2023 U.S. TOTAL PET SPENDING $117.60B…Up ↑$14.89B

In 2023 Total Pet Spending in the U.S. was $117.60B, a $14.89B (14.5%) increase from 2022. All segments had spending increases from 2022. Veterinary and Food had the biggest lifts and the increase in Food spending set a new annual record. Together this produced a big increase in Total Pet $. Inflation was again a factor affecting spending. It slowed in Supplies but remained high in the other segments. Total Pet was 8.0%. That means that the “real” 22>23 lift was 6.0%.

- A $6.81B (+17.6%) increase in Food

- A $1.08B (+4.9%) increase in Supplies

- A $5.95B (+20.0%) increase in Veterinary

- A $1.05B (+8.5%) increase in Services

Let’s see how these numbers blend together at the household (CU) level. Weekly, 26.8 million CU’s (1/5) spent $ on their Pets – food, supplies, services, veterinary or any combination – up from 25.3M in 2022 but still below 27.1M in 2019.

In 2023, the average U.S. CU (pet & non-pet) spent a total of $874.16 on their Pets. This was a +14.1% increase from the $766.20 spent in 2022. However, this doesn’t “add up” to a 14.5% increase in Total Pet Spending. With additional data provided from the US BLS, here is what happened

- 0.3% more CU’s

- Spent 8.1% more $

- 5.6% more often

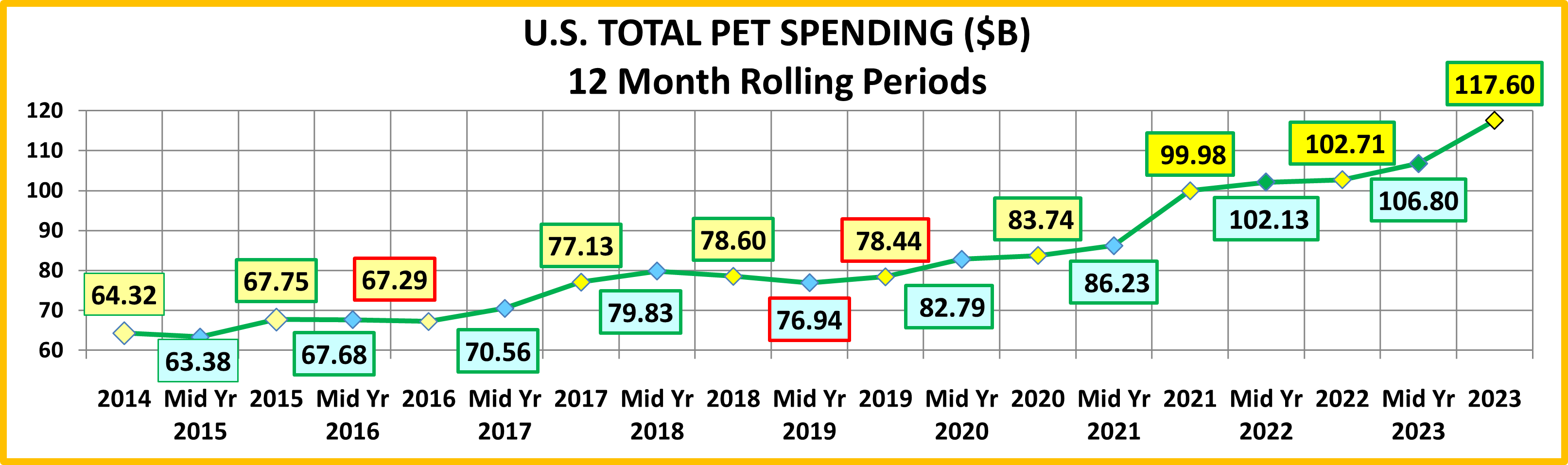

If 68% of U.S. CU’s are pet parents, then their annual CU Total Pet Spending was $1285.51. Now, let’s look at the recent history of Total Pet Spending. The rolling chart below provides a good overview. (Note: All numbers in this report come from or are calculated by using data from the US BLS Consumer Expenditure Surveys – The 2016>2023 Totals include Veterinary Numbers from the Interview survey, rather than the Diary survey due to high variation)

- In 2014-15, the Super Premium Food upgrade began, with the biggest lift coming in 2015.

- In 2016, they value shopped for super premium foods. They spent more in other segments, but spending fell slightly.

- In 2017, spending took off in all but Services, especially in the 2nd half. Consumers found more $ for their Pets.

- In 2018, a spectacular lift in Services overcame the FDA issue in Food, tariffs on Supplies and inflation in Veterinary.

- In 2019 a bounce back in Food and small lift in Veterinary couldn’t overcome the drop in Supplies from “tarifflation”.

- In 2020, consumers focused on necessities, Food & Veterinary (+$8.7B) while Services & Supplies suffered (-$3.4B).

- In 2021, there was no Food binge but in all other segments consumers made up for all the lost ground…and more!

- In 2022, big lifts in Food & Services overcame drops in Supplies & Veterinary.

- The 2022 lift was the 3rd in a row, breaking a pattern since 2010 – 2 years of increases followed by a small decrease.

- The 2023 lift was the 4th in a row, and despite strong inflation, the 3rd largest ever. Trailing only 2008: +$17.11; 2021: +$16.23.

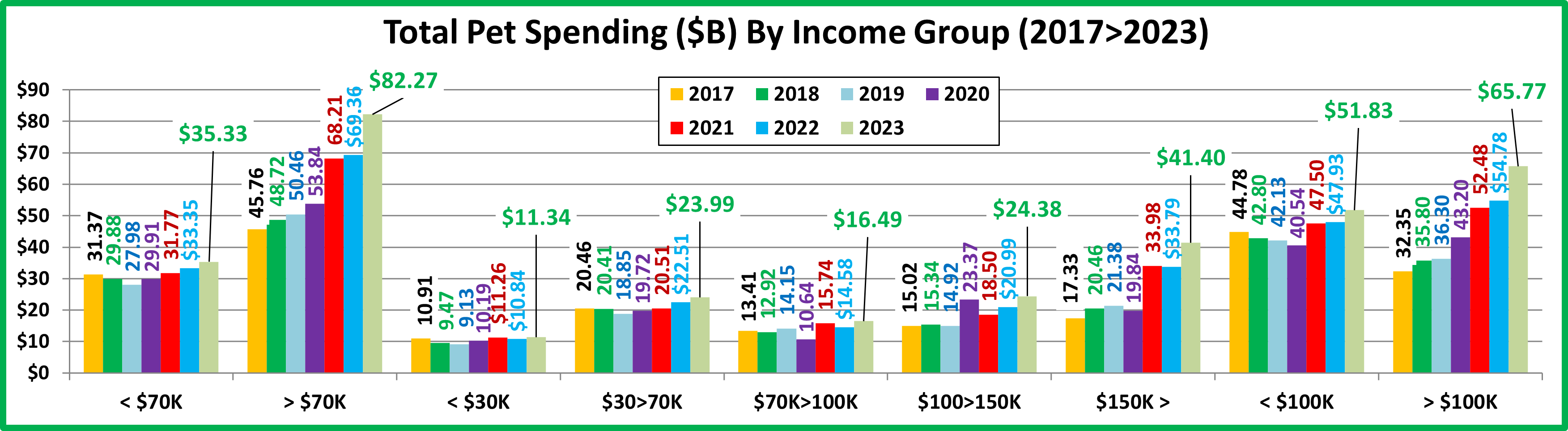

Now we’ll look at some Demographics. First, 2023 Total Pet Spending by Income Group

All income groups spent more but the biggest lifts came from the over $100K groups, especially $150K>.

Nationally: · Total Pet: ↑$14.89B · Food: ↑$6.81B · Supplies: ↑$1.08B · Services: ↑$1.05B · Veterinary: ↑$5.95B

- < $70K – (49.5% of U.S. CUs); CU Pet Spending: $529.77, +12.1%; Total $: $35.33B, ↑$1.98B (+5.9%) ..

- Food: ↑$2.44B

- Supplies: ↑$0.07B

- Services: ↓$0.06B

- Vet: ↓$0.47B

- Money matters a lot to this group. In the pandemic they focused on Pet needs. They have had slow but steady annual growth since 2019. In 2023 they focused on Pet Food.

- >$70K – (50.5% of U.S. CUs); CU Pet Spending: $1212.30, +10.9%; Total $: $82.27B, ↑$12.90B (+18.6%) from…

- Food: ↑$4.37B

- Supplies: ↑$1.01B

- Services: ↑$1.11B

- Vet: ↑$6.41B

- This group continues to grow in size, up 7.2% in 2023 and they produced 87% of the spending increase – 100+% of the 2 service segment lifts. All segments in the group had double digit % Total Pet spending lifts.

- < $30K – (21.3% of U.S. CUs); CU Pet Spending: $395.19, +13.1%; Total $: $11.34B, ↑$0.50B (+4.6%) from…

- Food: ↑$1.89B

- Supplies: ↓$0.07B

- Services: ↓$0.21B

- Vet: ↓$1.11B

- This lowest income group is shrinking but still has relatively stable spending. They remain committed to their pets, but In 2023 they focused on Pet Food as spending dropped in all other segments, especially Veterinary.

- $30>$70K – (28.3% of CUs); CU Pet Spending: $631.18, +10.9%; Total $: $23.99B, ↑$1.49B (+6.6%) from…

- Food: ↑$0.55B

- Supplies: ↑$0.14B

- Services: ↑$0.15B

- Vet: ↑$0.64B

- Again matching the National Pattern, they had increases in all segments, but all but Services were below average.

- $70>$99K – (14.1% of CUs); CU Pet Spending: $847.89, +10.6%; Tot $: $16.49B, ↑$1.91B (+13.1%) from…

- Food: ↑$0.63B

- Supplies: ↑$0.15B

- Services: ↓$0.43B

- Vet: ↑$1.56B

- This group is very price sensitive. They had a 26% drop in Services but lifts in all the others, including +40% in Vet.

- $100K>$149K– (16.6% of CUs); CU Pet Spend: $1113.13, +9.9%; Tot $: $24.38B, ↑$3.39B (+16.2%) from

- Food: ↑$1.67B

- Supplies: ↓$0.15B

- Services: ↑$0.39B

- Vet: ↑$1.47B

- In 2020 they led the way in the Food binge. In 2021 they had a huge drop in Food $ but big increases in the other segments. In 2022 they got more “on track” with the biggest Total Pet $ increase for any income segment. In 2023 Supplies $ dropped but they had big lifts in the others which produced the 2nd biggest lift in the income category.

- $150K> – (19.8% of CUs); CU Pet Spending: $1560.16, +9.5%; Total $: $41.40B, ↑$7.60B (+22.5%) from…

- Food: ↑$2.06B

- Supplies; ↑$1.00B

- Services: ↑$1.16B

- Vet: ↑$3.38B

- This group consists of 2 segments, $150>199K and $200K>. In 2021 both groups had double digit increases in all segments. 2022 was different, with an overall lift despite 2 drops. In 2023 the $150>199K group had a small decrease in Services $ but all other measurements for both groups were up from 10.5% to 55.9%. This produced a $7.6B lift which was 51% of the Total Pet increase. This group has 19.8% of CUs but generates 35.2% of Pet $.

- < $100K – (63.6% of CUs); CU Pet Spending: $600.80, +12.3; Total $: $51.83B, ↑$3.90B (+8.1%) …

- Food: ↑$3.07B

- Supplies: ↑$0.22B

- Services: ↓$0.49

- Vet: ↑$1.09B

- The only drop was from $40>49K, -$0.95B. The biggest lift was from $30>39K, +$2.35B. Regarding the drop in Services, $50>69K was the only group that spent more, +$0.40K. The biggest drop was from $70>99K, -$0.42B

- >$100K – (36.4% of CUs); CU Pet Spending: $1357.08, +10.1%; Total $: $65.778, ↑$10.99B (+20.1%) from…

- Food: ↑$3.74B

- Supplies: ↑$0.85B

- Services: ↑$1.55B

- Vet: ↑$4.85B

- The $100K> group exceeded 50% of Pet $ for the 1st time in 2020. Their lead is growing as they now do 55.9%.

Income Recap – The top 2 drivers in consumer spending behavior are value (quality + price) and convenience. That makes income very important in Pet Spending. We also often see motivation brought by new products. In 2020 we saw the results from perhaps the biggest human motivator – fear. This drove the binge buying of pet food. The huge lift from $100>149K helped push the 50/50 $ divide up to $103K, a huge change from $94K in 2019. 2021 brought a record lift and record spending in all segments but Food. This increase was driven by the $150K> income group and the 50/50 spending divide moved up to $107K. In 2022, Food & Services $ grew while Vet & Supplies fell. A big lift by $100>149K pushed the spending divide up to $108K. In 2023, all segments grew, but especially Food and Vet. The lift was driven by higher incomes so the 50/50 $ divide grew to $114K. Income continues to grow in importance in Total Pet Spending.

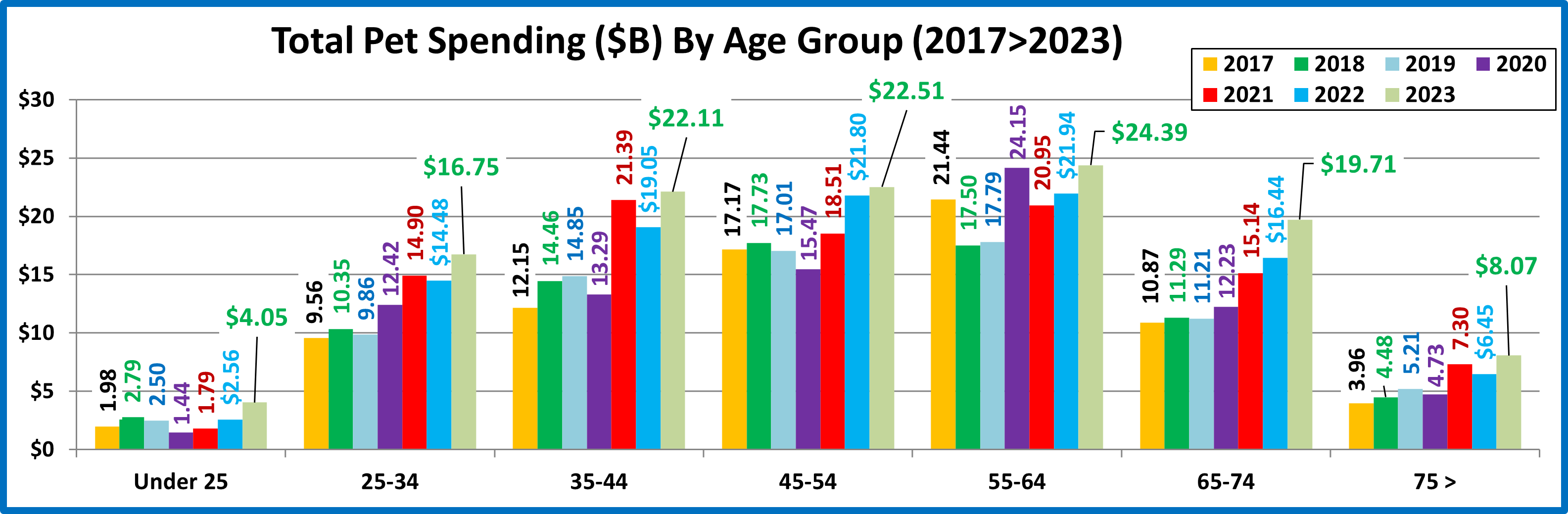

Next let’s look at 2023 Total Pet Spending by Age Group

All age groups spent more. 65>74 & 35>44 had $3+B lifts. However, all but 45>54 had a lift over $1B.

Nationally: · Total Pet: ↑$14.89B · Food: ↑$6.81B · Supplies: ↑$1.08B · Services: ↑$1.05B · Veterinary: ↑$5.95B

- <25 – (4.5% of U.S. CUs); CU Pet Spending: $653.22, +68.9%; Total $: $4.05B, ↑$1.50B (+58.5%) from…

- Food: ↑$0.37B

- Supplies: ↑$0.40B

- Services: ↑$0.001B

- Vet: ↑$0.72B

- Many consolidated into bigger CUs and some got married but their Pets were included. Plus, more pets were added which generated a lift in all segments. Overall, 3.7% fewer CUs spent 25.7% more $, 30.9% more often.

- 25-34 – (15.7% of U.S. CUs); CU Pet Spending: $799.70, +16.3%; Total $: $16.75B, ↑$2.27B (+15.7%) from…

- Food: ↑$2.02B

- Supplies: ↓$0.17B

- Services: ↓$0.18B

- Vet: ↑$0.60B

- In 2021 they had a 20% increase with a big lift in all segments. In 2022, spending fell overall and in all but Services. In 2023 spending was +15.7% due to lifts in Food & Vet. 0.9% more CUs spent 9.0% more $, 5.2% more often.

- 35-44 – (17.5% of CUs); CU Pet Spending: $931.98, +13.3%; Total $: $22.11B, ↑$3.06B (+16.1%) from…

- Food: ↑$1.25B

- Supplies: ↑$0.11B

- Services: ↑$0.31B

- Vet: ↑$1.38B

- They have the largest families and are building their careers, so they are very sensitive in times of change. In 2021 they spent more in all segments and became #1 in Total Pet $. In 2022 spending decreased and they fell to #3. In 2023 they had lifts in all segments but stayed #3 as 3.5% more CUs spent 3.0% more $, 8.9% more often.

- 45-54 – (16.9% of U.S. CUs); CU Pet Spending: $998.89, +3.3%; Total $: $22.51B, ↑$0.72B (+3.3%) from…

- Food: ↓$0.42B

- Supplies: ↑$0.84B

- Services: ↑$0.28B

- Vet: ↑$0.01B

- They have the highest income and were #1 in Pet Spending in 2018. In 2019 & 2020 their spending and rank fell. In 2021 & 2022 their spending grew but they stayed #2. In 2023, all but Food $ were up but their total lift was only 3.3%. They fell to #2 in CU spending and stayed #2 in total $. 0.1% more CUs spent 8.7% more $, 5.1% less often.

- 55-64 – (17.8% of U.S. CUs); CU Pet Spending: $1016.42, +12.2%; Total $: $24.39B, ↑$2.45B (+11.2%) from…

- Food: ↓$0.12B

- Supplies: ↓$0.26B

- Services: ↑$0.68B

- Vet: ↑$2.15B

- 60% are still younger Baby Boomers and they are very reactive. They were the drivers behind the 2020>21 binge & bust in Pet Food. In 22, spending normalized and they returned to #1. In 2023, big lifts in the Services & Vet overcame small drops in products as 2.1% fewer CUs spent 13.2% more $, 0.3% more often They are still #1 in $.

- 65-74 – (16.0% of U.S. CUs); CU Pet Spending: $909.91, +18.9%; Total $: $19.71B, ↑$3.27B (+19.9%) from…

- Food: ↑$2.35B

- Supplies: ↑$0.25B

- Services: ↓$0.09B

- Vet: ↑$0.76B

- This group is all Baby Boomers. They are careful with their money, but their commitment to their pets is very apparent. They are the only group with a spending increase every year from 2020>2023. In 2023 they increased spending in all but Services as 0.7% less CUs spent 9.7% more $, 10.0% more often.

- 75> – (11.6% of U.S. CUs); CU Pet Spending: $521.60, +21.5%; Total $: $8.07B, ↑$1.62B (+25.1%) from…

- Food: ↑$1.35B

- Supplies: ↓$0.09B

- Services: ↑$0.05B

- Vet; ↑$0.32B

- Pet parenting is more difficult, and money is tight for these oldest Pet Parents, but their commitment is still there. In 2021 they had increases in all segments. In 2022, only Food $ fell, but the drop was substantial. In 2023, they had a strong rebound in spending as their $ grew in all segments but Supplies, including a 35.4% lift in Pet Food. 2.2% more CUs spent 3.2% more $, 18.6% more often.

Age Group Recap: In 2022 Total Pet Spending skewed away from <45 to the 45>74 groups. In 2023, this reversed as <45 (38% of CUs) generated 46% of the $ lift. However, in 2023 Income became even more important in Pet spending.

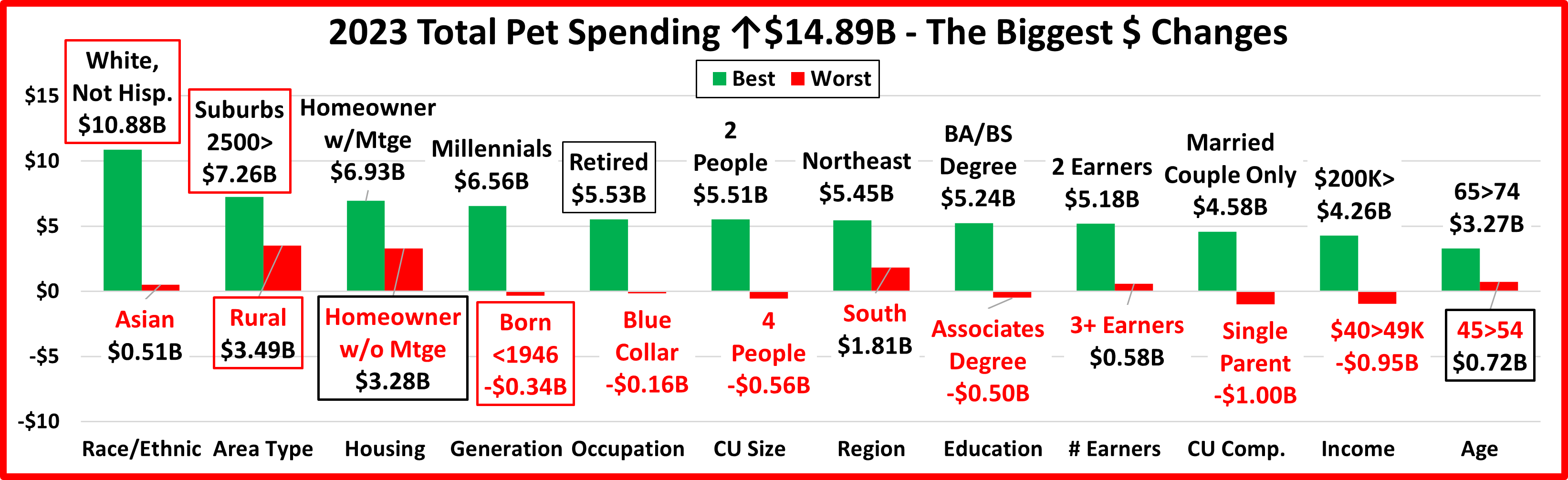

Next, we’ll take a look at some other key demographic “movers” in 2023 Total Pet Spending. The segments that are outlined in black “flipped” from 1st to last or vice versa from 2022. The red outline stayed the same.

In 2023, 87 of 96 Demographic Segments (90.6%) spent more on their Pets, a big lift from 69% in 2022. (With inflation, 78.1% spent more in 23.) Another difference was that in 2023 there were 6 categories where all segments spent more. In 2022 there was 1. There was also less turmoil in 2023 as 4 segments held their spot and only 3 of the 24 segments flipped from 1st to last or vice versa. In 2022 there were 10 flips and 3 “holds”. In 2023 all of the biggest lifts were significantly larger than the biggest drops, but the drops were generally small and only happened in 6 categories. We should also note the strong stability in the Area Type category. Both the winner and loser held their position both in 2023 and 2022. Their performance is even more memorable. Not only did they hold their position in 2022 & 2023 but in both years, there were no segments in the Area Type category with a decrease in Total Pet Spending.

Let’s look at some specifics.

10 of the winners are often on Top and almost all of them have higher incomes.

Only 2 winners are surprising, and they have 1 common trait – They are old.

• Retired • 65>74 years old

Among the losers, 6 often find themselves in this position. Note: 2 have increased spending – Asians & the South

• Asians • Born <1946 • Blue Collar • South • Single Parents • $40>49K

All but Asians have low incomes. There were 3 surprises: Note: None had a drop in spending.

• 3+ Earners • 45>54 yr-olds • Rural (despite +$0.8B spending in 22 & +$3.5B in 23)

All but Rural have a high income. However, Rural is a big Pet spender, with $1200 in annual CU pet spending.

Recap: After a slight downturn in 2019, Pet Spending turned up in 2020, primarily due to the pandemic binge buying of Pet Food. The Food binge ended in 2021 and Food $ fell. However, it was replaced by binges in the other segments. Pet Parents caught up with all the Supplies purchases that they had postponed due to the pandemic. COVID also caused them to focus on the health of their Pet Children so Veterinary also had a record increase. Services were hit hard by pandemic restrictions and closures, but they came back strong. Together, this produced a $16.23B increase in Pet Spending. 2022 brought a new challenge – radically high inflation. Supplies and Veterinary had drops in spending as their 2021 binge couldn’t be repeated. Food spending bounced back with a 12.5% increase. However, the Food lift didn’t make up for the combined drop in Veterinary & Supplies. Without the record increase in Services, Pet spending would have fallen in 2022 rather than being up $2.73B (+2.7%). However, if you consider 8.9% Petflation in 2022, the amount of Pet Products & Services sold in 2022 was really down 5.7%. Although inflation was still high in 2023, 8.0%, spending grew $14.89B to $117.60B, +14.5% (Real: +6.0%) and the lift was widespread as 90.6% of demographics spent more. It was 78.1% with inflation. All industry segments had increased spending, but the biggest lifts came from Food and Veterinary. Unlike 2022, when 45> was the driver, in 2023 most of the lift came from <45 & 65>. However, the strongest trend was in income. The $100K> group (36.4% of CUs) generated 73.8% of the increase. The 50/50 spending divide grew from $108K to $114K. In 2019, it was only $94K. In 2023, high income was by far the biggest driver in Pet Spending.