019>2022 was gathered from other reliable sources. In 2020, Restaurants were removed from the list and only Convenience stores sales for Gas Stations were included. I adjusted the 2019 list to reflect this change. This change means that the Top 100 now only includes Relevant Retail companies. The Top 100 account for 35.2% of the total market. This share peaked at 39.0% during the 2020 pandemic and has slowly declined since then. However, the Top 100 are still the “Retail Elite”. The vast majority of the group also stock and sell a lot of Pet Products so their progress is critically important to the Pet Industry. Let’s get started in our analysis. The report does contain a lot of data, but we’ll break it up into smaller pieces to make it more digestible.

We will begin our report with an overview chart of the 2019>2022 annual sales history for major segments of the Retail Marketplace. The U.S. Retail market has strongly recovered from the 2020 pandemic trauma and the resurgence has become widespread across most channels. Our regular retail sales reports have shown that different defined retail channels often took a different path from 2019 to 2021. In the Spring of 2021 and throughout 2022 the retail market faced a new challenge – strong inflation. The YOY price increases were the largest in decades, even reaching double digits near the end of 2021. The high rate didn’t start to slow until the Fall of 2022. The Top 100 analysis allows us to see if the company revenue size was a factor in their overall pandemic/price journey from 2019>2022. The following chart shows the annual sales and market share as well as the changes in both for large retail subgroups that are based upon the amount of their annual revenue. Note: In comments we’ll show Avg Growth Rates – Actual & Real (Inflation Related)

- The Total Retail Market grew $705B, +9.6% in 2022. That is less than the $1.14T, +18.4% in 2020. However, the growth rate since 2019 is 9.4%, which is still double the rate of recent years: 2019, 3.6%; 2018, 4.9%; 2017, 4.3%. Factoring in inflation, Real 19>22 growth was +3.4% compared to 18>19: +3.2%; 17>18: +3.0%; 16>17: +5.7%

- The “Non-Relevant” Retail Group (Restaurants, Auto Dlrs, Gas Stations) was hit hardest by the pandemic as sales fell -9.7% in 2020. However, they had a strong recovery as 20>22 sales grew $932B, producing an average 19>22 growth rate of 8.8%. However, high inflation was a factor for all groups. Gas Stations led the way as 19>22 prices were up +50.2%.

- Relevant Retail was the hero of the pandemic as they kept Total Retail positive in 2020. Their sales surged in the 2021 recovery then the increase slowed to +8.0% in 2022. They were still up $365B producing an average growth rate since 2019 of +9.75%. Their Real growth rate (considering inflation) was +5.75%. However, their share of Total Retail has fallen 3.5% after peaking in 2020. The story is a bit more complex. Let’s drill deeper into this group.

- The Top 100 Retailers make up 57.5% of Relevant Retail and 35.2% of Total Retail. They have shown consistent growth since 2019 but their market share has fallen since peaking in 2020 for Relevant Retail and 2019 for Total Retail. Their avg growth since 2019 is +7.1%, but Real Growth using the latest Top 100 CPI data is +3.6% – 51%.

- The biggest subgroup in $ales in the Top 100 is the Top 10 which accounts for 59% of the Top 100’s revenue, up from 55% in 2019. This group has been unchanged since 2015 and consists of Amazon, plus truly essential brick ‘n mortar retailers. Their biggest sales surge occurred in 2020 which was their peak in Retail market share. Their average growth rate since 2019 is +9.5%. The group is unchanged, so we know their Real growth was +5.7% – 60%.

- The Retailers ranked from #11 to #100 change slightly every year. Their sales in 2022 ranged from $3.7B to $76B and they accounted for 41% of the Top 100’s revenue. They have an unusual sales pattern in that their $46B decrease in 2020 is the only negative sales on the chart outside of the big drop by Rest/Auto/Gas. They did have a strong 10.7% increase in 2021 but that fell to 6.1% in 2022. They have also lost market share in Total & Relevant Retail every year since 2019 but are still a big part of U.S. Retail. Avg 19>22 Growth: +3.9%; Real: 1.0% – only 26%.

- The Relevant Retailers outside of the Top 100 don’t get a lot of “press” but maybe they should. They currently account for 42% of Relevant Retail $ and 26% of Total Retail. They had the biggest percentage increase of any Relevant Retail subgroup in all measurements since 2019. Their avg. increase since 2019 is +13.8%. Real: +9.8%, the best numbers of any group on the chart. While this performance is amazing, perhaps the most important fact is that they delivered 62% of Relevant Retail’s sales increase in 2020 and even 56% of the lift from 2019>2022.

There is no doubt that the big retailers are critical to the success of the U.S. Retail Market. However, there are sometimes “hidden heroes” that should be noted.

The Top 100 outperformed Total Retail in 2020 but not in 2021 or 2022. In fact, the sales growth since 2019 trails Total Retail, Relevant Retail and even Rest/Auto/Gas. It still generates 35.2% of Total U.S. Retail $ so it is still very important. We also should remember that the Top 100 is really a contest with a changing list of winners. Companies drop out and new ones are added. This can be the result of mergers, acquisitions, surging or slumping sales or even a corporate restructuring. In 2022, Smart & Final was acquired by Chedraui and Price Choppers merged with Tops. 4 dropped off:

- Bed, Bath & Beyond (Home Gds) • Restoration Hdwr (Home Gds) • Save Mart (Supmkt) • Urban Outfitters (Appar)

On the plus side, 4 new companies were added.

- Amway (Home Gds) • Raley’s Supermarkets (+Bashas’) • Neiman Marcus (Dept Str) • Schnucks (Supmkt)

I think that we now have a good overview of U.S. Retail and the Top 100 so let’s ask and answer a very relevant question. How many Top 100 companies are buying and selling Pet Products? This will reinforce that Pets have become an integral part of the American Household and how fierce that the competition for the Pet Parents’ $ has become.

- We should note that the data in the chart only reflects the performance of the companies in the 2022 list since 2019 and is not being compared to the Top 100 list of companies from prior years

- 87 are selling some Pet Products in stores and/or online. 2 of the companies added pet products to their offerings for the 1st time in 2022. Plus, 87 is 7 more companies than the 1st “official” all Relevant Retail Top 100 list in 2020.

- Their Total Retail Sales of all products is $2.74 Trillion which is…

- 96.4% of the total business for the Top 100

- 55.4% of Relevant Retail

- 34.0% of the Total Retail market

- 74 Cos., with $2.58T in sales sell pet products off the retail shelf in 165,205 stores – 12,000 more than 2020.

- 1 company on the current list added pet products to their shelves in 2022.

- As you can see by the growth in both sales and store count since 2019, “in store” is still the best way to sell pet.

- Online only is another story and the story gets complicated.

- Amazon includes Whole Foods, which has stores so the Amazon $ are in the “Pet in Store” numbers.

- 1 Retailer in the 2022 list added pet products to their offerings. This group had decreased sales and closed stores in 2020. Fortunately, 21 & 22 brought a rebound in both areas, but they still have the lowest 19>22 increase in $.

- Some non-pet specialty retailers like Lulumon and Signet have had extraordinarily strong post pandemic growth. However, the growth in the non-pet group has generally slowed in 2022. They have also closed 5% of their stores, which is now thankfully on hold. Perhaps, more of them will see Pet as a new growth opportunity.

- Their Total Retail Sales of all products is $2.74 Trillion which is…

The pandemic caused our Pets to become an even more important part of our households. They are truly family. Pet products have long been an integral part of the strongest retailers and are now even more widespread across the entire U.S. marketplace. Of the Top 100, 165,205 stores carry at least some pet items at retail. However, there are thousands of additional “pet” outlets including 15,000 Grocery Stores, 10,000 Pet Stores, 16,000 Vet Clinics, 6,000 Pet Services businesses and more. Pet Products are on the shelf in over 215,000 U.S. brick ‘n mortar stores… plus the internet. Pet Products have become part of the new “normal” for the majority of U.S. Retailers.

Before we analyze the whole Top 100 list in greater detail let’s take a quick look at the Top 10 retailers in the U.S.

Except for changes in rank, this group has been incredibly stable. The list has been the same since 2013, with one slight qualification. In 2015 Albertsons purchased Safeway. The new Albertsons/Safeway group replaced the stand-alone Safeway company in the list. There is one change to the chart. We have added average annual 19>22 growth rates – both Actual & Real (Inflation was factored in using specifically targeted CPIs) Now let’s get into the numbers.

- Their Total Retail Sales were $1.67 Trillion which is:

- 58.8% of Top 100 $ales, about equal to the 2020 peak (58.9%) but up considerably from 2019 (55.0%).

- 33.8% of Relevant Retail, down from 35.5% in 2020 but about the same as 2019 (34.0%).

- 20.7% of Total U.S. Retail $, down from 23.0% in 2020 but exactly the same as 2019 (20.7%).

- In ranking, Kroger & Home Depot swapped places. Walgreens fell from 6th to 8th, so Target and CVS moved up.

- Sales vs 21 & 19 are up for all but Walgreens. The biggest growth vs 21 came from Costco but Amazon is still the leader vs 19. In average growth, 5 have rates over 10%. The group averages +9.5% with +5.7% (60%) being real.

- Store count stabilized and turned up 0.3% in 22 but is still down vs 19 for 5 companies and -0.1% for the group.

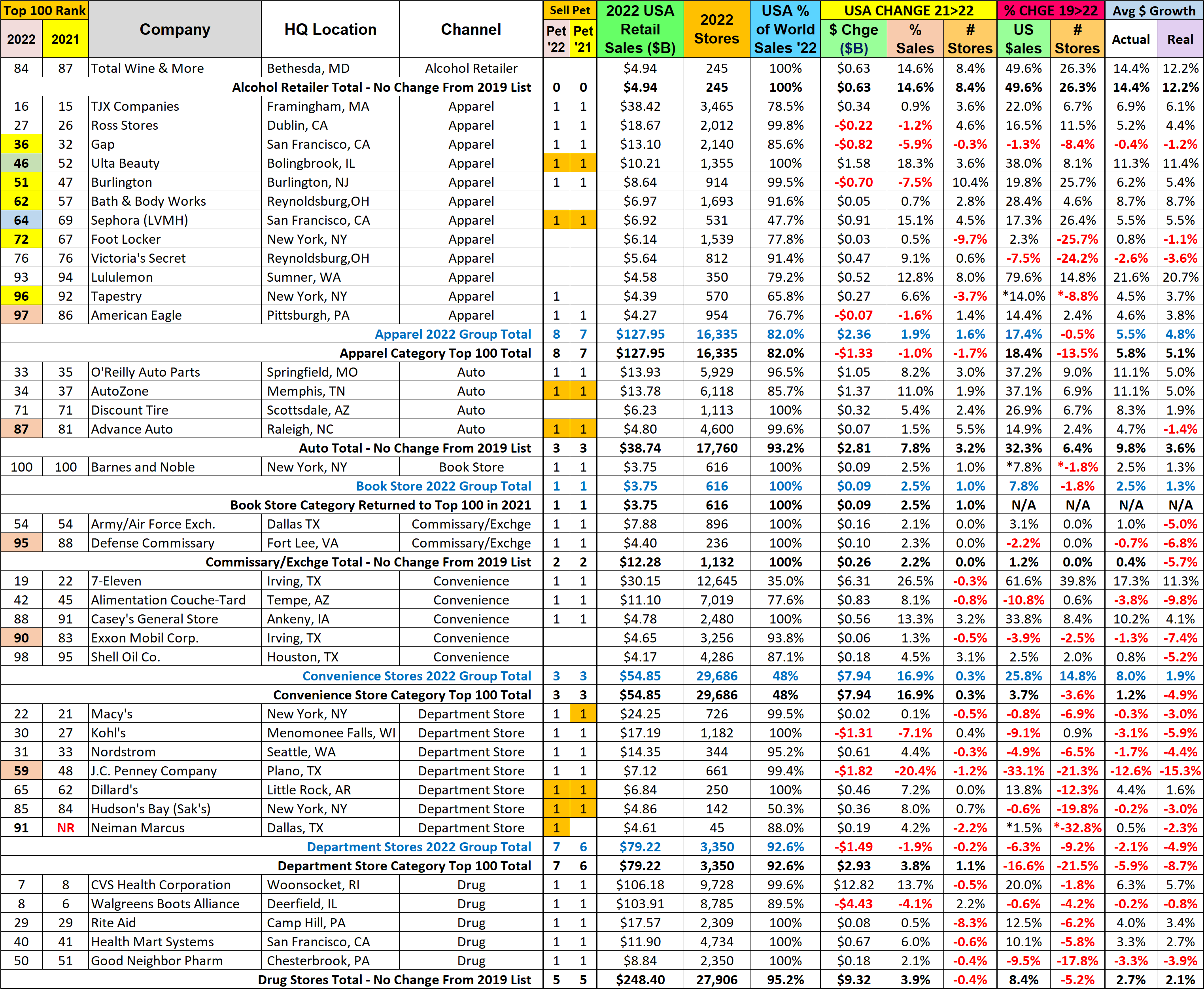

Now we’ll look at the detailed list of the top 100. It is sorted by channel groups with subtotals in key columns. For some groups there will be 2 subtotals. The subtotal in Blue compares the data history for just the 2022 list. The Black subtotal compares this year’s totals to those from previous year’s lists. Note: I used the same CPI rate for both Blue & Black Real averages because there was little difference in group share from 2019 to 2022. There is not a lot of highlighting, but:

- Pet Columns ’22 & ‘21 – a “1” with an orange highlight indicates that products are only sold online.

- Rank Columns – 2022 changes in rank from the 2021 list are highlighted as follows:

- Up 4-5 spots = Lt Blue

- Up 6 or more = Green

- Down 4-5 Spots = Yellow

- Down 6 or more = Pink

Let’s get started. Remember, online $ are included in the sales of all companies.

Note:(*) in the 2019 columns of some companies means the 2019 base was estimated from other sources.

Observations

- Alcohol Retailers first made the list in 2020 as consumers started dining at home. The behavior is accelerating.

- Apparel – They were hit hard by the pandemic, had a strong recovery in 2021, then the increase slowed in 2022. In 2022 sales decreased for companies focused on clothing while it increased for specialty and accessory stores. The average increase for the 22 group was Actual: +5.5%; Real: +4.8% (87%). Their performance differed from that of the category because the 2022 group had fewer companies than 2021 but more than 2019.

- Auto – Growth slowed a little in 2022 but the only negative for this group is that Advance Auto’s average Real Sales growth is down -1.4% from 2019. Group Avg Growth: +9.8%; Real: +3.6%.

- Book Stores – Barnes & Noble has had slow steady growth since 2019 and low inflation so 52% is real.

- Commissary/Exchanges – They have been on hold since 2019. Sales grew a little in 22 but real sales growth is -5.7%.

- Convenience Stores – Sales are up in 22 but most of the growth is due to 7-Eleven’s acquisition of Speedway. The 22 group has 8.0% average growth but only 24% is real. However, that’s much better than -4.9% for the category.

- The decline in Department Stores was accelerated by the pandemic. Sales in the category grew in 22 because of the addition of Neiman Marcus. Neiman Marcus’ sales are up slightly from 2019 but Dillard’s has the only significant actual and real growth since 19. Both the 22 group and the category are both actually and really down vs 2019. J.C. Penny, a hallmark in the department store channel, has by far the worst performance.

- Drug Stores – All but Walgreen’s increased sales in 2022 but the store closures continued. Vs 2019 only Walgreen’s and Good Neighbor Pharmacy have reduced sales but all have fewer stores. The average growth rate since 2019 is low at +2.7% but inflation is low so real growth is +2.1% (78%)

- Electronics/Entertainment – Sales Growth slowed in 22 and even fell for 3 companies. Store closures continued for electronics retailers.

- Amazon Retail growth slowed in 22 to only 36% of their average growth since 2019, but 85% is Real.

- Qurate was down for the year and the only company down vs 2019. Their avg real sales growth from 19 is -6.5%.

- 2 Electronics stores are down vs 2021 but all are up vs 2019. They continue to close stores. However, strong deflation has even pushed real sales significantly above actual.

- 22 group avg growth: +12.0%;Real: +12.5%. This is much better than the category because 22 is a smaller group.

- Farm – Tractor Supply growth slowed but is still +11.4%. Avg Growth: +19.1%; Real: +13.8% (72%). Plus, more stores.

- Hobby & Crafts– Hobby Lobby is the best performer, but both companies are up in all measurements. Avg Group Growth: 5.9%; Real: +5.4%. 92% is real.

- Home Improvement/Hardware – Growth slowed in 2022 but the only negatives on the chart come from True Value closing a few stores in 21 and the -1.6% real sales avg for Menards. Consumers are still focused on their homes.

- Harbor Freight is still growing fast. They earned a spot in the Top 100 in 2021.

- Vs 2021 & 2019 sales were up for all across the board with the biggest $ lifts coming from the 3 biggest guys.

- It is also a very healthy sign when 6 of 7 companies continue to add more stores.

- 22 Group Avg Growth: +11.5%;Real: +6.3% (55%). The category is slightly better because the group # is up by 1.

- Jewelry – Signet switched from closing to opening stores. Strong growth continues. Avg: 21.2%; Real: 18.7% (88%).

- Mass Merchants have 3 of the 7 largest volume retailers in America – Wal-Mart, Costco and Target. However, the value and selection offered by the whole group has increased its importance to consumers even more due to the pandemic.

- In 2022 Wal-Mart $ were up 8.7%, better than 6.9% in 2021 and above their average increase in sales: +7.7%. Their business is driven by SuperCenters. Groceries drove up inflation so their real sales avg increase was 3.7%, only 48%. They did stop closing discount department stores in 2022 but their store count is still -0.5% from 2019.

- Costco’s 2022 $ increase was +16.9%, up from +15.8% in 2021 and 23% more than their 13.7% average. Average real growth was 9.7% (71%). They also continued to open new stores, +5.9% vs 2019.

- Target posted a 6th consecutive sales increase in 2022, +2.8%. However, this was down a lot from +13.2% in 2021 and their 11.7% average. Their real avg growth rate is 7.7%, 66%. Their store count is up 4.3% from 2019 as they are opening more supercenters. However, they are also adding more fresh groceries to their discount stores.

- Meijer’s $ales were +5.6% from 21, up from 2.3% last year but below their avg of 6.1%. Their avg real growth is 2.1%, only 34%. Coincidentally, their avg growth rate from 2019 now exactly matches their 6.1% growth in stores.

- BJ’s is now the growth leader, +22.8% vs 21 and +55.3% vs 2019. However, we should note that Costco ranks 2nd in both comparisons. BJ’s also has 8.7% more stores than in 2019. Costco is +6.1%. BJ Avg growth: +15.8%; Real: +11.8%, 75%. Club stores have moved to the forefront.

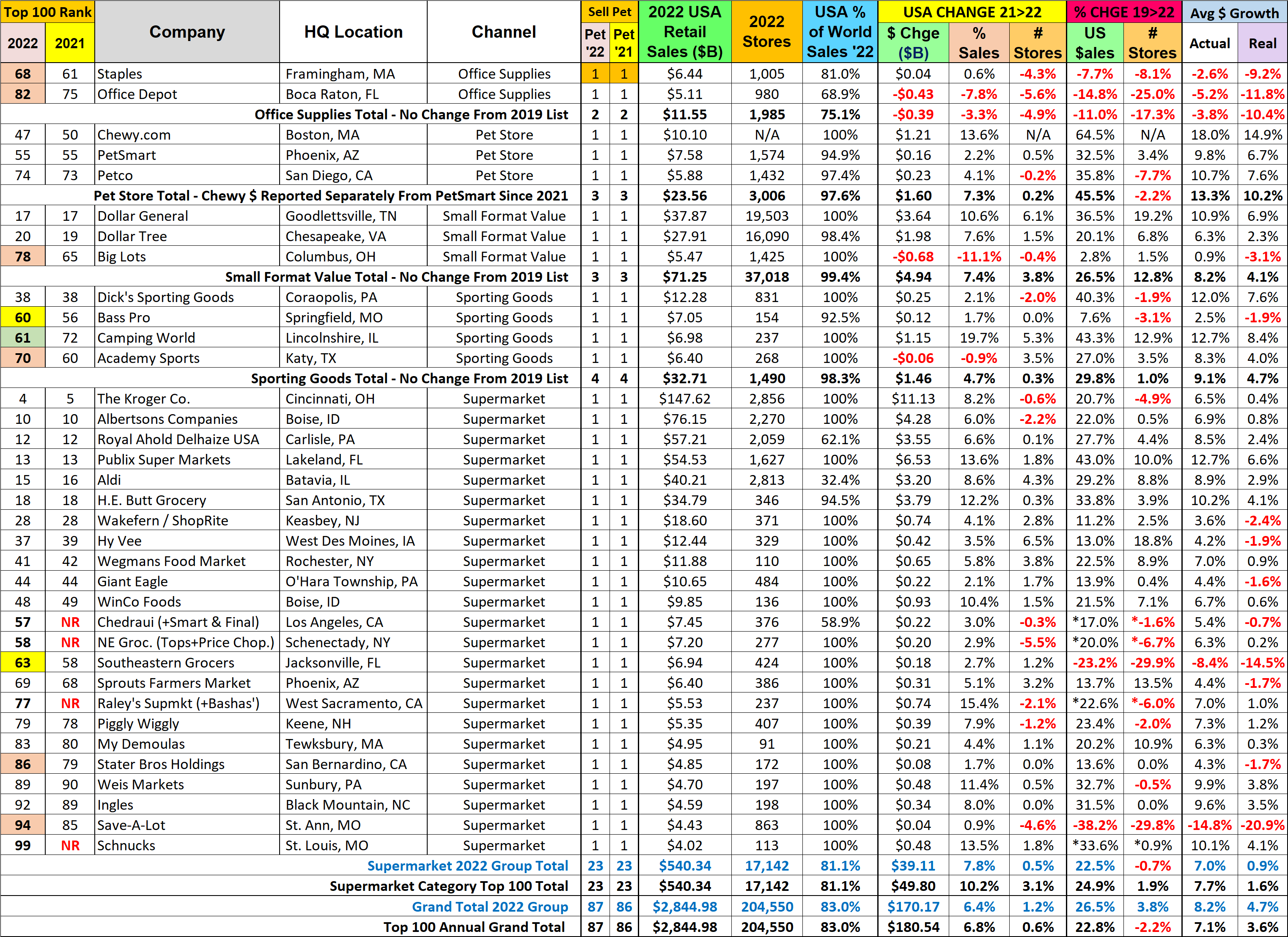

- Office Supply Stores – This channel continues its consistent decline as Consumers maintain their move to online ordering of these products. The only positive on the chart is that Staples sales were up +0.6% from 2021. The group’s average sales growth since 2019 is -3.8%; Real: -10.4%. Store count is down even more, -17.3% from 2019.

- Pet Stores growth in 2022 was +7.3%, down significantly from +22.3% last year but they are up +45.5% from 2019. Most of the growth in all measurements is coming from online sales.

- Chewy and PetSmart numbers are reported individually as they are now separate companies.

- With the strong consumer movement to online purchasing, Chewy is still the big story in this channel. They have the most sales. Their 21>22 increase was +13.6%, down from 24.4% in 21, but 76% of the Pet Store group’s 2022 $ increase. Their 64.5% sales increase vs 2019 is also nearly double that of the retail outlets. Avg Growth rate: +18.0%; Real: +14.9%. 83% of their big increase is real.

- PetSmart’s 21>22 growth was only +2.2%, 90% less than the +23.1% in 21. Sales are still up +32.5% from 2019 and they continue to expand their retail footprint with 3.4% more stores than in 2019. Their average growth rate is +9.8%. Real growth is +6.7%, 68%. This is not as good as Chewy’s, but still very good.

- Petco’s growth since 2019, +35.8% is slightly ahead of PetSmart. It also slowed markedly in 2022 to +4.1%, from +17.6% in 21. Avg growth: +10.7%; Real: +7.6%, 71%. The biggest difference between the 2 is that Petco has cut back on their retail stores, even in 2022. Their store count is now down -7.7% from 2019.

- Small Format Value Stores – These stores offer value and convenience, but there are 2 types – Big Lots & $ Stores

- Group sales grew +7.4%, up from +2.0% in 21. Avg 19>22 Growth: +8.2%; Real: +4.1%, 50%.

- Dollar General & Dollar Tree were responsible for almost all of the group’s growth in both $ and stores. Dollar General was the leader in both areas. Avg Growth: +10.9%; Real: +6.9%, 63%. Dollar Tree also looked pretty good with 6.8% more stores and avg growth of +6.3%. However, their Real growth was +2.3%, only 37%.

- Big Lots’ $ fell -11.1% from 21. Their store count is down -3.1% from 19. Avg $ Growth 19>22: +0.9%; Real: -3.1%

- Sporting Goods – Sales vs 21: +4.7%, down from +13.6% in 21. All but Academy were up vs 21 but all are up vs 19. The store count has also grown despite slight drops by Dick’s and Bass Pro. Avg $ Growth: +9.1%; Real: +4.7%, 52%.

- Camping World has the best performance vs 21 & 19 in both $ales and store growth.

- Dick’s had the biggest actual $ increase from 19>22 despite closing 1.9% of their stores since 2019.

- Bass Pro has the worst performance. They closed 3.1% of their stores in 20&21. Avg Growth: +2.5%; Real: -1.9%.

- Supermarkets – As usual there was some turmoil. Because of a merger & acquisition 2 companies were replaced. 1 other dropped out and 2 new were added. Ave Growth: +7.0%; Real: 0.9%, only 13%. Store count -0.7% from 2019.

- All were up vs 2021 in $ and only 2 were down vs 2019

- 7 companies cut back on stores in 2022 and 8 have fewer stores than in 2019.

- The category avgs and store count situation are better than for 2022 group because the group is bigger in 22.

- With $540B in sales from 17K stores, all carrying Pet Products, this group is essential both to the Retail Market and the Pet Industry.

Wrapping it up!

This report is focused on 2022 but we can also see the still evolving impact of the pandemic. In 2020 many non-essential retailers were hit with restrictions and closures. On the plus side, consumers turned their focus to essentials and their homes. This helped drive incredible growth in many retail channels.

In 2021 the Total Retail market moved into a full recovery with spectacular growth. Many channels showed a strong sales rebound from 2020. Others built upon their pandemic success while many returned to a more normal growth pattern. However, a few continued to decline. The Top 100 companies had participants in all of these patterns.

In 2022 we were hit by strong inflation in many categories which slowed both actual and real growth.

The Top 100 is a contest with the winners changing slightly every year. It is a critical part of the U.S. Market, accounting for almost 60% of Relevant Retail Revenue and 35+% of Total Retail. Sales have increased annually but the Top 100’s share of Total Retail peaked in 2020 and in 2019 for Relevant Retail and has steadily declined. The Top 10 has had consistent annual growth but sales in the #11>100 actually fell in 2020 and their 19>22 increase is only about 1/3 of the Top 10’s lift. However, we should remember that we discovered a new hero in 2021 – Relevant Retail, not in the Top 100. The 19>22 Sales by these smaller guys are +47%, 50% more than the Top 10. Their performance continues to be amazing.

Pet Products are an important part of the success of the Top 100. 87 companies (96.4% of $) sell Pet items in 165K stores and/or online. The 74 companies that stock pet products in their stores generated $2.58T in total sales. How much was from pet? Let’s “Do the math”. If we take out the $23.6B done by Top 100 Pet stores and the remaining companies generated only 1.7% of their sales from Pet, we’re looking at $43.4B in Pet Products sales from 71 non-pet sources! (The 1.7% Pet share is based on the Economic Census.) If you add Product sales for Pet Stores back in, Total Pet Products sales for the Top 100 are $67B. The APPA reported $89.6B in Pet Products sales for 2022. That means 71 mass market retailers accounted for 48.4% of all the Pet Products sold in the U.S. and 74 Top 100 companies generated 74.8%. Pet Products are widespread in the retail marketplace but the $ are concentrated. All Pet Industry participants should monitor the Top 100 group.

Retail sales increases slowed in 2022 as inflation became a major factor. The situation is still evolving but the Top 100 will always be a critical part of U.S. Retail. I hope that this detailed look helped put this group into a better perspective.